Beware! Market’s At An All-Time High Again.

What If…

It Tanks Tomorrow?

Don’t want to lose your hard-earned money

in an overvalued equity market?

Read this letter urgently now.

Dear Investor,

It was 15th of September in 2008. It was a cool, fine afternoon with a red streak painted right across the horizon.

Mr. Gonsalves was driving home from work when he heard the news on the radio — “Lehman Brothers files for bankruptcy-court protection.”

His car halted to a screech.

Even if he was not really well-versed with the financial markets, he knew something bad was going on.

The market represented by Nifty 50 index dropped by another 18 percent in a matter of a month and was almost 47 percent down from its peak seen in January 2008.

He realized he had made a BIG mistake.

Not by putting his entire retirement savings into the market.

But perhaps, by ending up investing in an overvalued market, when the Nifty 50 was at its peak.

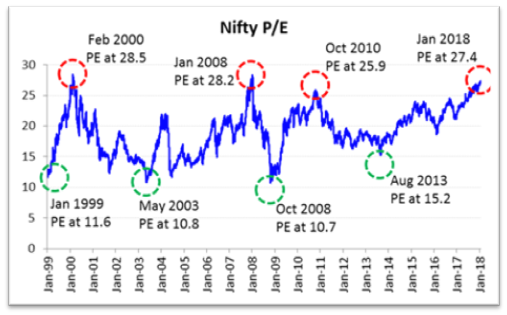

(The price-to-earnings (P/E) ratio, the measure of a market’s expensiveness, was around 28 then. Whew!)

What Mr. Gonsalves didn’t know was that investing in an overvalued equity market is inherently risky. As a matter of fact, the chances of making mistakes rise exponentially during these times of greed and uncertainty.

Why are we even talking about this?

Good question.

Because… the P/E ratio of Nifty 50 on a trailing basis stands at the same level today as it was then. Currently, it is about a whopping 27.

India is one of the world’s most expensive markets at present, based on price-to-earnings (P/E) ratio.

And we are worried.

Why? Because of this graph below.

Source: nseindia.com (Data as on 19-Jan-2018)

Whenever the market goes up without any solid reason to back it up, it is bound to correct to its fair valuation.

Every time, abundance of liquidity…

Some sudden global event…

Or simply, when our lack of financial knowledge pushes the market up, it comes back to its original level sooner or later.

So the case at hand:

The market is at its peak again.

Just like when Mr. Gonsalves invested his hard-earned savings.

And the question is…

What will happen next?

Will the market sustain its present valuation level?

Our research says that this overvalued market is not backed by strong fundamentals but rather by excess liquidity and inflow of foreign money.

It’s probably an “illusion”—yes, scarily so.

What if it does not sustain?

More importantly, what should you, as an investor, do?

We are going to explore it in the next couple of minutes. So, get yourself a mug of coffee and read on…

What If The Market Goes Down Tomorrow?

An absurd question? We guess not.

While quite a few popular money managers are strongly touting on the future growth potential of Indian market and…

Heck! Even the World Bank projects India's GDP to grow at 7.3% in 2018-19.

But that’s still a PREDICTION.

Wasn’t it the same before the 2008-2009 crisis?

Wasn’t everyone too optimistic to even pay heed to the bold red signals then?

How can we ever forget our foolishness then?

But what’s more important is, are we being foolish now?

Indian equities have been rallying since February 2016 even as economic growth had slumped to its weakest since the year 2014.

Our research team fears that the current market valuation is driven more by excess liquidity in the domestic and global markets, and less by economic fundamentals.

And they fear that we might be standing on the brink of a massive U-turn of the Indian capital market.

What if Kim Jong Un presses the buttons that he claims to be on his desk, and President Trump retaliates, with the bigger ones that he has on his desk?

What if there is another Brexit like scenario (any other European nation breaking out from the Euro zone)?

What if another sub-prime crisis is waiting around the corner?

What if BJP loses the next election?

What if crude oil prices reach 100 dollars again? (It’s already soaring!)

Last but not the least, what if it is just a bubble, after all, only to correct to its fair valuation in the near future?

Even while we (including most money managers want to think that this time might be different, the question is…

What if it is not?

What if something bad happens?

You must be wondering…

“So, Should I Not Invest Now?”

Wrong question, really.

Equity is one of the most important asset classes, and without investing in equities, you will not be able to achieve your financial goals and objectives. Period.

If you stall on investing now, you would probably be losing out on time.

And time is money.

But, weren’t we saying that the markets might go down?

Weren’t we talking about how Mr. Gonsalves lost all his retirement savings this way?

Ah…poor, old Mr. Gonsalves.

Let’s talk about what happened to Mr. Gonsalves after the crash. (And also why expensiveness is never a problem but something else is.)

Although he was not a financially savvy person, he still held on to his stocks as his best friend suggested him. His friend said, “Market’s are going to come back up. Stay put.”

Well, he did likewise.

And lo! The market rose to glory again. By November 2014, the market was up by 100 percent.

Hurrah! Good news…Mr. Gonsalves’ retirement savings comes back from the dead.

Well, not quite.

Even though the market went up by such significant percentage, the stocks that Mr. Gonsalves invested in were still lingering at those marginal levels.

How can this be?

His friend told him to stay put, right?

Even the market recovered?

So, what’s the issue now?

Okay, let’s put it this way. (or let’s say, break our very FIRST assumption here.)

His mistake was not because he invested in the market during its peak.

His real mistake was something else.

…What Was His Real Mistake?

Glad you are still here with us.

Because now, we are going to break you the secret to investing during overvalued markets.

And also, where Mr. Gonsalves went wrong…really.

The answer is, he bought stocks that were meant to ultimately lose his money. Simple.

That’s the reason he still incurred losses even when the market went up. Because his stocks were fundamentally weak in the first place.

They were all riding high due to the excess market liquidity…or let’s say, a foolishly positive market sentiment.

When the reality set in, the market corrected itself to its initial price levels.

And there’s the serious issue that you face in an overvalued market as an investor.

When all the stocks are riding high at the same time, how would you know which one is right and which one is wrong?

You cannot stall investing till the market goes down, because you may not be able to time the market, rightly. And honestly speaking, you may just be stalling your journey to financial freedom in that case. (A bad choice.)

However, if you invest and…that also, in the wrong stocks, you may end up losing your hard-earned savings. (We pity Mr. Gonsalves.)

Thinking, “What to do then?”

Here’s our answer…

Our Frank Advice For You

To Invest In Equities In Risky Markets

It’s better not to attempt to try to choose the stocks yourself.

If you are an average retail investor like most are...

You definitely don’t scour through dozens of financial journals every day.

You definitely don’t stay glued to Bloomberg for latest market news.

You definitely don’t crunch calculators pouring over financial statements.

So, it’s going to be a rather tricky affair for you.

More so in this tricky and fickle overvalued market.

Here’s our frank advice for you:

Invest in equity mutual funds instead.

Let those highly qualified and experienced fund managers work for you.

Let them make the right stock picks for you.

But wait! Not every fund manager can be relied upon and...

Not every fund ends up making you money.

And if you think that the most popular fund you get to hear about every day, whether on the TV news channels or in the financial journals, is the right one, you are dead wrong.

Here’s an example of it.

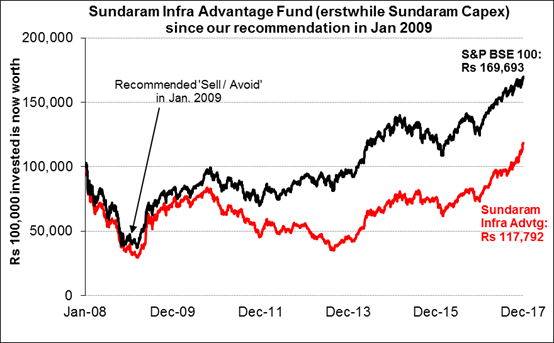

Have you heard about Sundaram Capex Fund?

The fund that became investor’s favourite during the infrastructure and capital boom in 2007. Its AUM doubled, rather tripled within months, in the year 2007.

Unfortunately, hype doesn’t sell for long in finance.

Many investors in this fund found themselves on the back foot, when the rally in the infrastructure came to a break during the 2008 subprime crisis. Notably many stocks in this sector have not yet recovered and so has the fund.

(Source: ACEMF, PersonalFN Research)

Performance from 1-Jan-2008 to 29-Dec-2017

PersonalFN has always recommended to avoid this fund. Past performance of the fund is neither an indicator nor a guarantee of its future performance.

On the other hand, In 2011, Mirae Asset Mutual Fund was a little talked about fund house, which had just completed 3 years of operation in India. Its flagship scheme Mirae Asset India Opportunities Fund was hardly known to investors. The fund was very small with a corpus of less than Rs 200 crore, then.

This is when PersonalFN identified the early potential of this fund and recommended it to the subscribers, way back in October 2011. Now with a corpus of over Rs 6,000 crore, the fund has grown big and made money for its investors too. It has been one of the top performing funds in its category.

(Source: ACEMF, PersonalFN Research)

Performance from 3-Jan-2011 to 29-Dec-2017

Past performance of the fund is neither an indicator nor a guarantee of its future performance.

You need to select your mutual funds very carefully.

Don’t fall for the hype around a fund.

Rather look deeper than you normally would.

And always…

Keep this little statistic in mind: around 3 out of 4 mutual fund investments are NOT worth your money.

But one of them potentially turns out to be a WINNER.

Arguably…

One out of four funds regularly beats the market by a wide margin.

One out of four funds performs well across market cycles.

One out of four funds possesses the ability to make you wealthy…in the long term.

How to find that hidden treasure?

Simple. Ask yourself these questions below.

Is the fund manager qualified to manage the fund? Is he well experienced? Does he have an innate sense of the market movement? And so on.

Is there a steady investment strategy? Don’t invest in a fund that chases hot trends. Look for a fund that is based on solid conviction, long term vision and sticks to the investment process and systems irrespective of market conditions.

How much expense ratio are you bearing? Even a few basis points can make a whole lot of difference! In fact, an additional expense ratio of 1% can easily erode as much as 50-55% from your investment returns in 15 years!

Is the fund diversified enough? Yes, you want to invest in equities and equities inherently are risky assets. But still, is it diversified enough to minimize the risk as much as possible? A narrowly focused fund might not be the best way to invest in equities.

Is the fund consistent enough? Make sure the fund has shown its mettle in the long-term past performance track record. Not one, not two, not even three—you should check 5-years track record as well; and more preferably their performance across past market cycles, to be sure of what you are putting your money in.

Does the fund belong to an investor friendly fund house? A fund house needs to be investor-friendly. Does the fund manager put his money where his mouth is? Is it a big fund or small? Are the scheme information documents, investor communication or fund reports transparent, clear and consistent? Pay attention to this.

When you find an equity mutual fund that passes these 6 questions favourably, you know that you have a great fund at hand.

Still thinking?

Wondering, “How to go about with this hectic, time-consuming process?”

It sure is.

We mean, it takes our whole research team working from 9-6 every day to come up with some of the best investment ideas out there.

How can an average investor like you carry out this alone?

…after finishing your own day job, and studies, if any.

…after reserving some quality time with your family & friends.

…after taking rest for a bit with yourself at last.

We hear you.

And we might have a better solution for you.

You wished to invest in equities in 2018, and that’s why we are writing this letter for.

We bring to you a ‘ready-made’ solution instead…drum-roll, please…

Our latest exclusive report

“Top 5 Equity Funds To Invest In 2018”

This exclusive report has been created keeping the Investment Scenario IN 2018 in mind.

If you have a question, “What equity funds to invest in NOW? Under the current market conditions?”

This report is the answer to your question.

In this report, you will find our recommended top 5 equity funds to invest in, carefully selected by testing each one of them as per our very own 7-point Selection Matrix.

We have tested them according to quantitative criteria.(That is, what do the numbers show?)

We have tested them according to qualitative criteria. (That is, what do the factors behind the numbers show?)

They have passed our tests with flying colours!

Here’s a brief overview of the funds that are being covered in this report:

Fund #1:

A large-cap oriented fund with a track-record spanning over two decades, that has established itself in the large-cap category with its consistent long term performance and has rewarded investors with superior risk-adjusted returns. The fund has not only kept risk under control, but has managed to deliver benchmark-beating returns as well. Its ability to curb the downside risk makes it an ideal fund to provide stability in ones long term portfolio.

Fund #2:

A decade old mid-cap fund that has come to the limelight recently. The fund has not disappointed over the recent market cycles and scores well in terms of managing risk. It has delivered superior risk-adjusted returns for its investors who have stayed invested in the fund for the long term. The fund manager looks for high growth oriented stocks in the mid cap segment, but which are available at fair valuations. Being a mid-cap oriented scheme, high volatility cannot be ruled out.

Fund #3:

A flexi style fund that has turned out to be a clear winner within its category. With its dynamic performance, the fund has been consistently generating superior risk-adjusted returns for its investors over the past few years. Despite being an actively managed fund, it has kept risk under control and has consistently delivered benchmark-beating returns. Its ability to tap the market rally and curb the downside risk makes it an ideal fund for long term investors.

Fund #4:

An opportunities style fund that has shown a turnaround in performance and has gradually climbed its way up the ranks over the last couple of years. The fund has performed extraordinarily well, posting a substantial margin in outperformance when compared to its peers. Though the volatility is comparable to that of other schemes in the category, this fund now scores high on risk-adjusted return and thus adds to positives that ranks the fund higher.

Fund #5:

A less popular fund that takes contrarian bets and invests in out of flavour sectors and stocks which are available at significant discount or cheap valuations. What differentiates this fund from its peers is its ability to enter stocks at right valuations and timely exit from underperforming stocks. This fund has been outperforming its benchmark by a substantial margin, while keeping volatility in check. It scores high on risk-adjusted returns and has consistently delivered superior returns for its investors who have stayed invested in the fund.

These are the FIVE funds that we believe hold the best wealth-creating potential in the coming few years.

Whether the market goes up or down, you need not worry.

These five funds, as per our research, are well poised to garner steady and significant returns over time, regardless of what happens tomorrow.

Click here to get this report now.

Are you still thinking?

It’s about meeting your financial aspirations.

It’s about achieving financial freedom.

It’s about living a happy & blissful life.

Equities have created wealth for investors in the past.

Equities are making money for investors even now.

Equities will keep doing so in the future as well.

It all depends on investing in the RIGHT one.

These five equity funds are what come with the best future investment return potential.

These are potentially the “best-of-the-best” equity funds out there.

And you get instant access to ALL these funds by subscribing to our exclusive report for a nominal one-time fee.

How much does the report cost?

Well, if you sign up now, we are happy to grant you with…

A Huge Introductory Discount

Of Over 50 Percent

For ‘First 1,000 Subscribers’!

Usually, this report will be valued at around Rs 2,000. It is a reasonable price, in our opinion, if you are going to invest Rs 1 lakh or even more in equities.

You would probably make multiple times that little meagre amount in returns, after all.

Isn’t it? Of course, it is.

However, how would it be an introductory offer, right?

So, to make it more attractive and accessible to you, we have lowered the price further.

If you subscribe to this introductory offer, you would pay Rs 2000 Rs 950 only.

That’s a whopping discount of OVER 50 PERCENT!

How cool is that? In fact, is it for real?

Yes, it is.

Only if you meet one simple condition.

You need to be among our first 1,000 subscribers.

Trust us when we say, that limit is probably going to expire in the next few hours, perhaps.

And we don’t want you to miss out.

So, act fast.

It’s your golden chance.

We want you to grab it while you can.

Don’t be like Mr. Gonsalves.

He probably didn’t have such awesome report at hand.

But you have.

If you are into equity investing, and you are looking to invest in 2018—a tricky time to invest in, let us guide you through this report.

Click here to get instant access to this exclusive report right now.

That’s all for now.

Wishing you a wealthy year ahead.

To your wealth,

Team PersonalFN

P.S. Do NOT stall investing in the equity market. The time is now. Looking for the RIGHT equity funds to invest in? Here are the ones for you…

P. P. S. Remember, the first 1,000 subscribers get more than 50 percent discount. Don’t miss this awesome opportunity for anything. It’s your freedom…your life…at the cost of a T-shirt.

*Price inclusive of applicable Goods and Services tax

** The performance data quoted above represents past performance and does not guarantee future results.

© Quantum Information Services Pvt. Ltd. All rights reserved.

Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021

Corp. Office: 103, Regent Chambers, Nariman Point, Mumbai 400 021.

Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 Mob.:8422907179 Mob.:8422907179 Mob.:8422907179 CIN: U65990MH1989PTC054667

SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013