5 Common Credit Card Problems And Solutions

Ketki Jadhav

Jun 20, 2022

Listen to 5 Common Credit Card Problems And Solutions

00:00

00:00

Credit cards are beneficial in many ways. With its differed payment benefit, you can buy your favourite item today and pay for it on a future date. Moreover, with a disciplined use of credit cards, you can improve your credit score over time and get qualified for bigger loans and higher credit limits. However, like anything else in the world, credit cards, too, are not perfect! Credit cardholders often come across several credit card problems that create a burden on the cardholders and can impact their financial well-being. This article states 5 common Credit Card Problems and their solutions to help you have a smooth credit card experience.

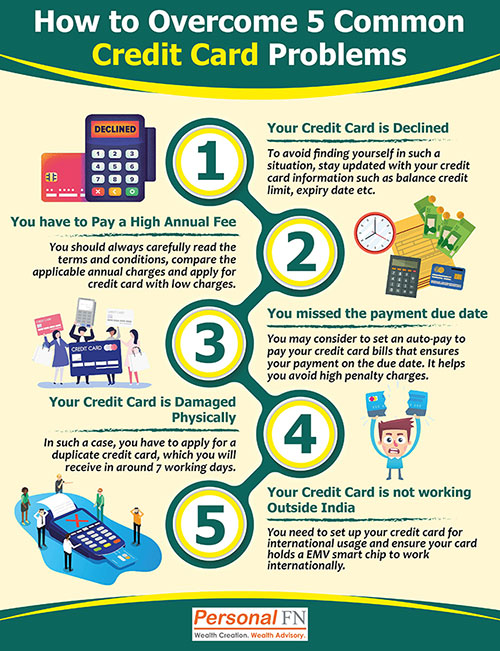

1. Credit Card Declined:

Has it ever happened to you that you went shopping or had a fancy dinner with your friends or family and insisted you would make the payment, but the cashier handed over the credit card back to you, saying the card is declined? Finding yourself in such a situation is frustrating. There could be several reasons for credit card getting declined, such as insufficient credit limit, card blocked, card suspended, card expired, pending KYC, or even network or technical issue.

To avoid finding yourself in such a frustrating situation, it is advisable to stay updated with your credit card by reading the important messages and emails sent by the credit card provider. It will help you know if you have any pending KYC, card expiry date, card blocked due to suspicious transaction history, etc., so that you can take the necessary action in advance. The most common reason for Credit Card decline is the insufficient credit limit. Hence, you should always check your credit limit before making big purchases.

2. High Annual Fee:

Many individuals try to hold several credit cards to get the benefit of the credit card offers from different merchants. Since many credit cardholders do not check the annual fee when applying for a credit card, the annual fee comes as an unpleasant surprise on the credit card bill. As many credit cards do not charge the annual fee in the first year to make the sale, some salespersons do not upfront disclose the fees that are chargeable from the second year. Besides, managing multiple cards can be tricky since they all come with different features, credit limits, interest rates, and due dates. People with multiple credit cards tend to forget the due date of the bill payments, which results in unintentional default in repayment.

To avoid such credit card issues, it is advisable to hold a maximum of 2 to 3 credit cards based on your requirements. Most importantly, before applying for a Credit Card, you should always carefully read the terms and conditions and service charges. Click here to know what is the ideal number of credit cards you should hold based on your lifestyle.

(Image Source: www.freepik.com)

(Image Source: www.freepik.com)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds

3. Missing the Payment Due Date:

Many credit card holders create debt by spending more than they planned, which becomes unaffordable to pay on the due date of a credit card bill. Whereas some cardholders genuinely forget the due date, especially those who hold multiple cards. Whatever could be the reason, if you fail to repay the entire credit card due amount on or before the due date, the credit card provider starts charging you a high rate of interest from that very date until the entire amount is paid. The rate of interest is usually very high on credit cards, which ultimately increases the outstanding amount. When paying the bill, some people again fall into the trap of 'Minimum Amount Due' and pay only the minimum required amount. While doing this, they might not be aware that they will be charged interest on the unpaid amount until they repay it in full.

Therefore, You should always pay your credit card bills in full before the due date. If you have already created a debt, try to pay as much as possible to minimise the interest amount. Before making high purchase transactions, have a proper payment plan in mind and be consistent in clearing the total dues on time. In addition, it is advisable to set an auto-pay to pay your credit card bills. It will ensure your credit card bills get paid automatically on the due date through your registered bank account. In case if the credit card bill is unaffordable to pay, you can convert your purchase/s into EMIs by logging into your credit card account or calling the customer service department, depending on the terms and conditions of the credit card issuer and your credit limit.

4. Physical Credit Card Damage:

If you have been holding your credit card for years, your credit card can refuse to get swiped as it becomes demagnetised. It generally happens due to wear and tear and overexposure to a magnet. The cashier will not be able to swipe your credit card to collect the payment. Sometimes instead of swiping, they can dial the entire number in the machine, but not all the merchants will be able to do that.

In such a case, you have to apply for a duplicate credit card. You can do so by logging into your internet banking or calling customer service. After the request is made, you typically receive the new card in 7 working days. However, depending on the terms and conditions of your credit card provider, you can be charged with a credit card re-issuance fee.

5. Credit Card Not Working Outside India:

Many credit cards require you to set up your international credit card usage after receiving the card. Otherwise, the card will not work outside India or on international websites. Hence, if you make purchases from international websites or planning to use your credit card outside India, you should enable the international credit card usage and set up the international credit card limit on your credit card. It can be done by logging into your online credit card account or internet banking, or you can contact the customer service of the card issuer and make the request. The requested limit is generally made available to use immediately after placing the request.

Another reason for a Credit Card not working outside India could be holding a non-EMV chip credit card. If you have an old credit card without EMV smart chip, it will not work internationally. Therefore, before travelling internationally, you should request a new credit card. All the new cards come with an EMV chip.

Before using your credit card internally, you should first check the international usage charges applicable to the card. Since these charges could be high, it makes sense to use a Forex Card for international travel expenses.

To Conclude:

The interest rate, fees and charges, terms and conditions, etc., of the credit cards, can vary from card to card and change frequently. Hence, it is advisable to read the important communication sent by the credit card providers. Taking necessary precautions for these common credit card problems and keeping the solutions in mind will help you avoid such frustrating situations. Also, click here to read the 10 common credit card mistakes you should avoid.

Warm Regards,

Ketki Jadhav

Content Writer