3 Best Banking & PSU Debt Funds for 2025

Rounaq Neroy

Dec 18, 2024 / Reading Time: Approx. 25 mins

The Reserve Bank of India in its December 2024 bi-monthly monetary policy once again kept the policy rate unchanged for the 11th successive time and the stance of the monetary policy was also kept 'neutral' as the Monetary Policy Committee (MPC) decided to remain unambiguously focused on a durable alignment of inflation with the target while supporting growth.

The stance of the monetary policy allows the RBI to respond appropriately depending on incoming data -- mainly inflation and GDP growth.

The newly appointed RBI Governor, Sanjay Malhotra (who took charge on December 11, 2024) has said, "Stability in policy and continuity is very important. Decisions will be taken with public interest to preserve trust in this institution."

However, it appears that we are almost ear the peak of the current interest rate upcycle. Going forward, if inflation moderates and is well within the RBI's target range, the RBI may cut policy interest rates perhaps in February 2025 and/or April 2025.

For those of you wanting to keep some money safe in a bank Fixed Deposit (FD,) this is an opportune time (before we witness a rate cut). FDs with tenures of 6 months, 1 year, or 2 years provide a meaningful balance of returns, liquidity, and flexibility as per your needs.

[Read: Here's Why You Should Invest in Bank FDs Now]

But if your investment time horizon is longer, say 2 to 3 years, and do not mind market-linked returns, then some of the best Banking & PSU Debt Funds could be considered as an alternative to park your money into a bank fixed deposit.

Banking & PSU Debt Fund is one of the sub-categories of debt mutual fund schemes in India as categorised by the capital market regulator, SEBI.

In this article, I'm going to elucidate which are the three best or top-performing Banking & PSU Debt Funds for 2025, but before that, let's understand some basics.

What Are Banking & PSU Debt Funds?

Banking & PSU Debt Funds, a sub-category of debt mutual funds, predominantly invest in top-rated corporate debt instruments issued by Banks, Public Sector Undertaking (PSUs), Public Financial Institutions (PFIs), Municipal bonds, and other such securities.

The regulatory guidelines make it mandatory to allocate a minimum of 80% of their assets into such debt instruments. The Debt instruments from these entities are recognised for their robust credibility and liquidity compared to those from private issuers, making them a relatively safer investment option. But it should be recognised that Banking & PSU Debt Funds aren't entirely risk-free.

As regards the maturity of debt papers, Banking & PSU Debt Funds have the flexibility to diversify their exposure across the yield curve. So, there isn't any fixed limit for the portfolio duration.

Having said that, most Banking & PSU Debt Funds typically maintain durations of around 2 to 5 years or more. The decision is based on the evaluation of various micro and macroeconomic factors, including the interest rate cycle.

Now given the kind of maturity profile (of 2 to 5 years or more) debt papers, Banking & PSU Debt Funds are moderately sensitive to interest rates. Particularly in volatile and rising interest rate scenarios, they are susceptible. That being said, these funds can benefit from regular coupon payments and may implement a partial accrual strategy to mitigate volatility during periods of rising rates.

Watch this video to know which are Best Banking & PSU Debt Funds:

What Is the Investment Objective of Banking & PSU Debt Funds?

Broadly, the primary investment objective of Banking & PSU Debt Funds is to generate reasonable returns in line with the aforesaid debt and money market securities by maintaining an optimal balance of yield, safety, and liquidity.

However, there is no assurance that the investment objective will be realised.

Are Banking & PSU Debt Funds Safe?

Although this sub-category of debt mutual funds, mainly invests in instruments from reputable banks, PSUs, and PFIs, investment in Banking & PSU Debt Funds cannot construed as safe or risk-free (compared to an FD with a robust bank).

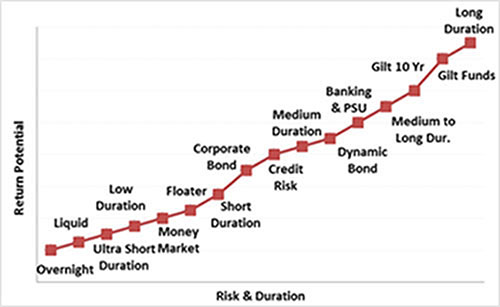

Graph: Risk-Return Spectrum Debt Mutual Funds

For illustration purposes only

For illustration purposes only

(Source: PersonalFN Research)

Banking & PSU Debt Funds do carry some level of interest rate and credit risk. Much depends on the portfolio characteristics of the respective scheme you decide to add to your portfolio. However owing to the short-to-medium duration typically maintained, indicatively Banking & PSU debt funds on the risk-return spectrum are placed a notch below the Medium-to-Long Duration Funds.

Is It an Opportune Time to Invest in Banking & PSU Debt Funds?

As you may know, interest rates and yields share a positive or direct correlation. Meaning when interest rates fall, bond yields also soften. Similarly, when interest rates go up, bond yields harden.

On the other hand, yields and bond prices share an inverse relation. Meaning, that when interest rates and yields move up, prices of bonds go down, whereas when interest rates go down and yields soften, bond prices go up.

Currently, at the peak of the interest rate upcycle in India and it is anticipated that the RBI will cut the policy interest rates going forward to support growth, the 10-year benchmark G-sec yield has eased to around 6.80% nearly a 3-year low. If the RBI indeed cut rates going forward abetted by moderation in CPI inflation, the 10-year benchmark yield could soften further. This is a positive for bond prices (as they will move up) owing to their inverse relation with bond yields.

Now, while the margin of safety has increased after a cumulative 250 basis points (bps) policy repo rate increase is almost absorbed in the economy, as an investor, you need to be cautious and conscious of the underlying debt papers held by the schemes.

To make the best choice among a plethora of Banking & PSU Debt Funds available, you must pay close attention to portfolio characteristics, the risk that the fund manager is taking (and whether it's justified), and the investment processes and systems followed at the fund house.

Prefer safely managed Banking & PSU Debt Funds that carry low credit risk and interest rate risk, as opposed to those engaging in yield hunting, i.e. taking higher credit risk for higher yields to clock high returns but paying little attention to the risk involved.

If you choose among the best Banking & PSU Debt Funds with worthy portfolio characteristics, i.e., high-quality debt papers and suitable duration (of around 2 to 5 years), it could offer stability and potentially earn you decent market-linked returns.

The category average returns over 1 year, 2 years, and 3 years are 7.3% absolute, 6.8% CAGR, and 5.7% CAGR, respectively, as of December 16, 2024.

How to Make the Best Choice of Banking & PSU Debt Funds for 2025?

To make the best choice from a plethora of schemes available, you need to evaluate a host of quantitative and qualitative parameters, such as the following:

-

The AUM and expense ratio of the scheme

-

The credentials and experience of the fund management team

-

The portfolio characteristics (who are the issuers, the sector they belong to, the type of debt papers held, the ratings of the respective debt papers, etc.)

-

The maturity profile of the fund (the average maturity, Yield-To-Maturity (YTM), and the Modified Duration (MD) of the portfolio)

-

Returns across time periods (6 months, 1 year, 2 years, 3 years, and so on)

-

The performance across interest rate cycles

-

The risk ratios (Standard Deviation, Sharpe Ratio, Sortino Ratio, etc.)

Also, it would be better to understand the investment ideologies, processes, and systems followed at the respective mutual fund house.

If the mutual fund house lacks a robust risk management framework and depends excessively on ratings assigned by credit rating agencies, the fund manager compromises on the quality of the portfolio, chases yields, and plays down on the liquidity aspects of the portfolio, then as an investor, you should be concerned.

Also, note that while evaluating historical returns it is okay to an extent to understand how the respective fund has fared in the past, it would not be worthwhile laying too much emphasis on it, as past returns are not indicative of future returns.

Further, don't be fooled by mutual fund star ratings. Many agencies or institutions assign these ratings based only on quantitative parameters of a mutual fund scheme, mainly historical returns, which may or may not be sustainable in the future.

Watch this video where our Founder of PersonalFN, Ajit Dayal, exposes the flaws of the popular star ratings given by certain agencies/organisations.

If you rely on mutual fund star ratings, it is possible that the 4 or 5-star rated fund that you added to your portfolio today may lose some of its stars (the sheen) if its performance lags in the future.

Keep in mind that mutual fund star ratings say nothing about the future potential of the fund. Relying on star ratings given on historical performance is akin to driving a car looking mostly in the rear-view mirror, which could result in a disaster.

To understand how the fund would fare in the future, it is important to give importance to qualitative factors as well, mainly the portfolio characteristics followed by the investment processes and systems at the fund house.

Which Are the Best Banking & PSU Debt Funds for 2025?

Considering the aforementioned parameters to make the best choice, the three Best Banking & PSU Debt Funds for 2025 are:

1. ICICI Prudential Banking & PSU Debt Fund

2. HDFC Banking & PSU Debt Fund

3. Bandhan Banking & PSU Debt Fund

These schemes hold quality debt papers of banks, PSUs, and PFIs plus with a maturity profile of around 3 to 5 years.

Table 1: 3 Best Banking & PSU Debt Funds for 2025

Data as of December 16, 2024

The list of funds cited here is not exhaustive.

Returns expressed are rolling returns in % and calculated using the Direct Plan-Growth option.

Standard Deviation indicates Total Risk and Sharpe Ratio measures the Risk-Adjusted Return. They are calculated over 2 years assuming a risk-free rate of 6% p.a.

Past performance is not an indicator of future returns.*Please note, that this table only represents the best-performing schemes based solely on past returns. The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

(Source: ACE MF, data collated by PersonalFN Research)

Here are some other details as to why these schemes are best in the Banking & PSU Debt Funds category...

Best Banking & PSU Debt Fund for 2025 #1: ICICI Prudential Banking & PSU Debt Fund

Launched in January 2010, ICICI Prudential Banking & PSU Debt Fund (IPBPDF) is a leading fund in the Banking & PSU Debt Fund category, aiming to optimise returns by investing in top-rated debt and money market instruments issued by Banks, Public Sector Undertakings (PSUs), Public Financial Institutions (PFIs), and Municipal Bonds.

At present, IPBPDF is holding significant portions of its assets in Corporate Debt, but they are all in AAA-rated securities issued by trusted corporate entities. A portion of the fund's portfolio (16.1% as of November 2024) is also held in sovereign-rated assets, i.e. Government securities (both, Central and State Government). So, the fund focuses on high-quality instruments in the endeavour to achieve its investment objective. Only 0.2% is held in an unrated Alternative Investment Fund (AIF), namely the Corporate Debt Market Development Fund.

While selecting securities, the fund undertakes rigorous in-depth credit evaluation to mitigate the risks. In addition, the investment team studies the macroeconomic conditions, including the political and economic environment as well as the other factors affecting liquidity and interest rates and accordingly positions the portfolio. It holds a fairly diversified portfolio across maturity papers.

As per the November 2024 portion, IPBPDF is holding 33.7% in 1 to 2 years maturity debt papers, and sensing the opportunity at the longer end of the yield curve, it is also holding 28.1% and 9.5% of its total assets in the 7 to 10 years maturity bucket and 5 to years bucket, respectively. The remaining holdings are all in shorter maturity buckets wherein the fund seizes accrual opportunities that align with its investment goals. In other words, actively adjusts its investment allocations and maturity profile in response to macroeconomic changes such as interest rates, inflation, market conditions, and liquidity.

Table 2: Top 10 Holdings of ICICI Prudential Banking & PSU Debt

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.10% GOI - 08-Apr-2034 |

Government Securities |

SOV |

7.71 |

| GOI FRB 22-Sep-2033 |

Government Securities |

SOV |

6.63 |

| Small Industries Development Bank of India Sr III 07.25% (31-Jul-25) |

Corporate Debt |

AAA & Equiv |

5.18 |

| HDFC Bank Ltd. SR-US006 7.75% (13-Jun-33) |

Corporate Debt |

AAA & Equiv |

4.21 |

| State Bank of India SR-II 06.24% (21-Sep-30) |

Corporate Debt |

AAA & Equiv |

3.67 |

| National Bank For Agriculture & Rural Development SR 23H 7.58% (31-Jul-26) |

Corporate Debt |

AAA & Equiv |

3.07 |

| National Bank For Agriculture & Rural Development SR-23 G 7.57% (19-Mar-26) |

Corporate Debt |

AAA & Equiv |

2.84 |

| Housing & Urban Development Corporation Ltd. -SR-C 7.68% (16-May-26) |

Corporate Debt |

AAA & Equiv |

2.47 |

| Mahanagar Telephone Nigam Ltd. SR-VIII TR C 07.80% (07-Nov-33) |

Corporate Debt |

AA & Equiv |

2.39 |

| Bharat Petroleum Corpn. Ltd. 7.58% (17-Mar-26) |

Corporate Debt |

AAA & Equiv |

2.19 |

Data as of November 30, 2024

(Source: ACE MF, PersonalFN Research)

IPBPDF maintains a well-diversified debt portfolio, typically holding between 80 to 100 securities. As per its portfolio as of November 2024 portfolio, the fund's assets amounted to around Rs 9,127 crore spread across 96 debt securities. The top 10 holdings comprised 40.4% of the fund's portfolio.

The Average Maturity of IPBPDF is 4.52 years, while the Yield-to-Maturity is currently 7.54%. YTM refers to the returns the fund expects to generate from its debt paper holdings until maturity. As the fund buys and sells debt papers for its portfolio, the YTM changes.

The balanced approach with a robust and well-rounded portfolio has delivered respectable returns while managing the risks well.

IPBPDF is a top performer in the Banking & PSU Debt Funds category, delivering solid returns across various timeframes. Since its inception, IPBPDF has clocked a compounded annualised return of 8.2%.

Over 3 years and 5 years, the fund has achieved rolling CAGRs of 6.32% and 7.26%, respectively, thus outperforming the category average returns and of the benchmark index, i.e. Crisil Short Term Bond Index (as of December 16, 2024).

In terms of risk-return metric, IPBPDF stands out offering strong risk-adjusted returns. It boasts a low standard deviation of 0.51%, well below the category average of 0.78%, along with a respectable Sharpe ratio of 1.02 and a Sortino ratio of 0.55 (as of December 16, 2024). The fund also has a competitive expense ratio of 0.74% for the regular plan and 0.39% for the direct plan, making it attractive compared to many peers in its category.

IPBPDF is an ideal choice for investors with a moderate-to-high risk tolerance who seek competitive returns from reliable Banking and PSU instruments, with a minimum investment horizon of 3 years.

ICICI Prudential Banking & PSU Debt has been managed by Mr Manish Banthia since September 2024 and Mr Rohit Lakhotia since June 2023. Before Manish Banthia, the fund was managed by Ms Chandini Gupta along with Mr Rohit Lakhotia.

Mr Manish Banthia is the Chief Investment Officer (CIO) - Fixed Income at ICICI Prudential AMC and leads the Fixed Income desk at the company. He holds an MBA and is a Chartered Accountant (CA), with nearly 20 years of overall work experience. He is also responsible for the debt investments of several other debt-oriented schemes at ICICI Prudential Mutual Fund.

Mr Rohit Lakhotia has been co-managing this fund since June 2023. He has earned his B.Tech from the National Institute of Technology, Rourkela, and holds an MBA in Finance from IIM, Mumbai. Rohit has over 5 years of experience in the fixed-income space.

Before joining ICICI Prudential Mutual Fund, he worked with Yes Bank in the Corporate Banking Group.

Best Banking & PSU Debt Fund for 2025 #2: HDFC Banking & PSU Debt Fund

Launched in March 2014, HDFC Banking & PSU Debt Fund (HBPDF) focuses on high-quality debt instruments issued by Banks, PSUs, PFIs, and Municipal Bonds. Plus, the fund has sizeable exposure to Government securities (G-secs) and high-rated corporate debt from private entities.

The fund adopts a strategic approach to diversify its holdings, aiming to invest in instruments with moderate to high ratings to maximise yield generation and ensure stable returns for its investors.

A dominant portion of its assets are AAA-rated corporate debt papers and government securities, and it holds cash-and-cash equivalents while aiming to achieve its investment objective. Much like its peers, HBPDF has a small allocation (of 0.27%) to an unrated AIF, namely the Corporate Debt Market Development Fund.

The Average Maturity of HBPDF is 5.13 years. Typically, it mainly holds debt securities with maturities between 3 and 5 years. However, recognising the opportunity at the longer end of the yield curve, HBPDF is also holding 26.4% of its total assets in the 7 to 10 years maturity bucket and 3.7% in the 10 to 15 years maturity bucket currently. By having exposure to shorter maturity bonds as well, the fund is also taking advantage of accrual opportunities. The fund manager keeps flexibility to adjust the fund's portfolio duration in response to changes in interest rate expectations, liquidity conditions, and broader economic factors.

Table 3: Top 10 Holdings of HDFC Banking & PSU Debt Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.18% GOI - 14-Aug-2033 |

Government Securities |

SOV |

5.13 |

| Indian Railway Finance Corpn Ltd SR-178 7.46% (18-Jun-29) |

Corporate Debt |

AAA & Equiv |

4.71 |

| Small Industries Development Bank of India SR-IX 07.59% (10-Feb-26) |

Corporate Debt |

AAA & Equiv |

3.82 |

| 07.26% GOI - 06-Feb-2033 |

Government Securities |

SOV |

3.75 |

| Indian Railway Finance Corpn Ltd SR-175 07.57% (18-Apr-29) |

Corporate Debt |

AAA & Equiv |

3.44 |

| State Bank of India SR-II 07.33% (20-Sep-39) |

Corporate Debt |

AAA & Equiv |

2.97 |

| Bajaj Housing Finance Ltd. - 08.10% (08-Jul-27) |

Corporate Debt |

AAA & Equiv |

2.57 |

| REC Ltd.-SR-216-A 07.55% (31-Mar-28) |

Corporate Debt |

AAA & Equiv |

2.56 |

| Small Industries Development Bank of India SR-II 07.44% (04-Sep-26) |

Corporate Debt |

AAA & Equiv |

2.37 |

| Housing And Urban Development Corporation Ltd. SR-V 8.41 (15-Mar-29) |

Corporate Debt |

AAA & Equiv |

2.22 |

Data as of November 30, 2024

(Source: ACE MF, PersonalFN Research)

Currently, as per the November 2024 portfolio, HBPDF has 83 debt securities in its portfolio. Its top 10 holdings account for 33.5% of the fund's portfolio, making it well-diversified.

Although HBPDF is considered relatively safer than its peers in the corporate bond funds category, it still carries some credit and interest rate risks. Nevertheless, HBPDF has consistently delivered an impressive performance, exceeding investor expectations with stable returns. The fund manager employs strategies to protect the portfolio from interest rate fluctuations while also managing credit risk through diversification.

Since inception, HBPDF has clocked a compounded annualised return of 8.0%, while the fund's Yield-to-Maturity is 7.37%. Over 3 years and 5 years, it has recorded rolling returns of 5.8% CAGR and 7.1% CAGR, respectively, positioning itself decently in the Banking & PSU Debt Funds category and has outperformed the Crisil Short Term Bond Index (as of December 16, 2024).

HBPDF's track record underscores its ability to provide solid returns with low-risk levels (as denoted by the Standard Deviation of 0.68). With a Sharpe Ratio of 0.72, the fund has generated strong risk-adjusted returns, and its Sortino Ratio of 0.55 is among the best in the category, indicating respectable performance even during volatile market conditions. The fund's expense ratio at 0.39% for the direct plan and 0.79% for the regular plan, is slightly higher than some of its peers but has justified the same with its performance.

HBPDF has been in the top quartile on performance. Thus, HBPDF is a solid choice for investors seeking stable and competitive returns with moderate risk in the Banking & PSU Debt Funds segment for a minimum investment horizon of 2 to 3 years.

HDFC Banking & PSU Debt Fund has been managed by Mr Anil Bamboli since its inception.

Mr Bamboli is a Senior Fund Manager - Debt at HDFC Mutual Fund. He has a collective experience of nearly three decades in Fund Management, Research, and Fixed Income dealing. Before joining HDFC AMC in July 2003, Mr Bamboli worked as Asst. Vice President at SBI Funds Management. Mr Bamboli holds an MMS (Finance) degree, Grad CWA, and is a CFA Charter holder.

Best Banking & PSU Debt Fund for 2025 #3: Bandhan Banking & PSU Debt Fund

Bandhan Banking & PSU Debt Fund (BBPDF), erstwhile known as IDFC Banking & PSU Debt Fund, was launched in March 2013 before the takeover of IDFC AMC by Bandhan AMC.

BBPDF aims to maximise returns through investments in top-rated money market and debt securities issued by Banks, Public Sector Undertakings (PSUs), Public Financial Institutions (PFIs), and Municipal Bonds.

To achieve its investment objective, Bandhan Banking & PSU Debt Fund mainly invests in a mix of securities. Currently, as per its portfolio as of November 2024, BBPDF has 54.2% exposure to Corporate Debt, 26.9% in G-secs, cumulatively 16.5% in Certificate of Deposits (CDs) and Commercial Papers (CPs), and 2.2% in Cash & Cash Equivalents. Mere 0.3% is held in an unrated AIF, i.e. namely the Corporate Debt Market Development Fund.

A majority of BBPDF's assets are in AAA-rated corporate debt papers (of reputed banks, housing finance companies, power finance companies, and PSU players), and sovereign assets, i.e. Central and State Government securities. There is a minimal level of credit risk, particularly associated with certain instruments issued by private entities.

For portfolio construction, the fund assesses inflation, interest rate cycles, overall liquidity, and other macroeconomic dynamics. BBPDF employs a robust risk management strategy to effectively mitigate risks associated with debt market investments.

Table 4: Top 10 Holdings of Bandhan Banking & PSU Debt Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.18% GOI - 14-Aug-2033 |

Government Securities |

SOV |

13.69 |

| 07.17% GOI - 17-Apr-2030 |

Government Securities |

SOV |

8.90 |

| Indian Railway Finance Corpn Ltd SR-168 A 07.40% (18-Apr-26) |

Corporate Debt |

AAA & Equiv |

5.37 |

| Indian Railway Finance Corpn Ltd SR-170A 7.51% (15-Apr-26) |

Corporate Debt |

AAA & Equiv |

4.19 |

| National Bank For Agriculture & Rural Development SR-23 G 7.57% (19-Mar-26) |

Corporate Debt |

AAA & Equiv |

3.66 |

| Export Import Bank of India -364D (10-Nov-25) |

Commercial Paper |

AAA & Equiv |

3.46 |

| 07.10% GOI - 08-Apr-2034 |

Government Securities |

SOV |

3.14 |

| REC Ltd.-SR-219-BD 07.60% (28-Feb-26) |

Corporate Debt |

AAA & Equiv |

2.92 |

| Nuclear Power Corporation of India Ltd. SR-XXXVIII 7.70% (20-Mar-38) |

Corporate Debt |

AAA & Equiv |

2.70 |

| NTPC Ltd. SR-62 07.58% (23-Aug-26) |

Corporate Debt |

AAA & Equiv |

2.60 |

Data as of November 30, 2024

(Source: ACE MF, PersonalFN Research)

BBPDF maintains a diversified debt portfolio, typically consisting of 50 to 80 securities. At present, as per the November 2024 portfolio, the has around 73 debt securities. The top holding comprises 50.6% of the portfolio of BBPDF.

The Average Maturity of the portfolio is around 3.04 years, while the fund is predominantly focusing currently on instruments in the 1 to 2 years maturity bucket (39.9% of its total asset as of November 30, 2024). It also holds 2.6% of its assets in the 2 to 3 years maturity bucket and 3.5% of its assets in the medium-term 3 to 5 years maturity bucket.

Sensing the investment the opportunity at the longer end of the yield curve, BBPDF is also currently holding 2.7% of its total assets in the 10 to 15 years maturity bucket, 9.4% of its assets in the 9 to 12 months maturity bucket, 16.8% of its total assets in the 7 to 10 years maturity bucket, 10.1% in the 5 to 7 years maturity bucket (as of November 30, 2024).

The rest of the assets are in shorter maturity buckets enabling BBPDF to leverage on the accrual opportunities.

This balanced approach has ensured a robust, well-rounded portfolio that aims to optimise returns while managing risk effectively.

The current YTM of the fund is 7.3%, but this could change as the fund manager buys and sells debt securities in the portfolio.

Even amidst rising interest rates, the fund has shown resilience. Since its inception, BBPDF has clocked a compounded annualised return of 7.79% (of December 16, 2024).

Over the last 3 years and 5 years, BBPDF has delivered CAGRs of 5.6% and 7.1%, respectively, on a rolling return basis (as of December 16, 2024), thus remaining almost competitive with the category average and the benchmark index.

With a standard deviation of 0.70%, significantly lower than the category average, the BBPDF has maintained a reasonable Sharpe ratio of 0.59 and Sortino ratio of 0.47 (as of December 16, 2024). Thus, BBPDF has also fared decently on the risk-return metric.

BBPDF is well-suited for investors with a moderate to high-risk tolerance, seeking competitive returns from reliable Banking and PSU instruments, and who have a minimum investment horizon of 3 years.

Bandhan Banking & PSU Debt Fund has been managed by Mr Suyash Choudhary since July 2021 and Mr Gautum Kaul since November 2021.

Mr Suyash Choudhary is the Head of Fixed Income at Bandhan Mutual Fund. He has over two decades of experience in Fixed Income. He holds a BA (Hons) in Economics from Delhi University and, a Post Graduate Diploma in Management from the Indian Institute of Management, Calcutta.

Mr Kaul is a Senior Fund Manager - Fixed Income at Bandhan Mutual Fund. He holds an MBA (in Finance) from Savitribai Phule Pune University. Gautam Kaul has over 15 years of experience in the fixed-income space.

Overall, these three Banking & PSU Debt Funds are from fund houses that follow robust investment processes and systems.

Who Should Invest in the Best Banking & PSU Debt Funds?

Banking & PSU Debt Funds are meant for investors with a moderate-risk appetite having an investment horizon of around 2 to 3 years, and want to have exposure to banking & PSU debt securities. At present, around 30% of your debt mutual fund portfolio could be allocated to some of the best Banking & PSU Debt Funds.

Note, that some degree of credit risk and interest rate risk is likely when investing in Banking & PSU Debt Funds.

What Are the Tax Implications of Investing in Banking & PSU Debt Funds?

All debt funds, including Liquid Funds, with effect from April 1, 2023, the capital gain arising at the time of redemption -- whether short-term (a holding period of less than 36 months) or long-term (a holding period of 36 months and above) -- are taxed as per investors' tax slab.

[Read: Taxation of Debt Mutual Funds - Here is All You Need to Know]

For NRIs, the capital gains on debt-oriented mutual funds are subject to Tax Deduction at Source (TDS) at the rate of 30% if STCG and 12.5% in the case of LTCG.

If you have opted for the dividend option (now known as the IDCW option), for resident Indians, any dividends from Liquid Funds (under the Dividend Option) are added to the investors' total income and are taxed according to your income-tax slab, i.e., at the marginal rate of taxation.

However, if the dividend amount is more than Rs 5,000, Tax Deduction at Source (TDS) will be first done at the rate of 10%. For NRIs, the dividend/IDCW received is subject to a 20% TDS or at the rate specified under the relevant double tax avoidance agreement, whichever is lower as per section 196A of the Income Tax Act.

To sum-up...

Make an informed decision when you invest in Banking & PSU Debt Funds - or any mutual fund for that matter. Don't live under the impression that investing in debt mutual funds is safe or risk-free; they are not.

When investing in Banking & PSU Debt Funds or any type of fund, don't just base your investment decision on past returns or mutual star ratings given on historical performance, but also pay close attention to the portfolio characteristics of the funds.

Be a thoughtful investor; deploy your hard-earned money sensibly in line with your personal risk profile, broader investment objective, the financial goals you're addressing, and investment horizon. When in doubt, speak to a SEBI-registered investment advisor.

Happy Investing!

Related links:

4 Best Tax Saving Mutual Funds or ELSS for 2025

3 Best Large Cap Funds for 2025 - Top Performing Bluechip Mutual Funds in India

3 Best Large & Midcap Funds for 2025 - Top Performing Large & Midcap Mutual Funds in India

3 Best Flexi Cap Funds for 2025 - Top Performing Flexi Cap Mutual Funds in India

The Ultimate Guide to the Best SIP Plans for 2025

3 Best Liquid Funds for 2025 - Top Liquid Mutual Funds for 2025

3 Best Medium to Long Duration Debt Funds for 2025

3 Best Dynamic Bond Funds for 2025

Note: This write-up is for information purposes and does not constitute any kind of investment advice or a recommendation to Buy / Hold / Sell a fund. Returns mentioned herein are in no way a guarantee or promise of future returns. Mutual Fund Investments are subject to market risks, read all scheme-related documents carefully before investing.

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.