3 Best Dynamic Bond Funds for 2025

Rounaq Neroy

Dec 05, 2024 / Reading Time: Approx 25 mins

In the December bi-monthly monetary policy for 2024-25, it looks unlikely that the Reserve Bank of India (RBI) would cut the policy interest rates. A majority of the six-member Monetary Policy Committee (MPC) is likely to keep rates unchanged for the eleventh time in a row and maintain a 'neutral' stance.

This is because, the CPI inflation data for October 2024 has inched up to 6.21% (a 14-month high) from 5.49% in the previous month, surpassing the RBI's target range of 2-6%.

This is mainly due to higher inflation in food & beverage (at 10.87%, which is a 15-month high) has nearly a 46% weight in the CPI basket.

As reported by Business Standard, the government is now considering reducing the weight of food items in the Consumer Price Index (CPI) basket to address inflation concerns.

That said, given that food prices are critical and directly impact the budget of the common man, the weightage of food may come down not more than 3% to 6%.

And say, if the government in its statistical jugglery removes certain food items that are kitchen staples, such as onions, tomatoes, potatoes, etc., it would distort the true picture of inflation on the ground.

The government reportedly is also contemplating changing the base year to 2024 from the earlier 2012 -- another statistical jugglery -- to very smartly prove that it has been successful in handling retail inflation.

The opposition cognisant of the ploy likely to be played, has called this manipulative instead of the government addressing the volatility in the food prices and hoarding issues. Here's what Jairam Ramesh, Senior leader of the Indian National Congress and Member of the Rajya Sabha said in a statement on this issue:

"The prime minister's entire focus is not on reducing inflation, but on showing low inflation figures. The government is now concertedly attempting to manipulate the Consumer Price Index (CPI) and Wholesale Price Index (WPI) figures to show inflation as being under control, even as the ground reality is that the common man is facing non-stop price rise."

Given the real risks to the inflation trajectory, CPI inflation is likely to remain elevated. According to the RBI, the progress on disinflation is still incomplete.

The RBI is of the view that at present, the risk stems from uncertainties relating to heightened global geo-political risks, financial market volatility, adverse weather events and the recent uptick in global food and metal prices. Hence, the MPC has decided to remain vigilant of the evolving inflation outlook.

So, where are Policy Interest Rates Headed?

The MPC has reiterated that enduring price stability strengthens the foundations of a sustained period of high growth.

Note, that food inflation still has a key influence on the monetary policy actions and stance. It is unlikely that the RBI will give in to the recent slowdown in GDP for Q2FY25 and cut the policy repo rate. A fact is consumption (which accounts for nearly 60% of GDP) is slowing down on account of higher inflation. It is particularly the lower middle class and the middle class who are affected.

If CPI inflation comes down, perhaps the February 2025 bi-monthly monetary policy the RBI may cut the policy rates or may even give it a miss and consider cutting rates in the fiscal year 2025-26.

That said, it appears that we are almost near the peak of the current interest rate upcycle.

To play the interest rate cycle with the expertise of a debt fund manager, Dynamic Bond Funds in the debt mutual funds category are a meaningful choice.

Regardless of the direction in which interest rates move, Dynamic Bond Funds are capable of taking advantage of dynamic market conditions and can invest accordingly to create an all-season portfolio that generates optimal returns.

In other words, dynamic bond funds have the flexibility to adjust their portfolios based on current interest rate conditions.

You see, bond prices and interest rates are interlinked; they have a direct correlation. Various macroeconomic factors, headline inflation, the interest rate cycle, and the central bank's objective affect bond prices.

On the other hand, bond prices and yields share an inverse correlation. Meaning, that when interest rates and yields move up, prices of bonds go down and vice versa.

Understanding the interest rate cycle can be challenging, particularly if you are a novice, and when Dynamic Bond Funds make sense.

What Are Dynamic Bond Funds?

These are a sub-category of debt mutual funds that, as per the SEBI guideline, have the mandate to invest in debt securities across duration, i.e. without a predetermined maturity profile.

In other words, Dynamic Bond Funds have the flexibility to shift investments between short-term, medium-term, and long-term debt securities, taking into consideration the interest rate cycle.

Typically, Dynamic Bond Funds invest in short-term instruments, such as Commercial Papers (CPs) and Certificates of Deposits (CDs), or medium to long-term instruments, such as corporate bonds and gilt securities.

The fund manager allocates to short and longer maturity papers depending on the outlook on the interest rates and overall economy.

If the fund manager of a Dynamic Bond Fund is anticipating interest rates to fall, wherein locking in at higher interest rates is beneficial, higher allocation may be made to longer-duration debt securities. Conversely, in a rising interest rate, the fund manager may allocate more to short or low-duration securities.

Dynamic Bond Funds take a view of the interest rate cycle and bond yields to actively manage their underlying portfolio.

What Is the Investment Objective of Dynamic Bond Funds?

Broadly, the primary investment objective is to provide optimal returns with high liquidity through an actively managed portfolio of high-quality debt securities across varying maturities (short-term and long-term) and money market instruments.

However, there is no assurance or guarantee that the investment objective will be realised.

Are Dynamic Bond Funds Safe?

The performance of a Dynamic Bond Fund largely depends on the fund manager's judgement of the interest rate movement.

If the manager fails to gauge the movement of the interest rate cycle correctly or is unable to hold a portfolio of debt papers that are in line with the rate cycle, or the portfolio quality is compromised, investors may suffer losses.

So, there is an element of credit risk, liquidity risk, interest rate risk and re-investment risk involved when investing in Dynamic Bond Funds. If the fund manager of a Dynamic Bond Fund invests in low-quality debt papers to engage in yield hunting, it may expose its investors to high risk.

So, a lot depends on the portfolio characteristics of the scheme/s you decide to add to your portfolio.

Graph: Risk-Return Spectrum of Debt Mutual Funds

For illustration purposes only

For illustration purposes only

(Source: PersonalFN Research)

By and large, Dynamic Bond Funds are placed at the higher end of the risk-return spectrum. For it to be a rewarding experience for you, selection matters.

The 4 Key Benefits of Investing in Dynamic Bond Funds Are...

1. Reduces interest rate risk through active management of portfolio based on interest rate outlook

2. No need to time the entry and exit in the debt market because fund managers take care of it

3. Offers a solution for your long-term debt investment needs

4. Earns better returns and higher liquidity than Bank FDs

How to Choose the Best Dynamic Bond Funds to Invest in?

Avoid zeroing in on Dynamic Bond Funds to invest in looking at just the past returns because they are in no way indicative of future returns.

Similarly, you cannot go by mutual fund star ratings given based on historical performance, as it isn't foolproof. Star performers are of one particular year, may not remain in the top quartile in the following year. Do watch this video:

[Read: Relying on Star Ratings to Pick Best Mutual Funds? Read This]

To make the best choice, you need to evaluate a host of quantitative and qualitative factors, such as...

√ The portfolio characteristics (who are the issuers, the sector they belong to, the type of debt papers held, the ratings of the respective debt papers, etc.)

√ The allocation to maturity profiles (short, medium, and long-term) of the debt portfolio

√ The Yield-To-Maturity (YTM) and the Modified Duration (MD) of the portfolio

√ The risk ratios (Standard Deviation, Sharpe Ratio, Sortino Ratio, etc.) to understand if the scheme is adequately compensating on a risk-adjusted basis

√ The performance across interest rate cycles

√ The credentials of the fund manager and his team

√ The AUM and expense ratio of the scheme

Also, it would be meaningful to understand the investment ideologies and the investment processes & systems followed at the fund house.

A fund house must have a robust risk management framework in place, and not dependent excessively on the ratings assigned by credit rating agencies.

Ideally, in the attempt to achieve its stated investment objective, a Dynamic Bond Fund should not be investing in low-rate debt securities and engage in yield hunting, or else it could expose you, the investor, to higher risk and jeopardise the liquidity of the portfolio.

It is critical to invest in Dynamic Bond Funds that hold a robust portfolio of securities across maturities and high-quality debt & money market instruments.

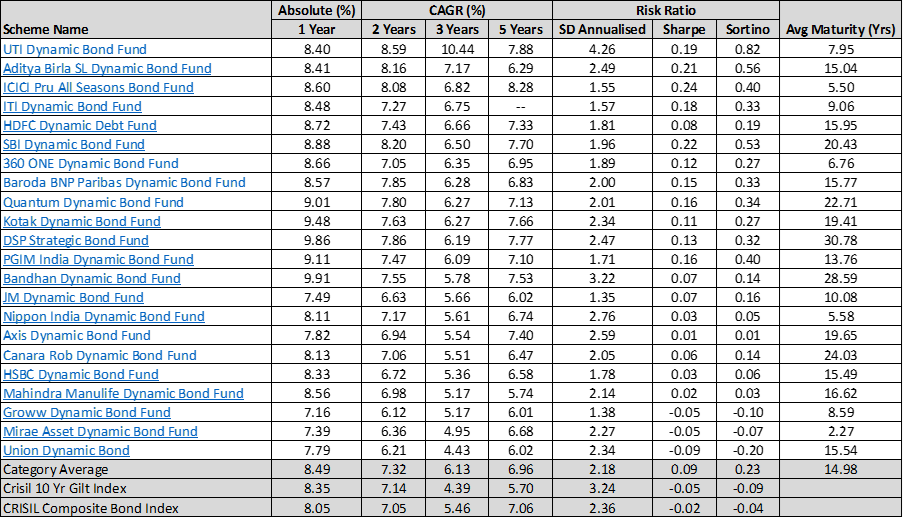

How Have Dynamic Bond Funds Fared?

The category average returns Dynamic Bond Funds for 3 years and 5 years -- which is an ideal time frame to invest in these funds -- have been 6.13% and 6.96%, respectively (as of December 2, 2024).

Table 1: Performance of Dynamic Bond Funds

Data as of December 2, 2024

Data as of December 2, 2024

The list of funds cited here is not exhaustive.

Returns expressed are rolling returns in % and calculated using the Direct Plan-Growth option. Standard Deviation indicates Total Risk and Sharpe Ratio measures the Risk-Adjusted Return. They are calculated over 3 years assuming a risk-free rate of 6% p.a.

*Please note, that this table represents past performance.

Past performance is not an indicator of future returns.

Disclaimer: Quantum Dynamic Bond Fund is a scheme from Quantum Mutual Fund, a group company of Quantum Information Services Pvt. Ltd.PersonalFN is not in receipt of any commission directly or indirectly for suggesting the scheme.

The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

As seen in the table above, certain Dynamic Bond Funds have clocked higher returns than the category average.

That said, one also needs to evaluate the kind of risk (as denoted by the Standard Deviation) taken to generate those returns and the portfolio characteristics. For example, although UTI Dynamic Bond Fund tops the list on 3-year and 5-year CAGR returns, the fund has also exposed its investors to very high risk (Standard Deviation of 4.26%) and is holding relatively shorter maturity papers (Average Maturity of 7.95 years) compared to some other peers in the category, when the interest rate cycle seems to have almost peaked.

Ideally, now Dynamic Bond Funds should have exposure to the longer end of the yield curve. Simply put, be holding quality debt papers with longer maturity.

So, the point to note here is that not all Dynamic Bond Funds are worth your hard-earned money, and therefore, prudent selection matters.

Which Are the Best Dynamic Bond Funds for 2025?

Considering the facets discussed above, the three best Dynamic Bond Funds currently for 2025 are:

-

HDFC Dynamic Debt Fund

-

SBI Dynamic Bond Fund

-

Quantum Dynamic Bond Fund*

* Disclaimer: Quantum Dynamic Bond Fund is a scheme from Quantum Mutual Fund, a group company of Quantum Information Services Pvt. Ltd.PersonalFN is not in receipt of any commission directly or indirectly for suggesting the scheme. Mutual Fund investments are subject to market risks.

These schemes hold worthy portfolio characteristics and are currently holding higher exposure to longer-maturity papers. The fund managers of these schemes are viewing interest rates currently near the peak and expecting them to decline going forward (if inflation pressure eases, allowing the RBI to cut rates).

Here are the details as to why HDFC Dynamic Debt Fund, SBI Dynamic Bond Fund, and Quantum Dynamic Bond Fund, are among the best in the Dynamic Bond Funds category...

Best Dynamic Bond Fund for 2025 #1: HDFC Dynamic Debt Fund

Launched in April 1997 as HDFC High Interest Fund - Dynamic Plan, after SEBI's mutual fund categorisation and rationalisation norms in October 2017, was rechristened as HDFC Dynamic Debt Fund (HDDF). So, effectively the fund has over 27 years of performance track record to its credit.

HDDF adopts a flexible investment strategy, allowing it to invest in instruments of varying maturities based on interest rate trends. By spreading investments across different maturities, HDDF navigates interest rate cycles effectively.

HDDF places a strong emphasis on safety and credit quality (holding mainly AAA-rated and sovereign rate papers), primarily investing in government and quasi-government securities. The fund maintains limited exposure to corporate bonds, favouring Quasi-Government and PSU bonds. Unlike some competitors that seek higher yields through substantial allocation to moderate-rated corporate bonds and other instruments, HDDF avoids investing in moderate to low-rated corporate bonds due to their high credit risk.

That being said, it does take calculated risks by investing in medium to long-term government securities, which carry interest rate risks.

As per HDDF's portfolio as of October 2024, the Average Maturity profile is nearly 16 years. A majority of the fund's investments are in debt papers in the 7 to 10 years maturity bucket, 10 to 15 years, and above 15 years maturity buckets. The portfolio, at present, is positioned in such a manner sensing the opportunity at the longer end of the yield curve.

Table 2: Top 10 Holdings of HDFC Dynamic Debt Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.30% GOI - 19-Jun-2053 |

Government Securities |

SOV |

15.20 |

| 07.18% GOI - 14-Aug-2033 |

Government Securities |

SOV |

12.98 |

| 07.10% GOI - 08-Apr-2034 |

Government Securities |

SOV |

9.06 |

| 07.26% GOI - 22-Aug-2032 |

Government Securities |

SOV |

8.80 |

| 07.25% GOI - 12-Jun-2063 |

Government Securities |

SOV |

7.22 |

| 07.26% GOI - 06-Feb-2033 |

Government Securities |

SOV |

6.51 |

| GOI - 30-Oct-2034 |

Government Securities |

SOV |

5.78 |

| 07.34% GOI - 22-Apr-2064 |

Government Securities |

SOV |

4.65 |

| 06.79% GOI - 07-Oct-2034 |

Government Securities |

SOV |

3.81 |

| REC Ltd.-SR-GOI-VI 08.80% (22-Jan-29) |

Corporate Debt |

AAA & Equiv |

3.36 |

Portfolio data as of October 31, 2024

(Source: ACE MF, data collated by PersonalFN Research)

HDDF typically maintains a streamlined portfolio, holding about 20 to 30 different securities. As per its portfolio as of October 31, 2024, HDDF has 26 securities in its portfolio with top 10 holdings accounting for 77.37% of the fund's portfolio

With a strong focus on G-secs, made up around 83.82% of HDDF's total assets, and about 11.7% is invested in corporate debt instruments. HDDF has 1.64% exposure to REITs and InVITs (namely, the Embassy Office Parks REIT and Bharat Highways InvIT), and 0.23% is held in an Alternative Investment Fund (namely, the Corporate Debt Market Development Fund).

This approach contrasts with some of its popular peers, who tend to allocate more to moderately rated, higher-yielding instruments issued by private entities.

The fund's prudent investment strategy has helped it achieve a decent Yield-to-Maturity (YTM) of 7.10% (which may change as the fund manager buys and sells securities).

For much of its history, where HDDF has functioned as a Medium Term Income Fund and has delivered returns of around 8.1% CAGR since its inception.

Over 3 years and 5 years -- which is an ideal time frame for investing in Dynamic Bond Funds -- HDDF has clocked a decent compounded annualised return of 6.66% and 7.33%, respectively, (as of December 2, 2024), keeping the risk low (as denoted by the Standard Deviation).

Thus, on a risk-adjusted basis, HDDF has fared reasonably well if one considers the Sharpe Ratio and Sortino Ratio of 0.08 and 0.19, respectively (as of December 2, 2024).

HDFC Dynamic Debt Fund has been managed by Mr Anil Bamboli, since February 2004. Mr Anil Bamboli is Senior Fund Manager - Debt at HDFC AMC. With an extensive background spanning more than 29 years in Fund Management, Research, and Fixed Income dealing, he brings a wealth of experience to his role.

Belonging to a fund house known for its disciplined systems and processes, HDDF follows a careful investment strategy. A prudent approach followed in managing the fund has resulted in above-average performance while keeping risks in check.

Best Dynamic Bond Fund for 2025 #2: SBI Dynamic Bond Fund

Launched in January 2004, the SBI Dynamic Bond Fund (SDBF) is one of the oldest schemes in the dynamic bond funds category that has a performance history of over 20 years to its credit.

SDBF's strategy focuses on maximising returns through active management of portfolio duration and diversification across different maturities and issuers. Its portfolio includes investments in sovereign-rated government securities and AAA-rated short to medium-term corporate bonds. This approach helps enhance yields while managing both interest rate risk and credit risk.

SDBF tends to take bold positions on interest rate movements, which has historically benefited investors in clocking optimal returns. The core of its investments is in medium to long-term government securities, which are sensitive to interest rate changes and carry interest rate risk.

However, in its endeavour, SDBF focuses on high-quality instruments from a range of issuers, including government, public, and private entities across different maturity periods.

As per SDBF's portfolio as of October 2024, the Average Maturity profile is over 20 years. A majority of the fund's investments are in the above 15 years maturity bucket, followed by 7 to 10 years, and 10 to 15 years maturity papers. This positioning of the portfolio would benefit SDBF as interest rates in the economy begin to descend.

Table 2: Top 10 Holdings of SBI Dynamic Bond Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 06.79% GOI - 07-Oct-2034 |

Government Securities |

SOV |

22.66 |

| 07.34% GOI - 22-Apr-2064 |

Government Securities |

SOV |

20.86 |

| 07.25% GOI - 12-Jun-2063 |

Government Securities |

SOV |

13.48 |

| 07.18% GOI - 24-Jul-2037 |

Government Securities |

SOV |

8.99 |

| 07.30% GOI - 19-Jun-2053 |

Government Securities |

SOV |

7.87 |

| Highways Infrastructure Trust -SR-III 08.34% (18-Jan-27) |

Corporate Debt |

AAA & Equiv |

4.97 |

| National Bank For Financing Infrastructure And Development SR NABFID2023 - 1 7.43% (16-Jun-33) |

Corporate Debt |

AAA & Equiv |

4.60 |

| National Bank For Financing Infrastructure And Development SR NABFID2025 - 1 7.43% (04-Jul-34) |

Corporate Debt |

AAA & Equiv |

3.07 |

| Indian Railway Finance Corpn Ltd SR-182 07.25% (29-Aug-34) |

Corporate Debt |

AAA & Equiv |

1.22 |

| Power Finance Corporation Ltd. SR-241 7.30% (16-Oct-34) |

Corporate Debt |

AAA & Equiv |

0.76 |

Portfolio data as of October 31, 2024

(Source: ACE MF, data collated by PersonalFN Research)

SDBF hold a compact portfolio of 10 to 15 securities, unlike many of its peers. As of October 2024, SDBF has 12 securities top 10 holdings accounting for 88.48% of the fund's portfolio.

The fund typically invests in a mix of securities issued by the Central and State Governments, Public Sector Undertakings (PSUs), Public Financial Institutions (PFIs), and select private issuers. At present, SDBF has allocated 73.86% of its assets to G-secs, 9.64% to corporate debt issued by PSUs, and 5.88% to corporate debt issued by private issuers.

Hence, SDBF has maintained a high-quality portfolio, primarily focusing on sovereign-rated instruments with medium to long-term maturities, complemented by substantial investments in top-rated corporate debt and money market instruments. At present 10.37% of the fund's total assets are held in cash & cash equivalents.

SDBF's prudent approach has helped it achieve a decent Yield-to-Maturity (YTM) of 7.03% (which may change as the fund manager buys and sells securities).

Over 3 years and 5 years -- which is an ideal time frame for investing in Dynamic Bond Funds -- SDBF has clocked a decent compounded annualised return of 6.50% and 7.70%, respectively, (as of December 2, 2024), keeping the risk low (as denoted by the Standard Deviation).

Thus, on a risk-adjusted basis, SDBF has done quite well if one considers the Sharpe Ratio and Sortino Ratio of 0.22 and 0.53, respectively (as of December 2, 2024).

SDBF has consistently delivered above-average performance, outperforming the Crisil Composite Bond Fund Index and many of its peers. It has provided excellent returns during bond market rallies and maintained steady performance even during challenging times.

SBI Dynamic Bond Fund is currently managed by Mr Rajeev Radhakrishnan and Mr Tejas Soman.

Rajeev serves as the Chief Investment Officer (CIO) - Fixed Income at SBI Fund Management and oversees the Fixed Income desk at the AMC. He is a CFA charter holder with a rich experience in fund management.

Tejas also brings valuable experience to his role possessing over 12 years of combined experience. He is a postgraduate in the securities market from the National Institute of Securities Market.

Best Dynamic Bond Fund for 2025 #3: Quantum Dynamic Bond Fund

Quantum Dynamic Bond Fund (QDBF), launched in May 2015, holds a flexible investment mandate allowing it to adjust allocations across maturities and shift portfolio duration based on the fund manager's outlook on macroeconomic trends and interest rate movements.

QDBF exclusively invests in government securities, treasury bills, and high-quality corporate debt instruments issued by public sector undertakings (PSUs), all selected through a stringent proprietary credit research and review process. Over its 9+ years of existence, the fund has consistently concentrated on top-quality government and quasi-government securities, steering clear of private issuers and the associated credit risks.

Avoiding private issuers has helped QDBF mitigate credit risk. Unlike many other debt funds that pursue high-yield strategies and credit risk bets to top performance charts, QDBF prioritises stability over aggressive returns. The fund's focus on the safety and creditworthiness of issuers makes it an appealing choice for investors with a moderate to high-risk appetite.

This conservative approach to safeguarding investors' capital has kept QDBF under the radar despite its solid track record.

As per QDBF's portfolio as of October 2024, the Average Maturity profile is nearly 20 years and the Modified Duration (MD) of around 10 years. A majority of the fund's investments are in above 15 years maturity bucket, followed by 10 to 15 years, and 7 to 10 years maturity papers. This positioning of the portfolio would benefit SDBF as interest rates in the economy begin to descend.

QDBF operates with a flexible investment mandate, allowing it to allocate 25% to 100% of its assets to G-secs, 0% to 50% to PSU Bonds, up to 75% to CDs/CPs and short-term debt instruments, and up to 100% to Tri-party repos or repos.

Currently, as per its October 2024 portfolio, QDBF has 87.76% exposure to G-secs, 8.98% in corporate debt of PSUs, and 3.03% is held in cash & cash equivalents. Only 0.23% is held in an Alternative Investment Fund (namely, the Corporate Debt Market Development Fund).

Table 3: Top Holdings of Quantum Dynamic Bond Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.30% GOI - 19-Jun-2053 |

Government Securities |

SOV |

31.89 |

| 07.34% GOI - 22-Apr-2064 |

Government Securities |

SOV |

23.55 |

| 07.10% GOI - 08-Apr-2034 |

Government Securities |

SOV |

13.77 |

| 07.18% GOI - 24-Jul-2037 |

Government Securities |

SOV |

9.24 |

| 07.70% Maharashtra SDL - 08-Nov-2034 |

Government Securities |

SOV |

4.69 |

| 07.32% GOI - 13-Nov-2030 |

Government Securities |

SOV |

4.62 |

| National Bank For Agriculture & Rural Development SR-F24 7.68% (30-Apr-29) |

Corporate Debt |

AAA & Equiv |

4.55 |

| Indian Railway Finance Corpn Ltd. SR-150 6.90% (05-Jun-35) |

Corporate Debt |

AAA & Equiv |

4.43 |

Portfolio data as of October 31, 2024

(Source: ACE MF, data collated by PersonalFN Research)

The fund typically maintains a focused portfolio of up to 5 to 15 securities. At present, it has 8 securities in its portfolio comprising 96.73% of its portfolio. This reflects QDBF's concentrated yet high-quality investment strategy.

However, its portfolio, currently dominated by G-Secs across the maturity curve, including some with maturities exceeding way above 10 years, may expose investors to moderate interest rate risk.

QDBF's prudent approach has helped it achieve a decent Yield-to-Maturity (YTM) of 6.97% (which may change as the fund manager buys and sells securities).

Since its inception in May 2015, QDBF has delivered a respectable 7.96% CAGR, as of December 2, 2024.

Over 3 years and 5 years -- which is an ideal time frame for investing in Dynamic Bond Funds -- QDBF has clocked a decent compounded annualised return of 6.27% and 7.13%, respectively, (as of December 2, 2024), managing the risk well (as denoted by the Standard Deviation).

Thus, on a risk-adjusted basis, QDBF has done fairly well if one considers the Sharpe Ratio and Sortino Ratio of 0.16 and 0.34, respectively (as of December 2, 2024). Quantum Dynamic Bond Fund is managed by Mr Pankaj Pathak (since March 2017). The fund has benefitted under his watch. He has adhered to the fund's investment mandate, successfully generating reasonable returns while avoiding unnecessary credit risk, thereby safeguarding investors' interests.

Pankaj has over 4 years of experience in Fixed income investments and research. He holds a Post Graduate Diploma in Banking & Finance from the National Institute of Bank Management (NIBM), Pune, and is a qualified CFA (Chartered Financial Analyst).

Overall, these three Dynamic Bond Funds follow appropriate risk management measures and have rewarded investors. They are from fund houses that follow robust investment processes and systems.

Who Should Invest in the Dynamic Bond Funds?

Dynamic Bond Funds are suitable for investors who want to benefit from both rising and falling interest rate cycles, with a professional debt fund manager doing it for them.

Regardless of the direction interest rates move, they are capable of taking advantage of dynamic market conditions and can invest accordingly to create an all-season portfolio that generates optimal returns.

While Dynamic Bond Funds may face short-term volatility, especially during rising interest rate periods, the impact typically reduces over time, making them suitable for disciplined investors with a long-term outlook of 3 to 5 years and a moderate-to-high risk profile.

It is critical to invest in Dynamic Bond Funds that hold robust portfolio characteristics.

At present, around 25% of your debt mutual fund portfolio could be allocated to some of the best Dynamic Bond Funds.

What Are the Tax Implications of Investing in Dynamic Bond Funds?

All debt funds, including Liquid Funds, with effect from April 1, 2023, the capital gain arising at the time of redemption -- whether short-term (a holding period of less than 36 months) or long-term (a holding period of 36 months and above) -- is also taxed as per investors' tax slab.

[Read: Taxation of Debt Mutual Funds - Here is All You Need to Know]

For NRIs, the capital gains on debt-oriented mutual funds are subject to Tax Deduction at Source (TDS) at the rate of 30% if STCG and 12.5% in the case of LTCG.

If you have opted for the dividend option (now known as the IDCW option), for resident Indians, any dividends from Liquid Funds (under the Dividend Option) are added to the investors' total income and are taxed according to your income-tax slab, i.e., at the marginal rate of taxation.

However, if the dividend amount is more than Rs 5,000, Tax Deduction at Source (TDS) will be first done at the rate of 10%. For NRIs, the dividend/IDCW received is subject to a 20% TDS or at the rate specified under the relevant double tax avoidance agreement, whichever is lower as per section 196A of the Income Tax Act.

To sum-up...

When investing in Dynamic Bond Funds, be mindful of the fact that you will be exposed to interest rate risk, credit risk, and liquidity risk. The level of risk shall depend on how well the fund manager understands and plays the interest rate cycle and the quality of debt papers held.

Therefore, avoid simply looking at past returns and mutual fund star ratings. Invest in Dynamic Bond Funds that follow robust processes and systems and devise a sensible investment strategy.

Be thoughtful in your investment approach and add schemes to your portfolio that are in congruence with your personal risk profile, investment objective, and investment horizon. When in doubt, speak to a SEBI-registered investment advisor.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.