Liquidity Check: Is Your Small Cap Fund Under Pressure?

Vivek Chaurasia

Mar 01, 2024 / Reading Time: Approx. 15 mins

Listen to Liquidity Check: Is Your Small Cap Fund Under Pressure?

00:00

00:00

In a positive development, the market regulator SEBI has taken steps to enhance transparency and safeguard investors in small and mid-cap funds. It has directed the Association of Mutual Funds in India (AMFI) to instruct mutual funds to take steps like moderating inflows, rationalising portfolios to safeguard investor interests, and protecting investors from the advantage to those who redeem early. Additionally, it has also urged mutual funds to provide more information about the risks associated with small and mid-cap funds.

Accordingly, AMFI has directed fund houses to submit stress test results every 15 days, with the first report due by March 15, 2024. Stress tests evaluate a portfolio's liquidity, indicating how quickly the funds can sell their portfolio holdings in case of a market downturn and increased redemption requests.

The significant inflows seen in the mid and small-cap funds have raised concerns about their stability during a sharp market decline or downturn. Mutual funds are now required to perform stress tests and share the results on both their own websites as well as AMFI's website. It would share additional information, such as how long it might take to handle huge redemptions (large withdrawals), the potential impact of big outflows on the fund's value, and the amount of cash and liquid assets they have to manage withdrawals.

While it is good that steps are being taken to control excitement about these high-risk funds, it is a bit too late since these funds have already seen substantial inflows. In fact, some small-cap funds have grown too big to be managed efficiently.

Despite mutual funds being aware of the liquidity challenges within their schemes, it has not been disclosed clearly to investors, leaving them unaware. Providing this information now gives investors more power to compare options and make more informed decisions. Moreover, limiting inflows in mid and small-cap funds might involve restricting fresh money in these funds. Notably, certain small-cap funds have placed limits on new investments but haven't completely stopped more money from coming in, despite being quite large.

Growing Interest Among Mutual Fund Investors in Small-cap Funds...

Small-cap investments have gained popularity among investors because of their high-risk, high-return nature. The impressive track record of small caps in recent years showcases their potential as lucrative and rewarding choices for investors.

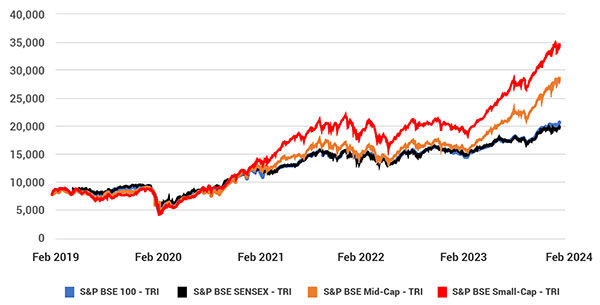

Over the past year, S&P BSE Small-Cap - TRI gained approximately 68%, and S&P BSE Mid-Cap - TRI grew by around 66% (as of February 26, 2024). Looking at a longer span of the past 5 years, the mid-cap index recorded an average annualised return of about 24%, while the small-cap index showed an annualised growth rate of approximately 29%, substantially increasing the value of one's investments in these segments. (See graph 1 below). Note: Past performance is not an indicator of future returns.

Graph 1: The Euphoric Rally in Mid and Small-caps Has Outscored Large-caps

Data as of February 26, 2024

Data as of February 26, 2024

The base is taken as Rs 10,000; Past performance is not indicative of future results

(Source: ACE MF, data collated by PersonalFN Research)

The impressive gains in mid-caps and small-caps have led to a significant rise in the values of mid-cap and small-cap mutual funds. Their outstanding performance and the potential for significant returns have made them a preferred choice for many mutual fund investors, resulting in substantial investments flowing into these funds. The continuous inflow of money into these schemes has also been pushing up stock prices in these segments.

As per data released by the AMFI, the total AUM of Indian mutual funds reached Rs 52.74 lakh crore as of January 31, 2024. This represents an impressive growth of almost 38 times in the last two decades. To put it in perspective, the industry AUM was only 1.45 lakh crore in January 2004, highlighting the significant expansion and progress in Indian mutual funds during this period.

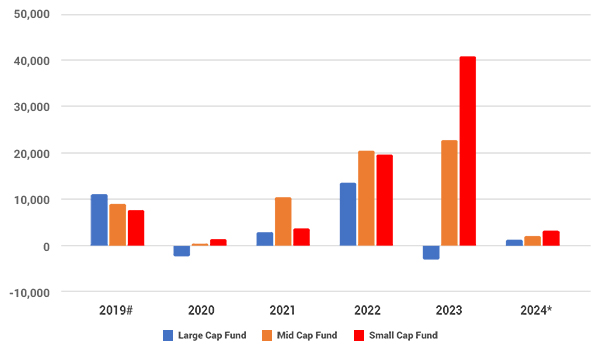

Graph 2: Year-on-Year Inflows in Small Cap Funds, Mid Cap Funds, and Large Cap Funds

The segment-wise data reported by AMFI is from April 2019 onwards.

The segment-wise data reported by AMFI is from April 2019 onwards.

(Source: ACE MF, data collated by PersonalFN Research)

Over time, the Indian mutual fund industry has seen a significant increase in AUM, with substantial net inflows in different fund categories. However, the year 2023 marked a significant shift from the previous years. The huge inflow into equity funds in 2023 was primarily fuelled by substantial investments in small-cap and mid-cap funds. Small Cap Funds saw a notable increase, bringing in over Rs 40,000 Crore in net inflows, while Mid Cap Funds received around Rs 23,000 Crore. On the flip side, Large Cap Funds recorded a net outflow of about Rs 3,000 Crore. The net inflows into mid and small-cap funds indicate a robust and positive trend in investor sentiment towards these segments. (See graph 2 above).

Is this extraordinary shift in interest towards Small Cap Funds justified - do fund managers have a magic wand?

With the eyebrow-raising inflows into Small Cap Funds, concerns would naturally arise.

- Do these Small Cap Funds have the capacity to absorb such substantial inflows?

- Can they effectively handle the ballooning corpus and do justice to investors?

- Will they encounter a liquidity crisis?

- Will they halt new investments or keep exceeding their capacity limits?

These are crucial questions that the industry needs to address. The recent suggestions from the regulator are a move in that direction.

Essentially, asset management companies should function as asset managers, focusing on efficient fund management. However, there has been a shift towards them becoming more like asset gatherers, consistently attracting inflows, sometimes exceeding their optimal capacity.

Think of a BMW or a Maruti car factory - they have a certain capacity, which means they can make a specific number of cars. Now, any car produced within that capacity comes with an assurance. These cars will have the same quality, functionality, and performance because they are produced rationally without any compromise on capacity and quality. In other words, all the cars share identical characteristics till the time they are produced within capacity.

Now, let's relate this to Mutual Fund schemes. Does a mutual fund scheme have a capacity, like a car factory? Can a fund house tell you the capacity of each scheme they offer? This is an important question because it makes us wonder if all the schemes managed by mutual funds justify their 'product characteristics' or if they operate differently from how they should ideally be.

Table 1: Yearly AUM Changes in the Top 10 Small Cap Funds - By Size

| Small Cap Funds (AUM Rs in Cr.) |

Jan-20 |

Jan-21 |

Jan-22 |

Jan-23 |

Jan-24 |

| Nippon India Small Cap Fund |

9,064 |

10,637 |

18,933 |

23,756 |

45,894 |

| HDFC Small Cap Fund |

9,872 |

9,069 |

13,524 |

14,630 |

28,607 |

| SBI Small Cap Fund |

3,493 |

6,594 |

11,288 |

15,292 |

24,862 |

| Axis Small Cap Fund |

2,084 |

3,724 |

8,411 |

11,500 |

19,531 |

| Quant Small Cap Fund |

2 |

108 |

1,517 |

3,134 |

15,664 |

| Kotak Small Cap Fund |

1,592 |

2,539 |

6,811 |

8,573 |

14,426 |

| HSBC Small Cap Fund |

6,123 |

5,349 |

8,167 |

8,672 |

13,981 |

| DSP Small Cap Fund |

5,264 |

5,812 |

8,793 |

9,115 |

13,859 |

| Franklin India Smaller Cos Fund |

7,188 |

5,952 |

7,209 |

7,174 |

11,834 |

| Canara Rob Small Cap Fund |

396 |

669 |

2,027 |

4,709 |

9,586 |

(Source: ACE MF, data collated by PersonalFN Research)

By nature, Small Cap Funds face high liquidity challenges compared to other mutual fund categories. This is due to the low liquidity of small-cap stocks, as they are not easily traded. Despite this, many Small Cap Funds have not taken steps to limit new investments and have grown significantly in the last five years (see Table 1). In the past, some small-cap funds temporarily stopped new investments even when they had just reached Rs 1,000 crores. Now, despite being quite large, they are allowing fresh investments with some limitations. Is this change in capacity driven by competition a point worth considering?

When more investors invest in mutual funds, it creates a large size of assets that need to be invested in the market. In this case, small-cap stocks. When multiple fund managers rush to buy a limited number of stocks, the stock prices go up, increasing the Net Asset Value (NAV) of the funds invested in such stocks. This improves the returns and attracts more investors, leading to more purchases and even higher prices.

On the flip side, if prices start falling during a market downturn, some anxious investors might choose to withdraw their investments. The stock prices drop further as fund managers rush to sell stocks to give back money to the investors, leading to a decrease in the NAV of the fund. This could trigger additional selling from other investors, contributing to increased selling pressure.

Now have these big-sized funds positioned their portfolios well and ready to handle the liquidity challenge? Or will they be able to sell less liquid stocks at throwaway prices, or will they opt to sell the more easily tradable high-quality stocks first, potentially ending up with less liquid and lower-quality ones?

Do not forget that fund managers are humans, and they cannot always perform magic.

The Significance of Liquidity and Its Impact on NAV...

Liquidity is key for investors who want smooth transactions when entering or exiting a fund. Similarly, the NAV is not just a theoretical number but a practical one that should reflect the fund's real transaction (buy/sell) value. This means the reported NAV should nearly match the actual transaction (buy/sell) value, highlighting the importance of transparency in managing funds.

The core idea here is that the assets held by a mutual fund should be easy to turn into cash quickly and efficiently. This ensures a fast and smooth selling process with minimal hassles or costs for investors. Essentially, what investors see in the reported NAV is what they should get when they redeem their investments.

However, when it comes to small-cap funds - which deal with smaller companies - a pressing question arises. Can investors trust that the reported NAV is an accurate representation of the price they will get when redeeming their investment? This question probes deeper into the reliability of reported NAVs, particularly in small-cap funds where market conditions can be more unpredictable.

The Fear of Style Drift!

Sometimes, investors and rating agencies make a mistake by looking too much at how a fund did in the past. Just because a fund has done well before doesn't mean it will do the same in the future. It is like the funds that won last year will win even this year as well - it doesn't always work that way.

One important thing to understand is that what we analyse or assess about a fund based on its past performance might not actually happen in the future. This is because the situation and how a fund is managed can change. In the world of investments, such change is called 'style drift.'

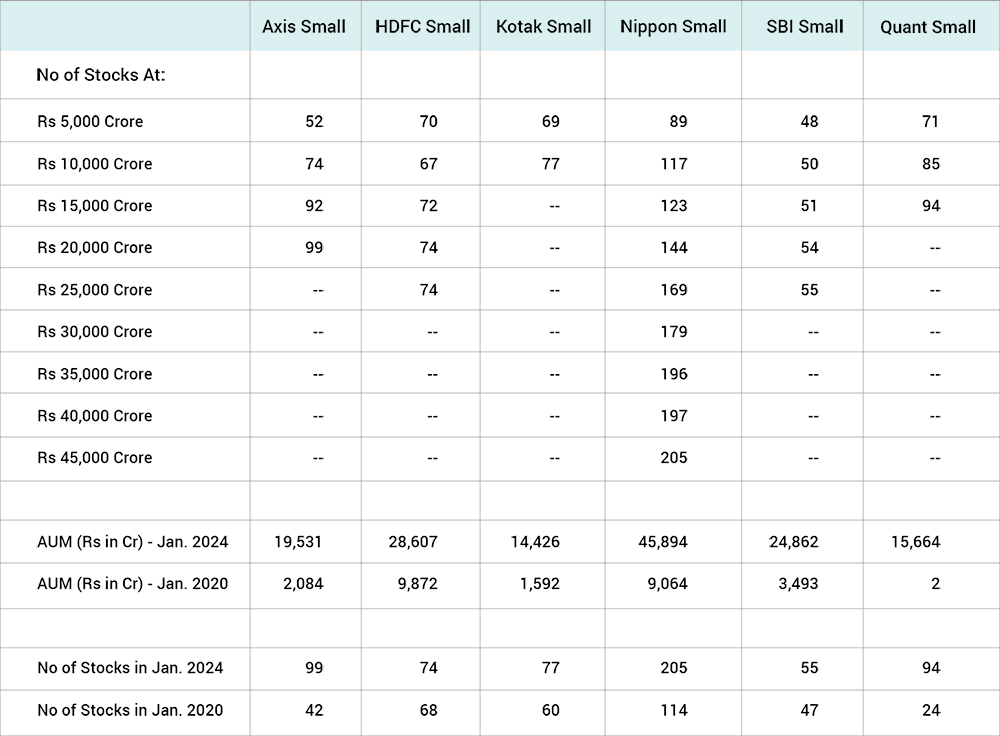

As more and more people invest in the fund, the size (AUM) and type of investments in the fund can change a lot. The fund manager might find it challenging to manage the fund in the same way they did before. They have to adjust things to make room for all the new money. The types and number of stocks they bought might change to handle all the new money coming in. So, it is important to be careful when looking at a fund and consider if its style or way of doing things has changed as it got more popular. (See the Table 2 below)

Table 2: No of Stocks and AUM: Disciplined Approach to Managing Money v/s Gathering AUM?

(Source: ACE MF, data collated by PersonalFN Research)

(Source: ACE MF, data collated by PersonalFN Research)

When the fund's focus shifts from just managing the money it already has to try to get more money from new investors, it can lose discipline and exceed its fair capacity. The increased size of the fund can have an impact on the number of stock holdings in the portfolio (as seen in Table 2 above). When a mutual fund starts facing a capacity challenge and keeps increasing the number of stocks in its portfolio, it can change how the whole thing works and affect its character or how it behaves.

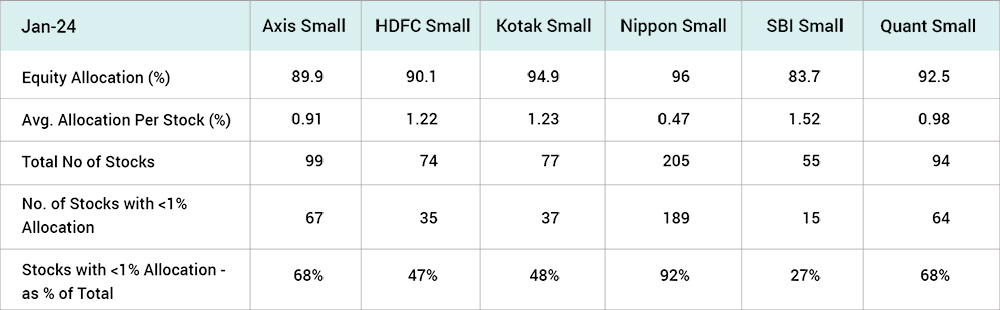

Are some mutual funds using fractional shareholding to hide capacity pressure?

Sometimes, it might seem like the fund believes in what it is investing in. But when we look closely, it could be just a small part of what they have. It is like having a small piece of something instead of a whole one. This might be a way for the fund to handle more money without showing a strong commitment to any specific thing.

Table 3: Owning a Fractional Shareholding Can be a Camouflage to Accommodating More AuM

(Source: ACE MF, data collated by PersonalFN Research)

(Source: ACE MF, data collated by PersonalFN Research)

Owning a fraction or smaller portion of a share allows the fund manager to diversify in various companies. It might be a strategy for managing a substantial amount of money without being fully committed to the goals of any single company. Beware of the long tail that is building up in some funds. Exposure in stocks with less than 1% allocation may be meaningless.

Table 4: Liquidity Analysis of Top 15 Holdings: How many days will it take to exit each of the Top 15 holdings if the scheme gets a maximum of 20% of the average daily turnover of each stock?

Liquidity data for Top 15 holdings - No of Days; If Fund sales account for 20% of Last 12 Months (LTM) Average Trading Volume

Liquidity data for Top 15 holdings - No of Days; If Fund sales account for 20% of Last 12 Months (LTM) Average Trading Volume

(Source: ACE MF, data collated by PersonalFN Research)

When we assess the liquidity of the holdings in a small-cap mutual fund, we essentially examine how efficiently the fund can liquidate or sell each of its stocks. Think of it as how sooner the fund can sell its assets, but with a limitation - practically, it won't be able to sell more than 20% of the trading volume for each stock per day.

The above 'table 4' involves popular small-cap funds and how soon these funds can strategically turn their top stock holdings into cash. Here, I am exploring what happens if these funds decide to sell their top 15 holdings, considering they are limited to selling only 20% of the daily trading volume for each stock. Well, as you can see, some of the popular funds can take more than 100 to 200 days to liquidate a portion of their top holdings. Some stocks might even take almost 10 years to be sold completely (considering 20% of the last 12-month average trading volume). This is much higher than the reasonable fair number of 66 days.

Not all small-cap funds are inherently liquid. It is the responsibility of the asset managers to control liquidity and not go overboard or exceed capacity while gathering assets.

To cap it all...

The recent directive by the market regulator SEBI is a positive and necessary move. The stress test and liquidity analysis of small and mid-cap funds is crucial because it provides insight into how easily or challenging it might be for your small and mid-cap mutual fund to convert its investments into cash when the need arises.

Mutual funds currently do not disclose the portfolio liquidity data, i.e. how easily they can convert their assets into cash. However, if the fund houses begin transparently disclosing this data, it will help investors understand the fund's capacity and how well it can handle liquidity challenges in different market conditions.

For Investors: Be careful when choosing mutual funds, making sure they match your investment plan. Currently, more money is flowing into riskier segments like small-cap, mid-cap, and multi-cap funds.

This trend is worrisome for investors who are now overexposed to small-caps and mid-caps. The volatility in these segments might not match appropriately with their risk tolerance. In the event of a market sell-off, these segments could be seriously affected, posing a big risk for investors with too much allocation to mid and small-cap funds in their portfolios.

I hope that investors who have been very aggressive in their investment approach will proactively review and adjust their portfolios for more stable investments. Doing so would help mitigate potential risks and improve the overall stability of their investment portfolio.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

VIVEK CHAURASIA is the editor of FundSelect and FundSelect Plus, the flagship research services of PersonalFN.

Having over a decade of experience in analysing mutual funds, Vivek understands the functioning of the mutual fund industry very well and applies his financial and analytical skills to closely scrutinize each fund to his satisfaction.

Vivek joined PersonalFN as a Senior Research Analyst in 2009 and quickly adopted the philosophy of our research team, i.e. honest and unbiased research for naive investors who are tired of being mis-sold. Over these years, he has developed a robust fund selection and filtration model - 'SMART Score matrix' that has been tested across various cycles now and constantly looks for a scope to strengthen it further. Vivek follows the principle of safety first when it comes to picking funds for investors. That is the reason why he has a long list of rejected funds as compared to the ones he has endorsed so far.

Vivek is an avid follower of John C. Bogle (the founder of The Vanguard Group and the author of the bestseller book - Common Sense on Mutual Funds: New Imperatives for the Intelligent Investor) and Warren Buffet (one of the most successful investors of all time)

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.