Should You Stop Your SIPs Now Amid Falling Equity Markets

Rounaq Neroy

Feb 18, 2025 / Reading Time: Approx. 9 mins

Listen to Should You Stop Your SIPs Now Amid Falling Equity Markets

00:00

00:00

Worried and anxious about the current volatility in the Indian equity market, where the small and midcaps (SMIDS) in particular have been hammered, investors are now wondering what they should be doing with the existing mutual fund SIPs. Many investors, in panic, have already discontinued or stopped their SIPs.

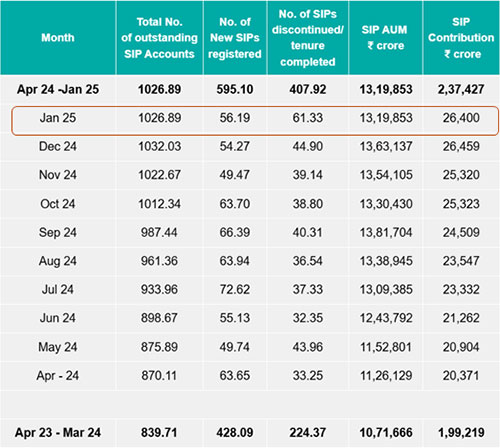

The Association of Mutual Funds in India (AMFI) data for January 2025 reveals that the number of Systematic Investment Plans (SIPs) discontinued has outdone the new SIP registration. This is the first time we are witnessing a reversal in trend since SIPs became household name and today comprise 19.6% of the total mutual fund industry assets.

Table: Number of New SIPs Registered v/s Number of SIPs Discontinued (SIP Count in Lakh)

(Source: AMFI)

(Source: AMFI)

Although SIP contributions have remained consistent, the anxiety of investors is evident, with the marginal drop in inflows for January 2025.

Given that the equity market has been volatile and corrected further from its peak, it wouldn't be unsurprising if SIPs flows decline further for February 2025 and some investors discontinue SIPs. This would more so be the case with first-time equity investors who entered the market during the COVID-19 pandemic times and haven't witnessed longer market cycles.

Many investors are finding their portfolios under pressure with unrealised losses as the market correction unfolds. This is particularly the case if the portfolio is skewed towards the Small Cap Funds and Mid Cap Funds, as their underlying indices -- the BSE Mid-Cap and Small-Cap Index -- have corrected nearly 20% since their respective peak.

Speaking at the 15th IFA Galaxy event, S. Naren, the CIO of ICICI Prudential Mutual Fund highlighting valuation concerns said, "We think it is time to take out lock, stock and barrel from small and mid-caps." He has also challenged the notion that SIP always yields good returns.

Coming from a veteran fund manager, this statement has further frightened investors.

Should You Really Stop SIPs in Equity-Oriented Funds Now?

You see, when SIP-ping into mutual funds, what matters or needs to be considered are two things: 1) when you started the SIP, and 2) how long is your investment horizon.

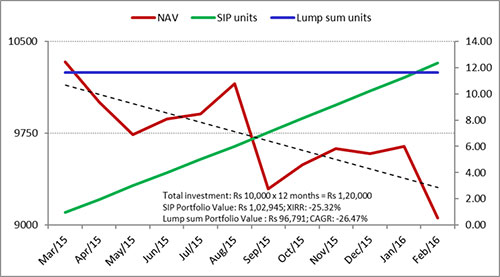

Graph 1: Mutual Fund SIPs Would Work Best in Correction or Bear Phases

NAV based on Nifty 500 - TRI between March 01, 2015, and February 29, 2016

NAV based on Nifty 500 - TRI between March 01, 2015, and February 29, 2016

Lump-sum investment assumed Rs 1,20,000

(Source: ACE MF, data collated by PersonalFN Research)

The graph above depicts how in the corrective phase of the Indian equity markets from March 2015 to February 2016, monthly SIP investments were rewarded better than a lump sum investment. Lump sum investment made during this period witnessed wealth erosion.

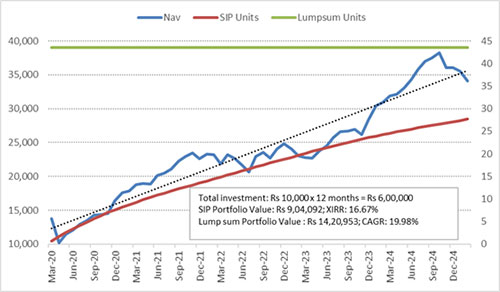

Similarly, during 2018-19 when SMIDs had fallen (while largecaps were resilient), if monthly SIPs were started in a worthy Mid Cap Fund and/or Small Cap Fund, the returns would be quite handsome as of today considering the remarkable rally until the peak of September 2024 and December 2024, respectively.

Graph 2: The result of Starting a SIP In a Market Rally

NAV based on Nifty 500 - TRI between March 01, 2020, and February 14, 2025

NAV based on Nifty 500 - TRI between March 01, 2020, and February 14, 2025

Lump-sum investment assumed Rs 1 lakh

(Source: ACE MF, data collated by PersonalFN Research)

Also, those who started the monthly SIP during the lows of the COVID-19 pandemic when the Indian equity market was relatively inexpensive or had bottomed, need not be much worried. Although lump sum investment made at the low of the pandemic has clocked better compounded annualised returns, the XIRR of 16.6% for SIPs for nearly a 5-year period is decent.

[Read: XIRR vs CAGR in Mutual Funds: Which is the Better Tool to Evaluate Returns]

But the ones who have started their SIP journey recently, say near the peak of the market cap segments, are the ones who need to be worried or careful. They need to ensure the schemes they are SIP-ping into are among the best and most suitable ones, and if that is the case, hold on to their SIP investments for longer.

Do note that while SIPs help in managing volatility, in the present market conditions a 3 to 5 years horizon may not yield good XIRR returns for SIPs. SIPs need to be continued for more than a 5-year horizon -- ideally 10 years or more -- particularly when investing in Small Cap Funds and Mid Cap Funds, whereby one potentially stands to benefit.

A longer investment horizon shall help mitigate the risk with the inherent rupee-cost-averaging feature and potentially add to the power of compounding.

Owing to a variety of factors in play, viz. tariff wars, weak Indian rupee, rising bond yields, geopolitical tension, chances of geoeconomic fragmentation, supply chain disruptions, imported inflation, the slowdown in consumption, subdued corporate earnings of late, higher financing cost, climate risk events, and the fact that valuations of the Indian equity market are expensive, the journey hereon in the equity market is expected to uncertain and volatile. India's Volatility Index (VIX) -- a measure of volatility -- has already spiked.

But then volatility is the very nature of the market. And to manage that, SIPs remain a prudent mode of investing systematically in mutual funds.

If the equity market tumbles further from hereon for whatever reason, the rupee-cost averaging would work in your, the investors' favour. More units will be purchased at lower NAV, and when the market begins to ascend again, it shall compound wealth.

Note that if the equity market continues to consolidate further or sinks by some percentage points, it is important not to get dismayed and discontinue/stop SIP in some of the best mutual fund schemes in your portfolio.

In the past, the Indian equity market has witnessed a variety of negative events, the Harshad Mehta scam (in April 1992), the dot com bubble burst (in March 2000), the Ketan Parekh scam (in March 2001), the great financial crisis of 2008, the Dubai debacle of 2009 (due to global financial crisis), the European debt crisis of 2009-14 (affecting Portugal, Italy, Ireland, Greece, and Spain), the COVID-19 pandemic, Russia invasion of Ukraine, military conflict in parts of Middle East after Hama's attack on Israel in October 2023, and many more. However, despite all these events, the Indian equity market over the long term has scaled highs and generated wealth for investors.

The reason for this is India's strong economy (at the fifth spot in nominal GDP terms) and the fact that it is the fastest-growing major economy and "a bright spot".

So, the point is to stay put and continue SIPs in the best and most suitable mutual funds with due importance to time in the market.

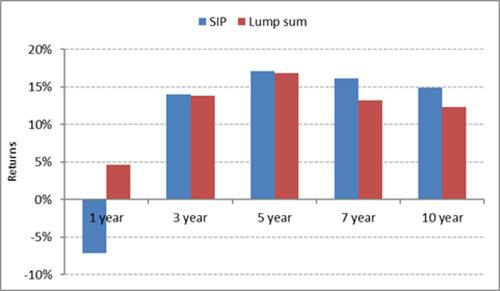

Graph 3: Sips Have Worked Better as Opposed to a Lump Sum Over Longer Time Frames

Data as of February 14, 2025

Data as of February 14, 2025

Returns based on investment in Nifty 500 - TRISIP returns are XIRR, while for lump sum investment it's CAGR.

(Source: ACE MF, data collated by PersonalFN Research)

The graph 3 vindicates that over the longer term, SIPs have delivered positive returns over the long-term - 5 years and more.

SIPs make timing the market irrelevant and add the needed investment discipline to accomplish your envisioned financial goals.

To conclude...

SIPs can prove rewarding as long as the underlying schemes are among the worthy ones, and you, the investor, are contributing meaningfully in the endeavour to achieve your envisioned financial goal/s.

In a volatile or falling market, do not commit the mistake of discontinuing or pausing SIPs. Doing so shall get in the way of rupee-cost averaging, apply brakes on the process of power of compounding, and derail achieving the envisioned financial goals.

That being said, when you are nearing your goal horizon, gradually reduce exposure to equities as an asset class and invest in a more stable and less risky investment avenue, such as bank deposits, small saving schemes, and some money in Liquid Funds.

Make sure your mutual fund portfolio is optimally structured in line with your personal risk profile, the broader investment objective, the financial goal/s you are addressing, and the time in hand to achieve those goals.

Keep in mind, that your investment temperament, strategy, and asset allocation shall pave the path to financial success. So, be a thoughtful investor.

Happy Investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.