Will RBI Cut the Policy Repo Rate Again in April 2025 as CPI Inflation for February Falls

Rounaq Neroy

Mar 18, 2025 / Reading Time: Approx. 10 mins

Listen to Will RBI Cut the Policy Repo Rate Again in April 2025 as CPI Inflation for February Falls

00:00

00:00

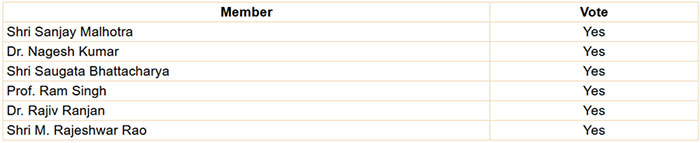

It was the first time in almost five years that the six-member Monetary Policy Committee headed by new RBI governor, Mr Sanjay Malhotra, cut the policy repo rate and consequently the Standing Deposit Facility (SDF) rate, the Marginal Standing Facility (MSF) rate and the Bank Rate, stood adjusted.

All six members of the MPC unanimously took these decisions assessing the current and evolving macroeconomic situation.

Table: Voting on the Resolution to Reduce the Policy Repo Rate to 6.25%

(Source: Minutes of the Monetary Policy Committee Meeting, February 5 to 7, 2025)

(Source: Minutes of the Monetary Policy Committee Meeting, February 5 to 7, 2025)

These decisions were taken in consonance with the objective of achieving the medium-term target for Consumer Price Index (CPI) inflation of 4.00% within a band of +/-2.00% while supporting growth.

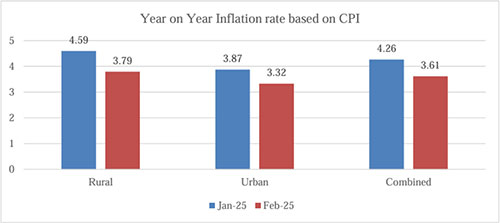

Now the CPI inflation for February 2025 (data released in March 2025) has plunged to 3.61%. It is the lowest year-on-year inflation after July 2024.

Graph 1: Retail Inflation for February 2025 Has Cooled Off

(Source: MOSPI)

(Source: MOSPI)

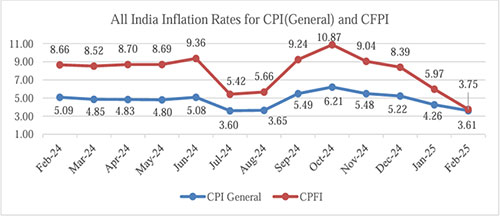

The key reason behind the CPI inflation cooling is that food prices across India (urban and rural) eased to 3.75% (provisional) showed the Consumer Food Price Index (CFPI). Several vegetables, pulses, and protein-rich foods such as eggs, meat and fish, as well as spices, have reported a drop.

Graph 2: Lower Food Prices Helped CPI Inflation Ease

(Source: MOSPI)

(Source: MOSPI)

The year-on-year fuel & light inflation rate for February 2025 (for both urban and rural India) was at -1.33 % versus -1.49% in the previous month.

The core inflation -- which excludes food and fuel - rose to 4.05% in February 2025 compared to 3.76% in the previous month.

It is for the first time in six months that the CPI inflation is below the RBI's 4.00% target. The question therefore is whether the RBI will now be nudged once again to reduce the policy rates.

Path to Interest Rates

Well, the expectation is that the central bank will cut rates by around 75 basis points (bps) in CY 2025. Of that, a 25 bps cut has been already done in the last bi-monthly monetary policy meeting held in February 2025.

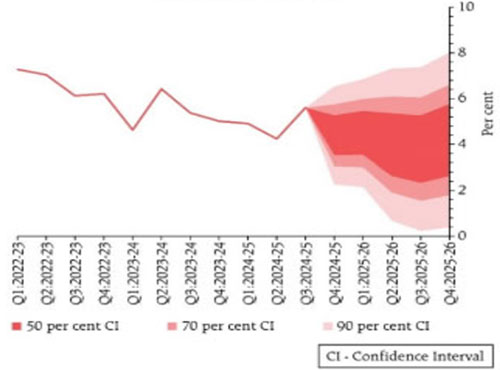

The RBI is expecting core inflation to rise but remain moderate. However, continued uncertainty in global financial markets coupled with volatility in energy prices and adverse weather events presents upside risks to the inflation trajectory.

Graph 3: RBI's Quarterly Projection of CPI

(Source: Monetary Policy Statement, 2024-25, February 5 to 7, 2025)

(Source: Monetary Policy Statement, 2024-25, February 5 to 7, 2025)

At present, items such as coconut oil (54.48%), coconut (41.61%), gold (35.56%), silver (30.89%) and onion (30.42%) have reported the highest retail inflation at all India levels in February 2025.

Besides, there is the risk of 'imported inflation', that is from goods imported from other countries. Imported inflation has already surged from 1.3% in June 2024 to 31.1% in February 2025, driven by rising prices of precious metals, oils, fats, and chemical products. Given Donald Trump's tariff tantrums and reciprocal tariffs, the risk of geoeconomic fragmentation and supply chain bottlenecks, imported inflation would continue to be a cause of concern for the RBI.

That being said, taking courage from the fact the CPI inflation is below the 4.00% target, the RBI may cut the policy repo rate by another 25 bps in the ensuing April 2025 bi-monthly monetary policy for 2025-26 (scheduled from April 7 to 9, 2025) to support GDP growth and provide a fillip to the capex expansion and industry at large.

Most members of the MPC, in the minutes of the last bi-monthly monetary policy, have expressed concerns about a slowdown in India's growth, in particular, the weakness in the manufacturing sector, subdued private consumption (due to a low growth rate of real wages), and the potential effects of Trump's protectionist policies on India's economy. Here's what RBI Governor Mr Sanjay Malhotra stated in the minutes of the February 2025 bi-monthly monetary meeting:

"In a world order dominated by continuing geopolitical tensions and elevated trade and policy uncertainties, monetary policy, as the guardian of macroeconomic and financial stability, is traversing through a challenging time. It has to balance a multitude of pressure points and continuously evolving policy trade-offs. Stronger policy frameworks and robust macro fundamentals remain the key to resilience and fostering overall macroeconomic stability. Domestically too, there is a need to preserve the high growth momentum, while maintaining price stability, necessitating monetary policy to use various policy instruments to maintain the inflation-growth balance."

With the stance of the monetary policy kept neutral, the RBI has the flexibility to respond to the evolving macroeconomic environment.

If the RBI cuts the policy repo rate once again in the April 2025 bi-monthly monetary policy, the interest rate-sensitive sectors and themes, such as housing, automobile, and consumption among others are likely to benefit. Also, for the equity market, it would be a positive move provided the ensuing CPI inflation reading remains within the RBI's comfort range.

[Read: RBI's Rate Cut and Impact on Key Sectors of the Indian Economy]

Investment Strategy to Invest in Debt Mutual Funds Now

At the current juncture, it would be an opportune time to invest in Medium-to-Long Duration Debt Mutual Funds, wherein the maturity profile of these funds should be up to 5 years or so with G-secs around 30%. When investing in these funds, keep an investment horizon of 3 to 5 years whereby you benefit from higher yield and unlock the capital growth. However, it is best to invest in these funds in a staggered manner.

For an investment horizon of 2 to 3 years, you may consider investing in some of the best Banking & PSU Debt Funds. At present, around 30% of your debt mutual fund portfolio could be allocated to some of the best Banking & PSU Debt Funds.

If you have a shorter investment horizon of 1 to 2 years, consider investing in the Ultra-Short Duration Funds and Short Duration Funds, that are having worthy portfolio characteristics, particularly holding higher allocation to government and quasi-government securities, and less of private issuers and, therein too, the highly rated ones only.

[Read: Best Mutual Funds for Short Term Investments]

If you have an investment horizon of a few months or up to a year, it would be better to stick to some of the best Liquid Funds having the least or no exposure to private issuers.

Keep in mind that investing in debt mutual funds, in general, is not risk-free, and hence choose the safety of the principal over returns.

Avoid investing in debt funds that engage in yield hunting to clock higher returns. For this purpose, closely look at the portfolio characteristics of the scheme rather than only the past returns that are in no way indicative of how the mutual fund scheme would fare in future.

[Read: Best Debt Mutual Fund Categories for 2025]

Should You Do SIPs in Debt Mutual Funds?

A Systematic Investment Plan (SIP) makes sense only if the investment time horizon is longer and depends on the sub-category of the debt mutual fund one chooses to invest in.

Typically, SIPs in Medium to Long Duration Debt Funds, Long Duration Funds, Gilt Funds, and Dynamic Bonds, where the volatility in their NAV movement could be on the higher side (due to their inherent traits and portfolio characteristics), could make sense.

However, for shorter-maturity funds like Overnight Funds, Liquid Funds, Ultra Short Duration Funds, and Money Market Funds, SIPs do not make sense.

By and large, keep in mind that the SIP returns in debt funds would be muted in contrast to equity mutual funds. In other words, the rupee-cost advantage does not necessarily work to the investor's best advantage in case the NAV of the debt mutual funds does not move up or down much.

Invest Strategy to Invest in Bank Fixed Deposits

Certain banks have already reduced interest rates on deposits after the 25 bps policy repo rate cut by the RBI in February 2025.

Before we see the transmission of the policy rate cut further and the banks cut their fixed deposit rates, it would be sensible to invest in bank fixed deposits. Senior citizens can benefit from an additional 0.50% interest rate on bank FDs.

Exercise caution when considering banks offering significantly higher interest rates than the market average, as higher returns often come with higher risks. It would be prudent to diversify your investment in FDs across banks rather than keeping money in only one or two. This helps to mitigate the risk.

[Read: DICGC Insurance Cover to Increase. Here's How You Could Maximise Bank Deposit Insurance]

To make the most of your investment and maintain liquidity, Fixed Deposit laddering is a smart strategy. It involves spreading your FD investments across multiple maturity tenures or maturity buckets (e.g. 6 months, 1 year, 2 years) rather than locking all your funds in a single FD. With this approach, you can potentially secure higher returns while ensuring liquidity to cover emergency expenses without needing to prematurely break long-term deposits.

FDs with tenures of 1 year or 2 years provide a meaningful balance of returns, liquidity, and flexibility as per your needs.

If you need access to money during emergencies, choose short-term deposits (of 6 months to 18 months tenure).

To conclude...

With the RBI likely to cut the policy repo rate by 25 bps in the April 2025 bi-monthly monetary policy, make sure your investment portfolio is well structured -- whether it is equity mutual funds, debt mutual funds, and/or bank fixed deposits -- and make sure you are investing sensibly.

Align with your investments in congruence with your risk profile, broader investment objective, the financial goals you wish to address, the time in hand to achieve those goals, and your liquidity needs.

Following a thoughtful approach and devising an investment strategy, paves the path to prosperity, success, and security.

Happy investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.