Hurry! Here’s Your Guide to Last-Minute Tax Saving Options Under Section 80C

Mitali Dhoke

Mar 04, 2024 / Reading Time: Approx. 10 mins

Listen to Hurry! Here’s Your Guide to Last-Minute Tax Saving Options Under Section 80C

00:00

00:00

The end of the financial year 2023-24 is fast approaching, and the familiar feeling of tax deadline anxiety may be creeping in. The Income Tax Act 1961 has availed various deductions and exemptions under different sections, aiming to minimise one's tax burden.

The most popular one amongst taxpayers is Section 80C. However, if you have not yet utilised the full benefit of Section 80C deductions for tax savings, you might feel the pressure. Section 80C remains your ally, offering a lifeline for tax savings even in the eleventh hour.

Don't worry! Whether you have meticulously planned your investments throughout the year or facing a last-minute scramble due to unforeseen circumstances, this article is your roadmap to maximising your deductions under Section 80C.

Even at this last stage, since we are already into the last month of the Q4 for FY 2023-24, there's still time to make smart choices and maximise your tax benefits.

We will delve into various last-minute investment options that qualify for Section 80C deductions, allowing you to make informed choices based on your risk appetite and financial goals. From understanding your remaining deduction limit to prioritising options and various suitable tax-saving investment options, this guide will equip you with the knowledge and strategies to navigate the final stretch and make the most of this valuable tax benefit.

We are on WhatsApp! Join our exclusive WhatsApp channel.

Remember, even if the deadline looms, taking swift action and making informed decisions is key to transforming this last-minute dash into a successful tax-saving mission.

While it's always recommended to plan your investments strategically at the beginning of every financial year to avoid unforeseen circumstances, procrastination can lead to rushing in the last quarter.

[Read: Why Invest in Tax-Saving Mutual Funds at the Start of the Financial Year]

However, this doesn't mean you have to miss out on the tax benefits, it's important to remember that last-minute planning is still better than not planning at all.

Understanding Section 80C:

Section 80C of the Income Tax Act 1961 provides a much-needed respite for taxpayers by allowing deductions for investments made in various avenues. It allows for deductions of up to Rs 1.5 lakh for investments made in various schemes, effectively reducing your taxable income and lowering your tax liability.

Here's a few tax-saving strategies that you may consider at the eleventh hour:

1. Assess Your Remaining Section 80C Limit:

The first step is to determine the unused portion of your Rs 1.5 lakh limit under Section 80C. You can easily access this information from your previous tax return; knowing the remaining amount will guide your investment choices.

For instance, you may have already invested in any of the tax-saving instruments (ELSS, PPF, NSC, SSY, SCSS ULIPs, etc.) covered under Section 80C. If you have already invested around Rs 50,000/- in such tax-saving avenues, you are left with an available deduction of Rs 1 lakh for the current fiscal year.

2. Explore Last-minute Tax-saving Investment Options:

While long-term investment planning is crucial, several options cater specifically to those seeking last-minute tax savings under Section 80C. Some popular options to consider:

Conventional Options for Risk-averse Taxpayers:

-

Public Provident Fund (PPF): This government-backed savings scheme offers guaranteed returns and tax benefits. However, it comes with a lock-in period of 15 years, making it less suitable for immediate requirements.

-

National Savings Certificate (NSC): Offered by post offices, NSCs provide fixed interest rates and tax benefits. Depending on the chosen maturity (1 to 5 years), they come with varying lock-in periods.

-

Tax Saving Fixed Deposits (FDs): There are two types of FDs: regular and tax-saver. These are fixed deposits offered by banks specifically for tax-saving purposes. They offer fixed returns and tax benefits but come with a lock-in period of 5 years. Banks do not allow premature withdrawals in tax-saver fixed deposits.

On the contrary, regular FDs do not offer tax-saving benefits; they come with an investment tenure that ranges from 7 days to 10 years.

[Read: Tax Savings in 2024: 5 Key Tax Efficient Investment Strategies]

For Taxpayers Seeking Growth Potential - Equity Linked Savings Scheme (ELSS)

ELSS are a category under equity mutual funds that invest predominantly in the capital market and choose stocks with different market capitalisations. They offer the potential for high long-term capital gains while allowing tax deductions under Section 80C. However, they also carry inherent market risks.

If you want to invest in mutual funds and save income tax, ELSS should be your go-to option. ELSS stands out from traditional tax-saving options due to its potential for higher returns and greater flexibility.

While traditional options offer guaranteed returns and security, they typically fall short of inflation in the long run. On the other hand, ELSS invests in the stock market, offering the potential for significantly higher returns that can outpace inflation and grow your wealth over time. Additionally, ELSS boasts a shorter lock-in period of 3 years compared to the 15 years of PPF or 5 years of FD and NSC. This allows better liquidity when needed while still providing significant tax benefits. ELSS is suitable for investors with long-investment horizon and who are comfortable with taking on some risk in exchange for the potential for higher returns.

[Read: Why ELSS Is Your Best Choice to Build Wealth and Save Tax]

However, when it comes to equity schemes, there are certain risks involved. Note that ELSS carries market risk like other equity investments, and their returns can fluctuate. As a result, you may not solely invest in ELSS for tax benefits without considering your risk tolerance and investment goals.

Understanding the tax benefits and investment risks can help you make informed decisions about incorporating ELSS into your tax-efficient investment strategy.

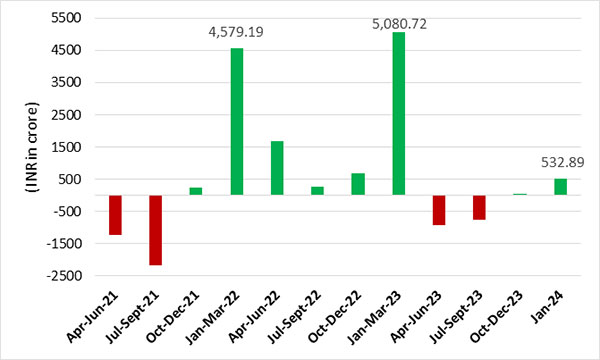

Graph: Net Inflows/Outflows in ELSS Past 3 Years Data

Data as of March 04, 2024

Data as of March 04, 2024

(Source: AMFI, data collated by PersonalFN Research)

The Association of Mutual Funds in India (AMFI) released quarterly statistics which show that traditionally, the final quarter of each fiscal year (Jan to March), which is the tax season, has seen larger net inflows in the ELSS category of equity mutual funds, making it a popular tax-saving option amongst taxpayers.

Several reasons have contributed to the decline in inflows, including increased interest rates, a declining rupee, geopolitical unrest, the broader market's poor performance compared to other asset classes, and investor risk aversion brought on by uncertain economic conditions. Despite the heavy outflows at the beginning, the Jan-March Q4 for FY 2021-22 received high net inflows of Rs 4,579.19 crore.

Moreover, 2022 proved to be a turning point for ELSS. Between April and December 2022, the category saw a favourable upswing, with active ELSS schemes drawing net inflows. This change was brought about by the market's improved performance as well as investors looking for opportunities to build long-term wealth through equities. Despite the market volatility in Q4 of FY 2022-2023, the ELSS category had strong net inflows of Rs 5080.72 crore.

The year 2023 witnessed volatility in the ELSS category, coupled with factors like potential profit-booking by investors after a strong rally in 2022, which might have also contributed to the outflows in Q2 (July-Sept 2023). According to the AMFI monthly data, ELSS had an increase in net inflows for January 2024; however, when the financial year comes to an end, a more precise picture of ELSS's overall 2023 performance will become apparent.

Notably, investors seeking to reduce their tax burden increase their investments in ELSS over the last three months or fourth quarter of the financial year. Moreover, the new tax regime does not offer any tax deductions under Section 80C for ELSS and a few other investments.

[Read: 7 Top-performing ELSS (Tax Saving Mutual Funds) with High Returns on 10-Year SIP]

However, Investors must shift their perspective to see ELSS as a wealth-creating tool rather than just a tax-saving option. During the high volatility periods, ELSS ensures the discipline of staying put for the investment horizon, ensuring the investor reaps long-term investment benefits because of the 3-year lock-in.

When investing in ELSS, one may consider the SIP route. It helps you rupee-cost average your investment, instils regular investing habits, mitigates market volatility and helps build wealth over the long term.

3. Consider Additional Deductions:

Beyond the typical investments, other avenues can contribute to maximising your deductions under Section 80C:

-

Employee Provident Fund (EPF) Contributions: If you are a salaried individual, your employer contributes a percentage of your salary to the EPF, which qualifies for tax deduction. Ensure you have utilised the full contribution limit.

-

Life Insurance Premiums: Premiums paid for life insurance policies for yourself, spouse, and dependent parents are eligible for deduction under Section 80C, subject to certain limits.

-

Tuition Fees: School fees paid for up to two children qualify for deduction under Section 80C. This can be a significant benefit for parents.

Don't rush into any investment decisions solely to meet the deadline. Conduct thorough research, understand the associated fees and risks, and consult a financial advisor if needed, ensuring the chosen option aligns with your overall financial plan.

[Read: 7 Tax Planning Checks to Carry Out Before You File ITR…]

For new investments, timely initiation is crucial to ensure they are reflected in your tax filings for the current financial year. If you are short on time, consider online investment platforms that offer quick and convenient access to various tax-saving options.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

MITALI DHOKE is a Research Analyst at PersonalFN. She is an MBA (Finance) and a post-graduate in commerce (M. Com). She focuses primarily on covering articles around mutual funds including NFOs, financial planning and fixed-income products. Mitali holds an overall experience of 4 years in the financial services industry.

She also actively contributes towards content creation for PersonalFN’s social media platforms in the endeavour to educate investors and enhance their financial knowledge.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.