Is the Revised New Tax Regime Truly Beneficial for You? Find Out Here…

Mitali Dhoke

Jul 25, 2024 / Reading Time: Approx. 10 mins

Listen to Is the Revised New Tax Regime Truly Beneficial for You? Find Out Here…

00:00

00:00

The Modi 3.0 full Budget 2024, presented on July 23rd, brought significant changes to the tax regime, affecting taxpayers across different income brackets. The amendments aim to simplify tax compliance, provide clarity, and offer choices that can maximise taxpayers' benefits.

Finance Minister Ms. Nirmala Sitharaman announced changes to the new income tax regime during the Union Budget 2024 presentation, providing some relief to taxpayers.

As a tax-paying citizen in India, you must be already aware of the recent revision to income tax slabs in India. Under the New Tax Regime, there have been several changes.

The Old tax regime versus the New tax regime debate is currently abounding. So, in addition to covering the technicalities of the new tax regime slabs, we will be comparing the two regimes to make the differences clear to you.

Understanding the Changes in New Tax Regime as per Modi 3.0 Budget 2024

The recent 2024 budget introduced several significant changes to the New Tax Regime, making it more attractive and competitive compared to the old regime. The standard deduction for salaried employees is proposed to be increased from Rs 50,000/- to Rs 75,000/-.

[Read: New v/s Old Tax Regime: Which One Should You Opt for After Modi 3.0 Budget?]

Similarly, the deduction on family pension for pensioners is proposed to be enhanced from Rs 15,000/- to Rs 25,000/-. This will provide relief to about four crore salaried individuals and pensioners. Plus, the deduction on employer's NPS contribution for private sector employees hiked from 10% to 14% of the employee's basic salary.

Moreover, in the New tax regime, the tax rate structure is proposed to be revised as follows:

| Net Taxable Income |

Income Tax Slab Rate for FY 2023-24 |

Net Taxable Income |

Income Tax Slab Rate for FY 2024-25 |

| Rs 0 - 3 lakhs |

Nil |

Rs 0 - 3 lakhs |

Nil |

| Rs 3 - 6 lakhs |

5% |

Rs 3 - 7 lakhs |

5% |

| Rs 6 - 9 lakhs |

10% |

Rs 7 - 10 lakhs |

10% |

| Rs 9 - 12 lakhs |

15% |

Rs 10 - 12 lakhs |

15% |

| Rs 12 - 15 lakhs |

20% |

Rs 12 - 15 lakhs |

20% |

| Above Rs 15 lakhs |

30% |

Above Rs 15 lakhs |

30% |

(Source: IndiaBudget.gov.in)

As a result of these changes, a salaried employee in the new tax regime stands to save up to Rs 17,500/- in income tax.

Under the old and new tax regimes, a surcharge is imposed on the total income tax payable when a taxpayer's taxable income surpasses specific thresholds. If the taxable income exceeds Rs 50 lakh, a surcharge is applicable in both tax structures. It's important to note that there are varying surcharge rates based on different income brackets.

Ever since the new tax regime was proposed, many have been debating as to which tax regime is better: the old one with deductions or the new one without them? The answer is relative. One tax regime cannot be universally beneficial for all.

Your income, its type, available deductions, and exemptions determine which tax regime would give you better tax benefits. You should calculate your tax liability using both regimes, and the regime which gives you the lowest tax liability should be chosen depending on your requirements.

Additionally, acknowledging the concept of the Break-Even point is essential for taxpayers trying to decide which regime to opt for, as it helps identify the income threshold where neither regime offers a tax advantage over the other. Understanding this break-even point can simplify decision-making, allowing taxpayers to optimise their tax outgo based on their income and investment behaviour.

How the Break-Even Point helps in Tax Liability Calculation

The break-even point is influenced by several factors, including the applicable tax slabs, available deductions, and exemptions under the old tax regime.

For most taxpayers, the Old tax regime allows for various deductions (such as those under Section 80C for investments, Section 80D for medical insurance, etc.) that reduce taxable income. In contrast, the New tax regime offers lower tax rates but with limited deductions and exemptions.

The example above has shown that the break-even or tax-neutral amount of deductions to be claimed such that tax payable in both regimes is equal will vary depending on the income level. The break-even point can be explained as deductions that must be claimed in the old tax regime from the gross taxable income so that tax payable in both old and new tax regimes becomes the same.

Break-even point: (Gross taxable income - deductions) = Tax payable in both tax regimes is the same

Here is a table outlining the minimum deduction amounts that taxpayers at various gross taxable income levels need to claim to equalise their income tax liability under the old and new tax regimes, thus identifying the break-even deductions.

| Gross Income of an Individual |

Minimum deductions /

Break-even Levels Required under the Old tax Regime for FY 2024-25 |

Equal Tax Outgo in Both Regimes as per FY 2024-25 |

| 8,00,000 |

2,25,000 |

28,600 |

| 9,00,000 |

2,75,000 |

39,000 |

| 10,00,000 |

3,18,750 |

50,700 |

| 11,00,000 |

3,43,750 |

66,300 |

| 12,00,000 |

3,68,750 |

81,900 |

| 13,00,000 |

3,87,500 |

98,800 |

| 14,00,000 |

3,87,500 |

1,19,600 |

| 15,00,000 |

3,87,500 |

1,40,400 |

| 16,00,000 |

4,50,000 |

1,63,800 |

| 17,00,000 |

4,50,000 |

1,95,000 |

*The revised tax rates as outlined in the full budget for FY 2024-25

are used to calculate the tax outgo under the New Tax Regime.

*The standard deduction of Rs 75,000/- under the New Tax Regime,

as specified in the full budget for FY 2024-25, has been taken into account.

*Cess at 4% is included in final tax liability.

(This is just for illustration purpose)

(Source: PersonalFN Research)

For instance, consider a taxpayer with an annual income of Rs 10,00,000. Let's calculate the tax liability under both regimes and determine the break-even point by including standard deductions and other exemptions available under the Old regime.

Under the New Tax Regime, with the revised tax rates, the tax liability is Rs 50,700/-. In contrast, under the Old Tax Regime (with unchanged tax rates), the tax liability is Rs 70,200/-, and the new regime with lower tax liability seems suitable for the taxpayer.

Now, to equalise the tax liability under both regimes, the taxpayer would need to claim minimum deductions totalling Rs 3,18,750/-. This includes a standard deduction of Rs 50,000/-, investments under Section 80C amounting to Rs 1.50 lakhs, and the remaining Rs 93,750/- could be for insurance premiums, interest on a home loan, and other eligible deductions/exemptions.

Therefore, in this example, the break-even point is defined as the minimum amount of deductions required under the old tax regime to equalise the tax liability with that of the New tax regime.

From the above table, we can see that once the gross income crosses the threshold of Rs 13 lakh, the minimum deduction of Rs 3,87,500/- remains constant. This is because the income tax rate of 20% remains constant for income slabs from Rs 12 to 15 lakhs under the New tax regime.

Consequently, the minimum deduction of Rs 4,50,000/- remains constant after gross income crosses the Rs 15 lakhs threshold, as the income tax rate of 30% is constant for income of Rs 15 lakhs and above under the New tax regime.

Under the Old tax regime, the income tax rate of 30% becomes constant once income exceeds Rs 10 lakhs. Do remember that surcharges are levied when taxable income exceeds Rs 50 lakh. Hence, for those incomes, the minimum deduction amount will vary.

[Read: Modi 3.0 Budget 2024-25: Here's How Ms Sitharaman's Proposals Impact Your Personal Finance]

Which Tax Regime Should You Opt for After the Modi 3.0 Budget 2024 Announcements?

The New tax regime offers simplified tax slabs with lower rates but eliminates most exemptions and deductions. It includes a standard deduction of Rs 75,000 and is designed for those who prefer a straightforward tax filing process without the need for extensive investment in tax-saving instruments.

On the other hand, the Old tax regime, with unchanged tax rates, still provides numerous deductions under sections like 80C, 80D, and others. This regime can be advantageous for individuals who have significant investments in tax-saving schemes, home loans, or insurance premiums.

Let us compare with an example to identify which tax regime will be beneficial for you, and it provides a better perspective on which one should you opt for:

An individual's taxable income is obtained after deducting various deductions under Chapter VI A of the Income Tax Act 1961. i.e. the deduction ranging from Section 80C to 80U from the Gross Total Income (GTI) .

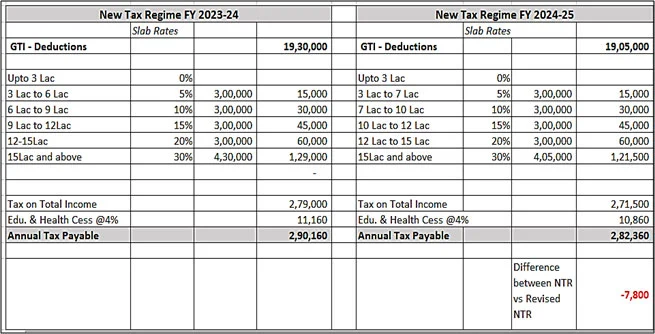

In the given example, the gross annual income of an individual is considered to be Rs 19.80 lacs per annum and we have calculated the taxable income after considering commonly used deductions such as: Standard deduction u/s 16, Children education allowance u/s 10(14), Professional tax u/s 16(iii), Mediclaim u/s 80D, Housing loan interest u/s 24(b), Leave travel allowance u/s 10(5), Meal allowance exemption, deductions for NPS and other benefits under Section 80C.

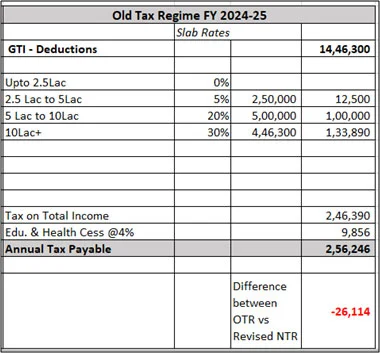

Comparison of tax liability under the Old tax regime Vs. New tax regime in FY 2023-24 and as per the revised rates applicable for FY 2024-25

(Source: PersonalFN Research)

(Source: PersonalFN Research)

As you can see, there is a substantial difference when you opt for the New tax regime due to the flexible rates as compared to the Old tax regime. In this case, there is a difference of Rs 7,800/- when compared to the New tax regime for FY 2023-24 and revised rates for FY 2024-25.

However, do note when comparing the Old Tax Regime with the Revised New Tax Regime, the difference of Rs 26,114/- is seen. As a result, the old tax regime proves to be more beneficial for high-income individuals due to the significant deductions available.

Remember, choosing between the Old and New Income Tax Regimes would entirely depend on a case-to-case basis. Your decision to choose the most suitable tax regime should be based on a variety of factors such as current income level, income structure, exemptions, deductions you are eligible for, etc.

Therefore, the tax benefits have been tweaked in the recently announced Modi 3.0 full Budget for FY 2024-25 to encourage individuals to move towards the New tax regime, which has not seen much traction since its launch in FY 2020-21 and to provide relief to middle-class taxpayers.

[Read: Mutual Fund Taxation: Here Are the Key Changes After the Union Budget 2024-25]

To conclude...

Deciding whether the New tax regime is more beneficial for you depends on a detailed analysis of your income and eligible deductions. The inclusion of a Standard Deduction of Rs 75,000 makes it more appealing, especially for salaried individuals and pensioners who may not have numerous other deductions to claim.

However, if you are someone who can take full advantage of the various deductions and exemptions under the old regime, such as those for investments, home loan interest, and medical insurance premiums, you might find that the Old regime offers more substantial tax savings.

Therefore, it is crucial to calculate your tax liability under both regimes, considering all possible deductions and exemptions, before making an informed decision. This approach ensures that you choose the regime that aligns best with your financial strategy and maximises your overall tax benefits.

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

MITALI DHOKE is a Research Analyst at PersonalFN. She is an MBA (Finance) and a post-graduate in commerce (M. Com). She focuses primarily on covering articles around mutual funds including NFOs, financial planning and fixed-income products. Mitali holds an overall experience of 4 years in the financial services industry.

She also actively contributes towards content creation for PersonalFN’s social media platforms in the endeavour to educate investors and enhance their financial knowledge.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.