Here’s Why Your Personal Accident Insurance Policy Claim Could Get Rejected

Listen to Here’s Why Your Personal Accident Insurance Policy Claim Could Get Rejected

00:00

00:00

Accidents can happen anytime and anywhere, unexpectedly and unintentionally. Such unfortunate events may lead to small or big physical injuries or in the worst case even death. A Personal Accidental Insurance Policy financially protects you against uncertainties such as, death, bodily injuries, permanent/temporary and/or total/partial disabilities arising out of an accident.

You can purchase a Personal Accident Insurance Policy like any other insurance policy, online or offline. The premium that you pay for the coverage primarily depends upon your location, age, occupation and the offerings of the plan. It typically covers medical expenses like emergency treatments, medical tests, hospital room rent, cost of medicines, etc. arising out of an accident and provides monetary benefit to the family in case of an unfortunate accidental death of the policyholder.

What is covered under the Personal Accident Insurance Policy?

As the name suggests, Personal Accident Insurance provides coverage only towards the situations caused by an accident. Here are the coverage benefits offered under the plan:

1. Accidental Death:

In case of unfortunate accidental death of the policyholder, the insurance company pays the entire sum insured to the nominee, as mentioned in the policy documents.

2. Permanent Total Disability:

If the accident results in permanent total disability of the policyholder, such as permanent loss of both limbs or eyes, an insurance company can pay up to 100% of the benefit of the sum insured as per terms and conditions of the policy.

3. Permanent Partial Disability:

In case of a permanent partial disability, such as loss of one limb or one eye, up to 50% of the benefit of the sum insured is paid to the policyholder, depending upon the policy terms and conditions.

4. Temporary Total Disability:

If an accident results in temporary total disability of the policyholder due to which there is a loss of income for specific period, an insurance company provides Daily/Weekly Cash Benefit, which can be used to fulfil any needs of the family.

What is not covered under the Personal Accident Insurance Policy?

(Image Source: www.freepik.com)

An occurrence of accident under the following situation will lead to personal accident insurance claim rejection. However, one should remember that the list of exclusions varies from insurer to insurer. Therefore, it is advisable to read such crucial details before purchasing the policy. Here is a common list of exclusions that are typically not covered under the Personal Accident Insurance Policy.

-

Natural death of the policyholder.

-

An accident caused due to participation in adventure sports or activities such as, paragliding, scuba diving, bungee jumping, parasailing, etc.

-

Self-inflicted injuries or suicide by the policyholder.

-

Childbirth or pregnancy-related complications.

-

Pre-existing disabilities or injuries of the policyholder.

-

If an accident occurs when the policyholder was under the influence of intoxicants such as, alcohol, drugs, etc.

-

Participation of a policyholder in criminal or hazardous activities that leads to an accident.

-

Mental disorder of the policyholder causing an accident.

-

An accident caused due to the policyholder's participation in defence services like Military, Naval, or Air Force.

-

An accident caused by war or war-like situations.

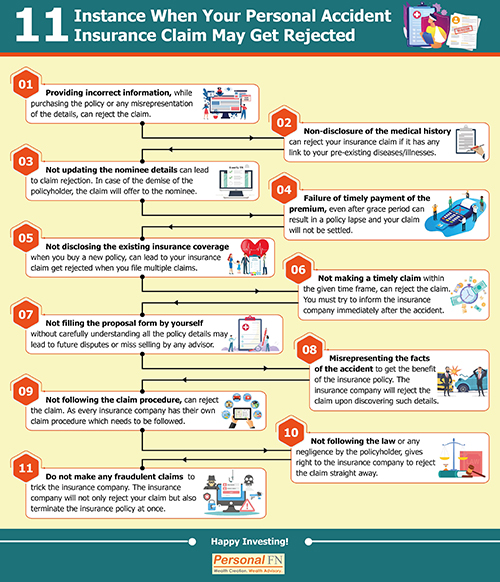

When can a Personal Accident Insurance claim get rejected?

Apart from the exclusions mentions above, below are the common mistakes while purchasing the policy or filing a claim that can lead to personal accident insurance claim rejection:

1. Providing incorrect information while purchasing the policy:

Your insurance claim will be rejected if you have provided any incorrect details while purchasing the policy. Your personal details, such as age, gender, occupation, income, smoking habits, etc. are the major deciding factors of the premium you pay to get the insurance coverage. In order to try to lower the premium, some individuals misrepresent such crucial information. For example, in many cases, individuals do not disclose their smoking habits as they think it will either unnecessarily reject their insurance application or they will be charged a heavy premium. However, when the insurance company discovers the incorrect or misrepresentation of the details at the time of claim settlement, they can reject the claim on the grounds of providing incorrect or false information.

2. Non-disclosure of the medical history:

While purchasing the policy, an applicant has to provide details of their medical history such as, pre-existing diseases or illnesses, previously done surgeries or operations, any other medical conditions, etc. Apart from this, you might also be asked about the medical history of the family, such as cancer, blood pressure, or any other genetic conditions. If the insurance company discovers the non-disclosed medical history, your insurance claim can get rejected if it has any link to your pre-existing diseases/illnesses.

3. Not updating the nominee details:

In case of the demise of the policyholder, an insurance company provides a death benefit to the nominee mentioned on the personal accident insurance proposal form. Therefore, it is essential to provide correct nominee details such as, full name, date of birth, address, etc. Moreover, it is necessary to update the insurance company if any changes need to be done with the nominee details such as, change of address, contact details, change of nominee, etc. Failing to do so can lead to claim rejection.

4. Failure of timely payment of the premium:

The insurance companies usually provide a grace period of 30 days if you fail to pay the premium for policy renewal. However, if you do not pay the premium even after the grace period, it can result in a policy lapse. Any insurance claims made once the policy is lapsed or expired are not settled by the insurance company. Therefore, it is necessary to make timely payments of the premiums to enjoy uninterrupted insurance coverage.

5. Not disclosing the existing insurance coverage:

It is mandatory to provide the details of your existing insurance coverage such as, the amount of coverage, name of the insurance company, policy number, etc. People often avoid this mandatory requirement as they think it might restrict them from getting additional coverage. In some cases, people don't want the hassle of going through old policy documents to check the details. This can lead to your insurance claim being rejected when you file multiple claims. Therefore, make sure you provide the details of all insurance policies in your name when you buy a new policy.

6. Not making a timely claim:

Every insurance policy has mentioned the time limit within which you are required to file a claim. If you do not make a claim within the given time frame, the insurance company can reject the claim. It is advisable to inform the insurance company immediately after the accident. However, if the reason for the delay in making a claim is valid, the insurance company may proceed with the claim settlement.

7. Not filling the proposal form by yourself:

Many times people simply sign on the insurance proposal form and submit the other required documents to the advisor. The advisor then fills up the form on behalf of the applicant. However, there are chances that the advisor does not disclose all the policy details to the applicant and miss-sells the insurance. If it is found by the insurance company that you have not filled the insurance proposal form by yourself, they can reject your claim. Therefore, it is advisable to carefully read and understand all the policy details, including its terms and conditions, list of inclusions, list of exclusions, and policy exemptions, etc. to avoid any future disputes. Your signature is the acceptance of the policy agreement which you must be aware of before buying the policy.

8. Misrepresenting the facts of the accident:

In some cases, the policy holder hides or misrepresents the accident to get the benefit of the personal accident insurance policy. For example, the policyholders may not divulge to the insurance company if the accident occurred when they were under the influence of alcohol. However, upon discovering such details, the insurance company will reject the claim, which could have otherwise been settled. Some insurance companies may offer to pay you the compensation if you provide all the correct details without misrepresenting the facts.

9. Not following the claim procedure:

Every insurance company has its own claim procedure, which a policyholder is required to follow while making a claim. The insurance company can reject the claim if you do not follow the proper procedure laid down by them. Therefore, it is vital to know the claim settlement process of your insurer in advance. Moreover, it is essential that you provide all the required documents without any delay and file the First Investigation Report (FIR) at the earliest, as not doing so will result in holding your personal accident insurance claim.

10. Not following the law:

If the accident occurs because of the policyholder's negligence or the policyholder not following the law, the insurance company will reject the claim. For example, driving without a licence or helmet, using a private vehicle for commercial purposes, etc. are illegal acts. And, if the policyholder is facing loss due to an accident that occurred because the policyholder was not following the law or showing negligence towards it, the insurance company holds the right to reject such claims.

11. Making fraudulent claims:

Some people try to trick the insurance company by making fraudulent claims in order to earn money out of it. Upon discovering the fraud, the insurance company can not only reject your claim, but can also terminate the insurance policy. Therefore, it is in the best interest of the policyholder to provide the correct details of the accident and not try to dupe the insurance company.

To Conclude:

It is important to know that this type of insurance does not cover any other type of death apart from accidental death, and medical claims arising from accidents only are covered under the plan. However, Personal Accident Insurance Policies are ideal if one wants to get maximum coverage at a minimum premium. The premium is very low compared to the other types of insurances as it offers coverage only against accidents. It is advisable to cover yourself with Personal Accident Insurance with coverage of 100-times of your monthly income. Make sure you thoroughly read the policy details before making a purchase and avoid making the mistakes given above to ensure a successful claim settlement.

Warm Regards,

Ketki Jadhav

Content Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds