How Mutual Funds Are Approaching Debt Securities in the Present Times

The massive monetary and fiscal stimulus package (worth USD 410 billion) by the U.S. Federal government to prop-up economic growth amidst the pandemic has been unsettling bond investors as they anticipate potential overheating of the economy and spike in inflation.

The U.S. 10-year Treasury yield from around 0.50% in August 2020 has been inched-up to 1.69% as of March 22, 2021 (see Graph 1). Market participants anticipate that the U.S. 10-year Treasury yields could harden even more, to around 2.0% if inflation continues to rise.

The U.S. Federal Reserve Chief, Jerome Powell has recently acknowledged that the United States of America will see higher inflation this year (due to major economic sectors recovering from the slumps of March and April 2020), but also opined that the uptick in prices will not be substantial. The U.S. Federal Reserve's target for inflation is 2.00% and it intends to keep interest rates near-zero until then to support growth amidst the pandemic.

Graph 1: The peregrination of the U.S. 10-year Treasury yields

Data as of March 22, 2021

Data as of March 22, 2021

(Source: www.macrotrends.net)

In India, the Reserve Bank of India (RBI), as well since the outbreak of the COVID-19 pandemic, has reduced policy rates by 115 basis points (bps), and since February 2019 by good 250 bps to support growth. Currently, the monetary policy stance is kept "accommodative as long as necessary - at least during the current financial year and into the next financial year - to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy while ensuring that inflation remains within the target going forward," as stated by RBI it last monetary policy review meeting.

That said, due to inflationary pressures, if the Consumer Price Index (CPI) reports a higher reading; policy rates could increase. It is important to note that recognising the intermittent risk to the inflation trajectory, the RBI in the last four monetary policy review meetings maintained a status quo on policy rates while ensuring that liquidity conditions in the system remain comfortable.

India's 10-year G-Sec yield, since the Union Budget 2021-22 announcements---mainly because of the widening the fiscal deficit target and higher borrowing program (of Rs 12.05 trillion)---has also hardened 30 bps to 6.18% as of March 22, 2021. These factors have not gone well with the sentiments in bond markets, given India's already has a high debt-to-GDP (70% of GDP). The increase in borrowings in the current fiscal year means an increase in the supply of government bonds, which would exert upward pressure on longer tenure bond yields.

In the current uncertain times, the longer end of the yield curve is seemingly more sensitive than the shorter end. And that's the reason why, of late, barring liquid funds, money market funds, low duration funds, most other sub-categories of debt-oriented mutual fund schemes are witnessing an exodus of money flow, although the net Assets Under Management (AUM) of debt funds is worth Rs 13.7 trillion as on February 28, 2021.

According to a report published by CARE Ratings on March 19, 2021, at present mutual funds are betting big on the short end of the yield curve. As of February 28, 2021, debt funds had invested 47.3% of their assets in securities with a residual maturity profile of less than 90 days, whereas, 38.2% of their assets were debt instruments having residual maturity of more than a year.

Before drawing any conclusion from this data, it's important to understand how the category-wise classification of AUM looks like.

Table 1: Sub-category-wise AUM of debt mutual funds

| Sub-categories of Debt Mutual Funds |

Category weight in the total AUM of income/debt oriented schemes |

| Feb-21 |

Jan-21 |

Feb-20 |

| Liquid Funds |

25.9% |

24.5% |

36.3% |

| Corporate Bond Funds |

11.4% |

11.9% |

7.0% |

| Short Duration Funds |

11.2% |

12.0% |

8.6% |

| Low Duration Funds |

10.6% |

10.4% |

8.3% |

| Banking and PSU Funds |

9.1% |

9.3% |

6.4% |

| Ultra Short Duration Funds |

7.1% |

7.3% |

8.3% |

| Money Market Funds |

7.0% |

6.3% |

6.9% |

| Overnight Funds |

4.8% |

4.8% |

4.4% |

| Floater Funds |

4.5% |

4.6% |

3.1% |

| Medium Duration Funds |

2.2% |

2.3% |

2.5% |

| Credit Risk Funds |

2.0% |

2.1% |

5.1% |

| Dynamic Bond Funds |

1.8% |

2.0% |

1.6% |

| Gilt Funds |

1.2% |

1.3% |

0.7% |

| Medium to Long Duration Funds |

0.8% |

0.9% |

0.8% |

| Long Duration Funds |

0.2% |

0.2% |

0.1% |

| Gilt Funds with 10 year constant duration |

0.1% |

0.1% |

0.1% |

| AUM of income/debt oriented schemes (Rs crore) |

13,74,384 |

13,74,117 |

12,22,324 |

(Source: AMFI)

Liquid Funds still occupy a major chunk of the total AUM of debt funds. Credit Risk Funds have clearly lost their popularity due to the amplified credit risk in an uncertain environment.

Despite a massive rally in bonds over the last one year, gilt funds haven't been a sought-after choice of investors. Perhaps investors are rightly assessing that the present interest rate cycle has almost bottomed out. The shift towards Banking & PSU Debt Funds and Corporate Bond Funds suggests that safety has become an important criterion for fund selection, and rightly so.

Since short-tenure funds are popular with investors, fund managers have also preferred to stick to the shorter end of the yield curve, and not the other way round. After all, fund managers are bound by the scheme mandates rather than anything else.

A deeper analysis of portfolios of debt schemes reveals that the proportion of Certificate of Deposits (CDs), Commercial Papers (CPs) and other types of corporate debt instruments in the AUM of debt funds has fallen noticeably over the last one year on account of fall in interest rates on such instruments and flush liquidity.

(Image source: freepik.com; photo created by mindandi)

(Image source: freepik.com; photo created by mindandi)

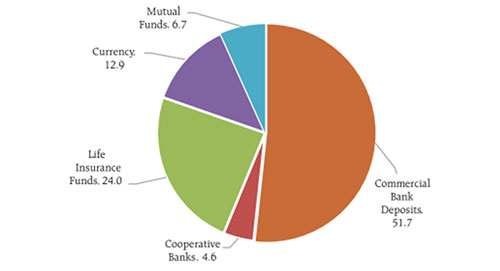

Where are households in India deploying their savings?

Households in India, particularly the retail investors, are wary of deploying their savings into certain sub-categories of debt mutual funds. Of the 31.9% proportionate share of debt-oriented schemes in the Indian assets as of February 2021, institutional investors still occupy a 61% chunk. Household savings in India have mainly being deployed into bank deposits (Commercial and Co-operative Banks) and various life insurance policies --particularly during uncertain times (see Graph 2).

Graph 2: Composition of Household Financial Assets

(Source: RBI's March 2021 Bulletin)

(Source: RBI's March 2021 Bulletin)

During the COVID-19 lockdowns last year, the rate of household savings touched an unprecedented high of 21% in Q1FY21. But with easing COVID-19 restrictions, people moving out and buying discretionary goods and seeking loans; preliminary estimates of the RBI reveal that household savings in Q2FY21 regressed to the pre-pandemic level to 10.4%, following a global pattern. The household debt-to-GDP ratio in India has gone up sharply from 35.4% in Q1FY21 to 37.1% in Q2FY21, observes the RBI.

With the second wave of COVID-19 India, in my view, households should focus on saving more and deploying the money saved in productive avenues whereby the investment portfolio clocks an efficient real rate of return (also known as the inflation-adjusted return).

Follow an asset allocation that is best suited for you and diversify your investments well across asset classes and investment avenues therein. Own a variety of the best mutual funds in your portfolio; do not skew only to bank Deposits.

[Read: Can Senior Citizens Solely Depend On Fixed Income Instruments for their Retirement Needs?]

A sensible approach with an astute investment strategy would pave the path to wealth creation and is always good for your long-term financial well-being.

The path to interest rate and the investments strategy to follow while investing in debt mutual funds now...

RBI has time and again reiterated that its policy stance is going to remain accommodative until growth revival is clearly visible. Although the stance of the monetary policy is kept, it could prove meaningless if CPI inflation rises beyond RBI's comfort range. The upward pressure to the inflation trajectory emanates from higher 'food & beverage prices, 'light and fuel' (due to the rise in oil prices and LPG), and 'transport & communication'. Core inflation (which excludes food, fuel and light) also continues to be sticky.

Overall it appears that the present interest rate cycle has bottomed out. Most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing policy rates. Debt securities with longer maturity papers may not be able to generate returns as seen in the last couple of years. The returns may moderate on the longer end of the yield curve and could turn riskier (may encounter high volatility) in the foreseeable future.

To approach debt mutual funds, the shorter end of the yield curve looks more attractive than the longer end. To put it simply, you'll be better off deploying your hard-earned money in shorter duration debt mutual funds. Having said that, approach even short-term debt funds with your eyes wide open, paying attention to the portfolio characteristics and quality of the scheme. Stay away from debt mutual fund schemes that have exposure to low-rated securities in the hunt for yield, as we have seen a widespread contagion of credit risk and mismanagement of fund houses. You see, very severe stress on the financial system was introduced amidst the COVID-19 pandemic and the situation would not be settling soon with the second wave of COVID-19 now.

Hence, it would be wise to stick to debt mutual funds where the fund manager does not chase yields by taking higher credit risk but instead focuses on government and quasi-government securities. You may consider Banking & PSU Debt Funds that allocate 85-90% of its assets in instruments issued by major Banks and PSUs for an investment time horizon of 2 to 3 years.

For a shorter time horizon of you would do better going with only a pure Liquid Funds and/or Overnight Fund who does not have exposure to private issuers. Prefer the safety of principal over returns.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

Editor's Note: If you are looking for quality mutual fund schemes to add to your investment portfolio, I suggest you subscribe to PersonalFN's premium research service, FundSelect. Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

Under DebtSelect, we give high weightage to schemes displaying worthy portfolio characteristics. We avoid debt mutual fund schemes that aim for higher yields by taking undue higher credit risk with substantial exposure in instruments issued by private issuers.

At PersonalFN we follow a comprehensive S.M.A.R.T Score Matrix, wherein we evaluate...

-

S - Systems and Processes

-

M - Market Cycle Performance

-

A - Asset Management Style

-

R - Risk-Reward Ratios

-

T - Performance Track Record

The stringent process has helped our valued mutual fund research subscribers to own some of the best mutual fund schemes in the investment portfolio with a commendable long-term performance track record.

This service is apt for you if you are looking for insightful guidance and recommendations on some worthy funds having high growth potential, in the years to come.

We will also help you choose some of the best Equity Linked Saving Schemes (ELSS) for your tax-saving with PersonalFN's premium research service, FundSelect.

PersonalFN's FundSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds