How the Regulator Is Ensuring That You Can Make an Informed Decision When Investing In Debt Mutual Funds

Listen to How the Regulator Is Ensuring That You Can Make an Informed Decision When Investing In Debt Mutual Funds

00:00

00:00

The ongoing COVID-19 pandemic has wreaked havoc for various sectors of the economy. However, for India's mutual fund industry, the impact perhaps is the least: the Assets under Management (AUM) is on the rise supported by upward market movement, various type of mutual funds are reporting inflows, and folios have touched a record high.

Yet some fund houses have held the pandemic responsible as a black swan event to hide the big black holes in their investment systems and processes. They have taken refuge under the standard disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. But, the fact is, none of such disclaimers warns mutual fund investors against losses arising on account of mismanagement and negligence.

The recent episode of Franklin Templeton serves as an example and brings to light how lapses and violations could happen when trustees, whose job is to ensure the pool of money in the respective schemes is managed in the interest of unitholder/investors, do not follow high fiduciary standards for the position they occupy.

As you may know, Franklin Templeton Mutual Fund arbitrarily shut down six debt schemes that collectively had the Asset Under Management (AUM) of Rs 26,000 crore in April 2020. Justifying the move, the fund house cited two primary reasons: 1) liquidity crunch and 2) mounting redemption pressures due to coronavirus pandemic. Thankfully, the capital regulator, SEBI immediately swung into action and pulled up the fund house for this, and very recently even held the trustees for violation of regulations and imposed penalties amounting to Rs 15 crore on the Franklin Templeton Mutual Fund, wherein it even made the CEO, CIO, CCO, and fund managers personally liable. Moreover, as a punitive action, the regulator banned the fund house from launching any new debt fund scheme for two years. The regulator's observations, in this case, have been quite serious and pointed.

The market regulator has found Franklin Templeton 'obsessed' about chasing 'high yields' without paying any attention to the risks involved. The six schemes which were suspended last year had different objectives, investment mandates, and despite that, they had similar portfolios. The proportion of AA and below bonds, especially in the shorter duration schemes, has been unnerving. So far only about 71% of the money (AUM as of April 23, 2020) has been distributed among investors of the six shuttered debt mutual fund schemes.

The regulator has censured Franklin Templeton's fund management for not exercising the exit options from the debt instruments. Plus, SEBI found Franklin Templeton on a wrong footing for not being able to take concrete steps in managing various risks such as the risk of concentration, liquidity and downgrades amongst others. The fund house failed to make appropriate risk disclosures as regards valuation and credit rating agencies.

Additionally, the regulator pointed out that the fund managers of these schemes violated practices meant to protect investors' interest including those pertaining to resetting interest rate on instruments, and calculation of Macaulay Duration (MD).

My colleague Vivek wrote an extensive piece on how the debt scheme fiasco has been leading to investors losing confidence in Franklin Templeton Mutual Fund. Read here.

This wasn't the first occasion when investors had to bear the brunt of the negligence of mutual fund managers-IL&FS, Essel, Reliance ADAG, Jet Airways, DHFL...the list is long.

(Image source: pixabay.com)

(Image source: pixabay.com)

The capital market regulator has time and again directed mutual funds to adopt more pro-investor practices. And on the backdrop of repeated unpleasant experiences in the case of debt mutual fund schemes, appropriate additional guidelines have been issued by the regulator to protect your, the investor's, interest.

Last week, in a circular dated June 7, 2021, the capital market regulator has introduced a dynamic scheme classification concept of the Potential Risk Class (PRC) matrix for debt funds based on interest rate risk and credit risk. The regulator considered the recommendations of the Mutual Fund Advisory Committee (MFAC) and also held discussions with asset management companies to arrive at this decision.

So, what will change for debt mutual funds?

Mutual fund houses will continue to classify their debt offerings according to the existing Categorization and Rationalization norms. PRC will be additional compliance and won't be considered as the changes in the fundamental attribute, but in fact, help in evaluating the risk better.

The market regulator has offered complete freedom to fund houses in selecting any of the 9 combinations to highlight the interest rate and credit risk attributes of schemes. However, once the classification is done, the subsequent changes would be treated as the changes in the fundamental attributes of schemes.

Three buckets for measuring the interest rate risk based on MD are:

-

Class I: MD <=1 year

-

Class II: MD <=3 year

-

Class III: Any (other) MD

In other words, the lower the MD, the lower would be the interest rate risk involved. MD value is the weighted average MD of each instrument in the portfolio of the scheme, and weights are based on the proportion to the AUM. Moreover, the value of the debt instrument to be considered in calculating the AUM shall include interest, i.e. dirty price as per SEBI.

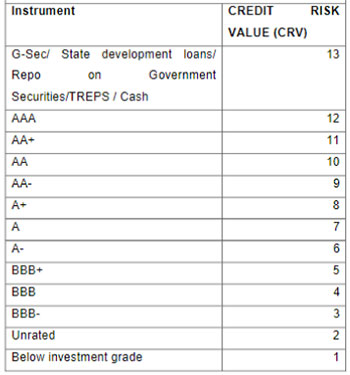

Similarly, different instruments will have pre-specified Credit Risk Values (CRVs) starting from 13 and going down to 1; wherein the highest value denotes the highest safety and vice versa. In other words, G-sec instruments will have a score of 13 and the below investment grade bonds will have a score of 1.

Table 1: Credit Risk Values of Debt Securities

(Source: SEBI Circular)

(Source: SEBI Circular)

As per the regulator, for investments in mutual funds in instruments having short-term ratings, the credit risk value shall be based on the lowest long-term rating of an instrument of the same issuer as shown above (in order to follow a conservative approach) across credit rating agencies. But if there is no long-term rating of the same issuer, then based on credit rating mapping of Credit Rating Agencies (CRAs) between short-term and long-term ratings, the most conservative long-term rating shall be taken for a given short-term rating.

The three credit risk buckets are as follows:

-

Class A: CRV>=12

-

Class B: CRV>=10

-

Class C: CRV<10

The CRV of the scheme shall be the weighted average of the credit risk value of each instrument in the portfolio of the scheme, the weights based on their proportion to the AUM.

Table 2: Debt scheme classification matrix to highlight the interest rate and credit risk

| Credit Risk (alongside) |

Class A (CRV >=12) |

Class B (CRV>=10) |

Class C (CRV<=10) |

| Interest Rate Risk (below) |

| Class I: (MD<=1) |

Relatively Low Interest Rate Risk and Relatively Low Credit Risk |

Relatively Low interest rate risk and moderate Credit Risk |

Relatively Low interest rate risk and Relatively High Credit Risk |

| Class II: (MD<=3) |

Moderate interest rate risk and Relatively Low Credit Risk |

Moderate interest rate risk and moderate Credit Risk |

Moderate interest rate risk and Relatively High Credit Risk |

| Class III: (Any Macaulay Duration) |

Relatively High interest rate risk and Relatively Low Credit Risk |

Relatively High interest rate risk and moderate Credit Risk |

Relatively High interest rate risk and Relatively High Credit Risk |

(Source: SEBI Circular)

The combination of the existing Risk-O-Meter and PRC is expected to give investors an idea not only about the existing risk profile of the debt mutual fund scheme but also of its potential risk profile.

A scheme classifying itself in the 'Class I' bucket of interest rate risk can hold an instrument with a maximum residual maturity of three years. Similarly, a scheme classifying itself in the 'Class II' category can hold an instrument with a maximum residual maturity of seven years. There is no such cap on the Class III schemes; it can invest in instruments of any maturity. Furthermore, ceilings on the maximum permitted residual maturity for Class I and Class II schemes won't apply to investments in government securities. Only the caps pertaining to weightage average MD for the portfolio will apply.

When it comes to credit risk disclosures, the market regulator has followed an ultra-conservative stance in the interest of unitholders/investors.

The compliance of the PRC matrix will be applicable from December 1, 2021.

Here's how the new norms will help investors to make well-informed decisions...

-

✓ The new classification rules will help investors select suitable debt mutual fund schemes based on their risk profile and investment time horizon.

-

✓ Since the thresholds of credit and interest rate risks are defined at the time of investing in the scheme and any subsequent change thereof is transparently communicated to the investors, panic redemptions may reduce significantly, particularly during challenging market conditions.

-

✓ Short term debt funds won't be able to invest in long-term non-government bonds. Debt mutual fund schemes investing in long-term bonds will have to classify themselves in Class III. Companies having low long-term ratings and high short-term ratings won't be able to lure mutual funds. This eventually may help better product categorization and improve product suitability.

-

✓ To be able to classify as a 'Class A' scheme on CRVs, fund houses will have to chiefly target sovereign or AAA-rated instruments. This will eventually keep a check on yield hunting and investments in below AAA-rated instruments---a trait observed amongst Franklin Templeton's fund managers.

In summary, the new norms would help bring back the portfolio discipline amongst mutual fund houses, improve disclosures and achieve greater transparency. More importantly, the new rules will protect investors from potentially negligent investment practices at mutual fund houses.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

Editor's Note: If you are looking for quality mutual fund schemes to add to your investment portfolio, I suggest you subscribe to PersonalFN's premium research service, FundSelect. Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

Under DebtSelect, we give high weightage to schemes displaying worthy portfolio characteristics. We avoid debt mutual fund schemes that aim for higher yields by taking undue higher credit risk with substantial exposure in instruments issued by private issuers.

At PersonalFN we follow a S.M.A.R.T Score Matrix, wherein we evaluate:

-

S - Systems and Processes

-

M - Market Cycle Performance

-

A - Asset Management Style

-

R - Risk-Reward Ratios

-

T - Performance Track Record

The stringent process has helped our valued mutual fund research subscribers to own some of the best mutual fund schemes in the investment portfolio with a commendable long-term performance track record.

This service is apt if you are looking for insightful guidance and recommendations on some worthy funds having high growth potential, in the years to come.

We will also help you choose some of the best Equity Linked Saving Schemes (ELSS) for your tax-saving with PersonalFN's premium research service, FundSelect.

PersonalFN's FundSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds