Will Gold Lose Its Lustre Going Forward?

Listen to Will Gold Lose Its Lustre Going Forward?

00:00

00:00

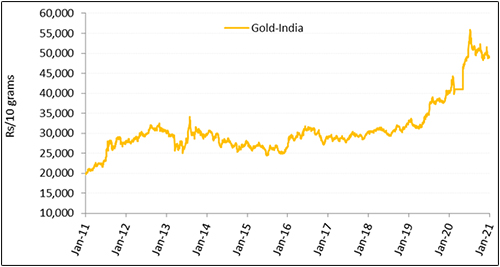

Since the beginning of the fiscal year, which coincided with the first lockdown phase, gold prices have rallied nearly 25%. The prices touched a peak of Rs 55,922 (MCX Gold price per 10 gram) in the month of August, proving to be a safe haven amidst the uncertainty.

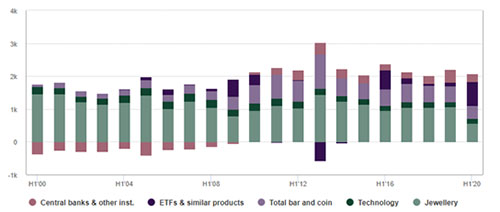

The elevated prices amidst the COVID-19 crisis kept the demand for gold muted, people are focused on essentials, conserving cash and pushing back discretionary spends, leading to plunge in demand for gold. Demand for gold jewellery fell 74% in the June quarter as compared to the year ago period at 44 tonnes (t).

Likewise, demand in H1 2020 was down 60% to an all-time low for our series of 117.8t, according to the data released by the World Gold Council (WGC).

Over the past couple of weeks, gold prices have witnessed a sharp decline, down by about Rs 6,000 from its peak. This could be attributed to profit booking in gold.

Despite decline in prices, the demand for gold continued to be muted. According to data by Ahmedabad Air Cargo Complex (AACC), gold import declined by 75% in September to 0.47 metric tonne (MT), lower than 1.9 MT in August.

When the economy started to gradually unlock, investors shifted preference to equities; hence, gold demand took a major hit in September. Moreover, a vast segment of investors in India believe it is inauspicious to purchase gold during the Shradh period, which fell during the month of September. This could have further deterred investors away from gold.

However, with the festive season about to commence, the demand for gold may start to look up. But the WGC does not expect a significant improvement in demand during the second half of 2020 due to the slowdown in economic activities, concerns about rising unemployment, and income erosion.

Graph 1: Gold jewellery demand plunged sharply in H1 2020

(Source: World Gold Council)

(Source: World Gold Council)

That said, gold would continue to play an increasingly relevant role in the investor's portfolio, because in response to the pandemic when central banks around the world aggressively cut rates and/or expand asset purchasing programmes, the unintended consequences are:

-

Soaring equity market valuations that are not always backed by fundamentals, increasing the chance of pullbacks

-

Corporate bond price increases, pushing investors further down the credit-quality curve

-

Short-term and high-quality bonds have limited - if any - upside, reducing their effectiveness as hedges

Global uncertainty has heightened and central banks across the globe are maintaining healthy gold reserves in cognizance of the following factors:

-

COVID-19 cases are failing to recede and there is a second wave of virus outbreak.

-

GDP growth has contracted sharply in advanced economies and emerging economies.

-

A virus-led global recession looks inevitable ---probably worse than the Global Financial Crisis of 2008 as pointed out by the IMF. The IMF has observed that the COVID-19 crisis is like no other.

-

Consumption is muted in many parts of the world posing a challenge to reinvigorate growth.

-

The central banks across the world are reducing interest rate and keeping monetary policy stance accommodative to support growth.

-

The global debt-to-GDP is at a record high, nearly US$ 258 trillion (over 331% of global GDP) as per the Institute of International Finance. This is because most economies are relying on sovereign debt, particularly when their economic growth rate has shrunk sharply amidst the pandemic.

-

Geopolitical tensions are escalating with every country blustering nationalism and protecting its political and economic interest--the US, UK, China, India, Pakistan, South Korea, North Korea, discontent in Latin America, and even countries in the MENA (the Middle East and North African) regions.

-

Trade war tensions exist due to protectionist policies followed by many nations.

-

There is a potential risk to the inflation trajectory (mainly on account of food).

-

The US Presidential elections are in November 2020.

-

The stock market volatility has increased.

Gold tends to outperform other asset classes during extreme events such as recession, which makes it an important asset from a diversification and hedge point of view. Unlike financial assets, gold is a real asset. This means, gold does not carry credit or counterparty risk and usually supported by high inflation. This is why gold has demonstrated its appeal and fared well over the long-term.

Graph 2: Gold displays its lustre in the long run

Data as on October 05, 2020

Data as on October 05, 2020

(Source: MCX, PersonalFN Research)

Going forward, gold is expected to display its lustre, play the role of an effective portfolio diversifier, a hedge (when other asset classes fail to post alluring returns), a safe haven, and command a store of value ---particularly when the world is staring at economic uncertainty caused by the pandemic and geopolitical tensions are escalating.

Therefore, it makes sense to tactically invest in gold. Irrespective of your risk profile, consider allocating around 10% to 15% of your entire investment portfolio in gold with a long-term view (whereby short-term price fluctuations can be mitigated).

Here are the smart ways to invest in gold:

-

Gold Exchange Traded Funds (Gold ETFs) - Gold ETFs are open-ended exchange-traded funds (offered by mutual funds) which track the price of gold, and each unit represents ownership of the gold asset. Each unit in the gold ETF is equal to 1 gram of gold (some mutual fund houses also offer 1 unit at 0.5 gram of gold).

The investment objective is to generate returns broadly in line with the performance of gold (the domestic price of gold).

You can purchase units of gold ETF on the recognised stock exchange; a demat account and share trading account is necessary.

Do note that on the exchange, the units can be purchased/sold in a minimum lot of 1 unit and multiples thereof. When you buy gold ETF, you get a contract indicating your ownership in gold equivalent to the rupee amount of your investment.

The gold is held on your behalf by an appointed custodian for the ETF. Notably, you will not get to see or receive delivery of the gold you own.

The tax implications when you sell physical gold and Gold ETFs are the same. Selling gold ETF units attracts capital gain tax. And in times of need, the units can be used as collaterals for loans.

-

Gold Saving Funds - This is an open-ended Fund of Fund scheme (offered by mutual fund houses) investing its corpus into an underlying Gold ETF, which benchmarks the performance against prices of physical gold.

Thus, the investment objective is to generate returns that closely correspond to returns generated by the underlying Gold ETF.

The application for purchase needs to be made to the respective mutual fund house, a demat account is not necessary. The units allotted reflect in your mutual fund account statement. The units are purchased/sold at the NAV declared by the mutual fund house.

Investment in a Gold Savings Fund can be done lump sum or through SIP (Systematic Investment Plan), whichever way is convenient for you.

The minimum investment amount to invest in a Gold Savings Fund is Rs 5,000; for additional purchase, the minimum amount usually is Rs 100; while the minimum SIP amount required is Rs 1,000 (with minimum 36 instalments).

Speaking of the tax treatment, in case of Gold Savings Fund and gold ETF is the same. Selling units of a Gold Savings Fund attracts capital gain tax.

To invest in gold regularly, systematically and in a disciplined manner, taking the SIP route with a Gold Savings Fund would prove sensible -- as it can help compound wealth with the benefit of rupee-cost averaging.

If you invest in gold now, it would probably help your investment portfolio overcome challenges caused by risk, volatility, and correlated global influences in the journey of wealth creation.

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds