Going beyond numbers, inflation has been hurting the industry. For business houses, it means cost of borrowing and cost of raw material remaining higher making a dent into their profitability. This looks much relevant to India at current juncture. Growth (measured by GDP as well as IIP) is falling and companies in the capital intensive industries are holding back their expansion plans due to dearer credit and uncertain economic conditions. Equity investors usually avoid sectors which are faltering on growth. However, this is not to say that when the sector is not growing, all companies in the sector wouldn’t grow. Some may still grow at ferocious pace and bottom up stock pickers may still prefer them.

One sector that would best explain this scenario is the capital goods sector. Capital Goods sector has been the lynchpin of India’s manufacturing wheel. Post-Independence, India followed "Mahalanobis Model" of growth, the model which emphasises on attaining self-sufficiency in building manufacturing capacities. It assumes that country of a huge population such as India would primarily be driven by the domestic consumption. In order to be able to produce superior consumption goods, the country at first, has to be self-sufficient in production of capital goods. This will then augment the capacity of production of consumption goods.

Capital goods sector comprises mainly of companies (but not exhaustive) that operate in any of the area of production as mentioned below:

- Machine Tools

- Plastic processing Machinery

- Mining & Earthmoving

- Heavy electrical & Power Plant Equipment

- Metallurgical Machinery

- Textile Machinery

- Process Plants

- Engineering Goods

- Dies, Moulds and Tools

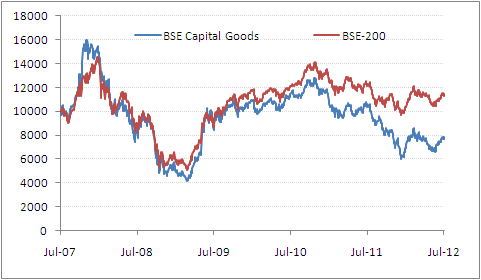

BSE Capital Goods vs BSE 200

Base: Rs 10,000

(Source: ACE MF, PersonalFN Research)

Capital Goods (CG) once investors’ preferred sector has been witnessing ebbing popularity these days at least their stock prices say so. Rs 10,000 invested in BSE Capital Goods Index on July 13, 2007 would have reduced to Rs 7,699 on July 13, 2012. On the other hand Rs 10,000 invested in BSE 200 would have returned Rs 11,293 on July 13, 2012. Movement in BSE Capital Goods Index, over last 2 years, shows a total disconnect from the broader markets (BSE 200). It is imperative to find out what has led investors to completely shun the sector in the last 2 years.

(Source: CSO, PersonalFN Research)

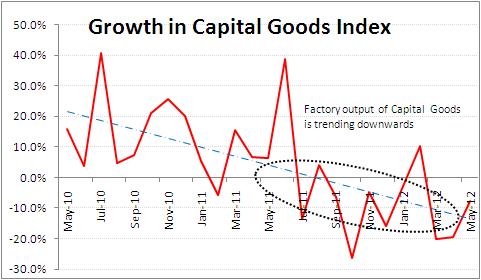

In last two years, the capital goods index, (not to be confused with BSE Capital Goods Index, a stock market index) which is one of the important constituents of Index of Industrial Production (IIP), has seen bouts of volatility with negative bias. It has struggled to maintain a positive growth momentum over last two years which reflects in the stock market performance of the sector as seen above.

Long term growth trend of the Capital Goods Sector

| Capital Goods |

2006-07 |

2007-08 |

2008-09 |

2009-10 |

2010-11 |

5 Yr. CAGR |

| Market Size |

198,240 |

231,542 |

240,811 |

266,785 |

311,515 |

9.5% |

| Domestic Production |

173,627 |

203,644 |

215,711 |

230,425 |

267,944 |

9.1% |

| Imports |

52,160 |

61,020 |

72,187 |

72,696 |

91,055 |

11.8% |

| Exports |

28,577 |

35,776 |

48,709 |

37,832 |

47,348 |

10.6% |

Value: Rs in Crore

(We have considered only following industries

Machine Tools, Plastic processing Machinery, Mining & Earthmoving, Heavy electrical & Power Plant Equipment Metallurgical Machinery, Textile Machinery, Process Plants, Engineering Goods, Dies Moulds and Tools)

(Source: Department of Heavy Industry, PersonalFN Research)

It is clear from the table above; the overall growth in the market size of capital goods sector has been tepid. Domestic production is weak and reliance on imports has gone up. The sector is in the firm grip of bears.

Reasons for Slump

High Inflation, higher borrowing cost and lower outlay towards capacity addition from the Corporates has resulted in lower demand for capital goods. The demand for capital goods depends on the demand for the goods produced by the industries using capital goods. For example, demand for a textile machine depends on the demand for yarn. When a textile company expects boom in the yarn consumption it tries to add up capacities to generate more output in future. But it may hold back its expansion plans when the demand for the end product is low or it will try to find out alternatives to expansion if the cost of adding up new capacities is high. The situation will worsen if the expected demand is low but the cost of borrowing is still high; which is the case at present. In the recovery phase (Started in March 2009), India encountered with the demon of high inflation and to respond to it; RBI increased repo rate 13 times between March 2010 - December 2011. As a result, the cost of borrowing has gone up while higher inflation has lowered the pace of growth in the consumption demand. This is the basic argument for slump in the revenue growth of the companies engaged in production of capital goods.

How Mutual Funds have responded to changing situation?

Being one of the major sectors of Indian economy; mutual funds actively track and invest in capital goods sector. It is important to analyse their response to the changing fundamentals. Let‘s now find out whether mutual funds have followed the trend or have taken a contra call. We shortlisted top 10 schemes by Assets Under Management (AUM) as per their latest disclosed data (June 2012) to get the idea about how mutual funds, by and large, have invested in the capital goods sector in the recent times. Coincidentally 6 out of top 10 mutual funds (in 2012, AUM wise) mentioned in the table were amongst the top 10 funds (AUM wise) even in 2007.

Exposure of Top 10 Funds (Assetwise) to capital Goods Sector

| Scheme Name |

Jun-07 |

Jun-08 |

Jun-09 |

Jun-10 |

Jun-11 |

Jun-12 |

| DSPBR Top 100 Equity (G) |

11.4 |

6.5 |

7.2 |

12.7 |

11.9 |

7.2 |

| HDFC Equity (G) |

6.3 |

12.6 |

6.1 |

5.8 |

4.4 |

6.0 |

| HDFC Top 200 (G) |

8.2 |

12.2 |

6.2 |

8.1 |

4.5 |

5.8 |

| Franklin India Bluechip (G) |

18.8 |

15.7 |

12.9 |

15.1 |

6.8 |

4.6 |

| Reliance Equity Oppor (G) |

15.3 |

14.2 |

14.2 |

9.1 |

8.9 |

4.4 |

| Fidelity Equity (G)* |

13.9 |

9.7 |

9.5 |

8.4 |

6.1 |

3.2 |

| ICICI Pru Focused Blue Chip Equity (G) |

- |

11.1 |

10.1 |

8.2 |

2.5 |

2.7 |

| UTI Dividend Yield (G) |

6.6 |

2.9 |

3.8 |

3.9 |

6.6 |

2.6 |

| Reliance Growth (G) |

11.4 |

4.9 |

7.8 |

7.0 |

5.3 |

2.6 |

| ICICI Pru Dynamic (G) |

5.5 |

8.6 |

3.2 |

5.1 |

5.4 |

1.6 |

*portfolio as on June 30, 2012 was not available and hence the portfolio disclosed on May 31, 2012 is considered

(Source: ACE MF, PersonalFN Research)

Clearly, even the biggies in the industry are wary of capital goods sector and have significantly reduced their exposure over the years. For example, Franklin India Bluechip Fund which has been a decent performer for years; has reduced its exposure from 18.8% in June 2007, to 4.6% in June 2012. Reliance Equity Opportunities is another such fund which has reduced its exposure from 15% in 2007 to under 5% (approx.) in 2012. Interestingly all these funds have outperformed BSE 200 over 3 and 5 years. On the other hand, the maiden sector fund focused on Capital Goods has severely suffered and has underperformed both, Top 10 funds (by AUM) and the BSE 200.

How the Funds Have Fared?

(NAV data as on July 17, 2012; Standard Deviation and Sharpe ratio is calculated over a 3-Yr period.

Risk-free rate is assumed to be 6.37%)

(Source: ACE MF, PersonalFN Research)

Road Ahead..

There has been a strident demand made by Corporate India to RBI for reducing policy rates. The policy rates have been entirely held responsible for the lackadaisical capital expenditure. However, there have been other issues which are as important as the high interest rates; however they have been conveniently sidelined by exaggerated demands for the rate cut.

Falling interest rates would definitely provide some relief to capital goods sector which is in a dire state but to resume the growth path it would need much more than cheaper credit. For example, bleak outlook for heavy electrical manufacturers wouldn’t improve with falling interest rates. It would need government action on rationalizing import duty structure which will make the level playing field for Indian manufacturers which are hit badly by the cheap Chinese imports. This issue has been awaiting action at least for last 2 years. The process of imposing import duties is in the final stages now. This means, the government has taken over 2 years to reach a solution. There have been inter-ministerial differences, both lobbies, power generators and the equipment manufacturer, have been seeking favor; both have the national interest as priority at least they say so. So far, the power generation lobby has been stronger; lead by some prominent private players. Many of them have been importing equipment from Chinese companies which come 15%-20% cheaper and are delivered faster than the Indian counterparts.

It is often argued by the power generating companies that costly Indian equipment eats into their margins and the time lag taken by the manufacturing companies to deliver orders delays the commencement of projects. Furthermore, the costly equipment increases the cost of electricity to the end user. We believe that power generators would still save cost if the coal is available on time and at a right price. But the government is hesitating to break the monopoly of Coal India. And more importantly, the cost of power to the end user is going up instead of cooling off. This mess is called "policy paralysis", a phrase that has been made popular by the news channels nowadays. Unless this is cleared up, no monitory policy will help review the sector. Issues such as environment clearances and the land acquisition are also impeding growth of the sector

End Note:

As far investment in capital goods sector is concerned, some prominent funds are keeping the sector at arm’s length. Taking a contra call on the sector would require a lot of courage and would also involve great deal of risk of earning poor returns on investment. Unless the policy reforms are implemented religiously and the borrowing cost comes downs at least a bit; revival of the sector looks a daydream. Fools rush in where angels fear to tread. This is more evident in the investment world.

Add Comments