|

| July 07, 2017 |

|

|

|

|

Impact

Multiple finance-media forums have been reporting how the conundrum of Non-Performing Assets (NPAs) has marred the progress of Indian Public Sector Banks (PSBs).

Now even non-savvy investors know about the asset quality problems Indian banks are facing. But they tend to overlook that their investments in debt funds can meet with the same fate—if the fund managers managing them don’t remain vigilant about the asset quality.

After all, debt funds invest heavily in securities issued by corporate entities. There’s always a chance that, like companies miss repayment timelines while repaying bank loans, they can also dishonour commitments made to debt funds as well.

The good part is— Securities Exchange Board of India (SEBI)—the capital market regulator, is aware of the elephant in the room. And, of late, it has doubled efforts to safeguard the investors’ interest.

Continuing on this drive, SEBI recently warned fund managers against complacencies in doing risk assessment. The recently appointed SEBI chief, Mr Ajay Tyagi, remained hopeful that the fund managers will exercise due diligence and demonstrate dexterity in managing the investors’ legitimate money.

Addressing the mutual fund industry honchos at the AMFI (Association of Mutual Funds in India) Summit, Mr Tyagi said, “You need to be more watchful. You have to make sure non-performing assets don’t get shifted to MF portfolios by way of transfer of debt”, Ajay Tyagi, chairman of SEBI, said on Thursday.

"There are instances of default on debt portfolio, so naturally MFs need to strengthen their due diligence and evaluation mechanisms, and not only depend on credit rating agencies,” he also added.

Over the last few years, mutual funds houses have lost money in debt securities issued by some of India’s troubled corporates such as Amtek Auto and Jindal Steel and Power Limited (JSPL). Mark-to-market losses have also been higher in funds that assumed greater risk in search of higher returns.

At the conclave, he also touched upon a whole host of other issues such as the apathy of mutual fund houses to vote at board meetings of companies where they allocate the investors’ money. Investor education, responsible approach to ad campaigns, and prudent spending there on and the merger of similar schemes were some other issues Mr Tyagi highlighted.

How can you assure that your investments in mutual funds are not at risk?

- Once you trust a fund house with your money, you hardly have any say in deciding how it actually does manage your money. Therefore, you need to select a debt fund cautiously and prudently.

- Before you decide on which fund to invest in, you should consider your time horizon, financial goals, and risk appetite.

- Invest as per your personalised asset allocation.

- Long term debt funds shouldn’t acquire more than 20% weight in the fixed-income part of your portfolio.

- Don’t invest in funds that have a history of taking excessive risks. Prefer process-driven fund houses instead.

- A record of the consistency a mutual fund scheme sustains across timeframes and interest rate cycles is a crucial parameter to shortlist schemes for your portfolio.

In case you aren’t sure about which debt funds to invest in, please subscribe to PersonalFN’s premium mutual fund research report—DebtSelect.

|

Impact

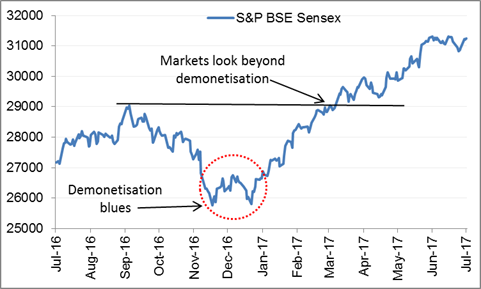

Stock markets reflect people's opinion about an economy.

So when the BSE Sensex hits an all-time high in India, it suggests investors are optimistic about the future of the Indian economy. Needless to say, when the bellwether stock market index touches new lows it suggests that investors are inclined to be more pessimistic about the future.

But like the weather in the Andaman Islands, market opinion swings too quickly without fair warning. This confuses the majority of investors. Big money is made or lost when the market is in a confusing state.

You will find some eternal bulls on the one side of the spectrum who keep reiterating the good things about the stock markets, almost always. And there will be the perennial bears on the other hand who will be consistently engaged in fault-finding and painting a gloomy picture.

But if you want to be a successful investor, you can't be friends with any of these camps forever. Do you remember how diverse the opinion of experts was about the demonetisation and its impact on the Indian economy?

Is GST going Demonetisation way?

(Source: BSE, PersonalFN Research)

Looking at the movement of equity indices, it seems markets are no more interested in perceiving demonetisation as a threat. But the general market opinion about the same event was negative around 6 months ago.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

The revolutionary Goods and Services Tax (GST) is probably affecting every area of your life.. Be it, daily necessity or a luxury. And if you are looking to buy gold in the near future, you might have to shell out little more money.

Here's why...

After much debate, GST on gold is set at the rate of 3% as against to 2.2% (1% excise duty and 1.2% VAT) charged earlier. Additionally, the existing 10% import duty on gold remains the same. Plus, the service tax on jewelry making charges will be levied at 5%. But on the bright side, implementation of GST will have a positive impact on the gold industry.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

The real estate sector has been going through some crucial changes lately.Demonetisation discouraged cash dealings involved in the sector, while the implementation of Real Estate(Regulation and Development) Act made builders more accountable. The sector is likely to streamline further after the implementation of Goods and Services Tax (GST).

If you are a real estate buyer and willing to acquire a ready-to-move property, you will have to shell out more after the implementation of GST. New and under-construction properties will attract 12% GST (Stamp duty and registration charges will be additional.)

As compared to previous rates, the GST rate is higher by around 3%-4%, even after considering the difference in the Value-Added Tax (VAT) charged under various states in the previous taxation system. This will make ready-to-move properties relatively expensive.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

If you have received a bill and looked at the details toward the end, there were cesses added that lightened the weight of your wallet.

Good news is, that's changed!

Although, the transition to the new direct taxation system is a difficult one, Goods and Services Tax (GST) is expected to be a boon for the country.

And already some positive effects have begun to take effect.

For one, cesses were charged on the tax collected and used for a particular purpose. While we are accustomed to paying various cesses such as Krishi Kalyan cess and Swachh Bharat cess to name a few, the good news is these cesses will not be applicable now.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

The weekend might have turned out to be a tad bit more expensive for those who enjoy to shop, eat out, or watch movies or do all of the above at a shopping mall. Yes, the Goods and Service Tax (GST) that came in to effect from midnight of July 1, 2017 would have caught many on their weekend outings by surprise.

Foodies, shopaholics, and regular cinemagoers will now have to shell out more for their goodies.

- Air-conditioned restaurants are now pricier with a GST rate of 18%, up from the effective 5.6% tax rate earlier.

- Apparels costing above Rs 1,000 will attract 12% tax compared to 5%, while footwear priced above Rs 500 with attract a GST of 18%.

- Movie tickets above Rs 100 will cost more with 28% GST.

- Therefore, if you enjoy weekends out, it is likely to affect your budgeted expenses.

While GST may lower prices for regular household items, your lifestyle choices will determine whether your outgoings will grow or decline in the coming months with the effect of GST.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

Goods and Services Tax (GST) has finally become a reality as of July 01, 2017. The Mutual Fund industry which usually sees any macro-level change as an opportunity to grow its Assets Under Management (AUM), couldn't hold itself back this time either. Habitually, mutual fund houses strike when the iron is hot, aiming to build up their future.

Storytelling is an art, and without a shadow of doubt, mutual funds certainly seem to know how to spin tales.

To read more about this story and Personal FN's views over it, please click here.

|

If tomatoes, carrot, peas, and ginger are part of your daily diet, you are likely to shell out more. Due to the mismatch in demand and supply, possibly on account of hoarding and black marketing, vegetable prices are raising eyebrows across States. Last week, the price of tomatoes shot up in the northern states and in last few days, southern states too have witnessed a sharp rise in wholesale prices, leading to even higher retail prices. The price of vegetables is an important constituent of the Consumer Price Index (CPI), which gives investors and analysts a picture of the retail inflation.

|

How Should Doctors Take Care Of Their Financial Health

How To View And Read Form 26AS

|

Mark To Market - MTM: Mark to market (MTM) is a measure of the fair value of accounts that can change over time, such as assets and liabilities. Mark to market aims to provide a realistic appraisal of an institution's or company's current financial situation.

2. The accounting act of recording the price or value of a security, portfolio or account to reflect its current market value rather than its book value.

3. When the net asset value (NAV) of a mutual fund is valued based on the most current market valuation.

(Source: Investopedia)

|

Quote: Everyone has the brainpower to make money in stocks. Not everyone has the stomach" - Peter Lynch

|

|

|

|

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 16 Jolly Maker Chambers II, Nariman Point, Mumbai 400 021 . Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667

SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013

|