Retirement: the golden years of your life. After a lifetime of hard work, the years of life where you want to live peacefully, doing things you have always longed for – going on a long vacation with your family, farming, teaching, devoting quality time to grandchildren, social service, and so on.

Have you dreamt about what you plan to do post-retirement?

Whatever may be your plans, one thing's certain: you'll need to make enough money for the rest of your life without a pay check.

They say, "the early bird catches the worm". Similarly, start your financial planning early for retirement; in fact, as soon as you receive your first pay check is imperative. Don't live under the misperception that there's ample time before you hang your boots and opportunities will come your way.

Mind you, retirement planning warrants utmost financial discipline together with prudent investing.

In this article, we'll find out if the National Pension System (NPS) and Public Provident Fund (PPF), the (most) commonly used retirement avenues, are good enough to live a blissful retirement…

First, let us understand the two products individually.

National Pension System (NPS) – This is a retirement product offered by the Pension Fund Regulatory and Development Authority (PFRDA), established by the Government of India to provide pension, and make our country a pensioned society.

NPS is a voluntary defined contribution scheme for those in the unorganized sector (UoS). Therefore, the pension you receive depends on the retirement corpus accumulated over the years.

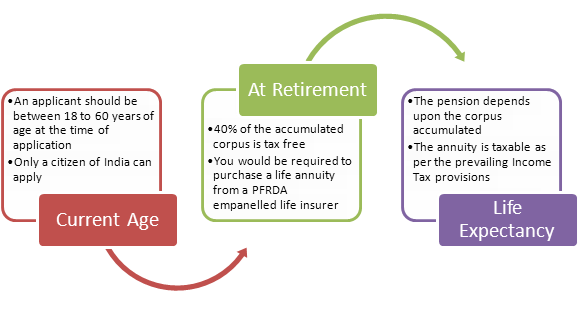

Here's a snapshot of how it works:

(Source: PersonalFN Research)

Public Providend Fund (PPF) – This retirement avenue is also a scheme of the Central Government, framed under the Public Provident Fund Act, 1968. Briefly, PPF is a Government backed long-term small savings scheme, which was initially implemented to provide retirement security to self-employed individuals and workers such as for e.g.: Shop owners, freelancers, SMSE staff without EPF facility in the unorganized sector. This has been every Indian citizen's darling investment avenue; most of the older generation have utilized to plan their retirement and is popular along with EPF.

The contributions (i.e. investments) made to the PPF account, will earn you tax-free interest and the maturity proceeds are exempt from income-tax. But keep in mind your liquidity needs, because under PPF your hard-earned money is blocked for 15 years.

One yearly withdrawal is permitted starting from your seventh year (through application vide Form C). The first withdrawal can be done after the expiry of 5 full financial years, from the end of the year in which your initial subscription was made. This means that from the day your account is open, you will need to complete 6 full financial years before you can make any withdrawal. Thereafter, you can make one withdrawal per year.

The amount of withdrawal will be limited to 50% of the balance in your account at the end of the fourth year, immediately preceding the year in which the amount is to be withdrawn, or the balance at the end of the preceding year, whichever is lower.

Here's a snapshot of the features of PPF account:

| Eligibility |

You need to be a Resident Indian Individual |

| Entry Age |

No age is specified (Minor is allowed through guardian) |

| Interest rate |

7.90% p.a. compounded annually* |

| Tenure |

15 financial years (plus the first year of investment)

On completion of 15 years, the account can be extended in a block of 5 years |

| Minimum Investment |

Rs 500 p.a. |

| Maximum Investment |

Rs 1,50,000 p.a. (A maximum of 12 deposits allowed in a financial year) |

| Tax Benefit |

Up to Rs 1,50,000 under Section 80C;

Interest earned is exempt from tax and so are the maturity proceeds |

| Can be opened at |

Any Post Office and authorized branches of some Banks |

| Who cannot invest |

Hindu Undivided Family (HUFs); Non Resident Indians (NRIs); and Person of Foreign Origin |

| Mode of Payment |

Cash / Crossed Cheque / Demand Draft / Pay Order / Online Transfer in favour of the Accounts Officer |

| Nomination |

Nomination facility is available |

*The interest is subject to change.

Since April 1, 2016 vide an office memorandum, the Department of Economic Affairs—Budget Division (under the Ministry of Finance, Government of India) has been revising the interest rates for Small Savings Scheme (SSS) which PPF is a part of.

Pursuant to the recommendation of Shyamala Gopinath Committee, interest rates on the SSS parallelly to that of money market rates and are reviewed every quarter based on the G-Sec yield of the previous three months vis-à-vis the erstwhile practice of reviewing annually.

PPF rates over the years

| Period |

Interest Rate p.a. |

| 01 April 1986 - 14 Jan 2000 |

12% |

| 15 Jan 2000 - 28 Feb 2001 |

11% |

| 01 March 2001 - 28 Feb 2002 |

9.50% |

| 01 March 2002 - 28 Feb 2003 |

9.00% |

| 01 March 2003 - 30 Nov 2011 |

8.00% |

| 01 Dec 2011 - 31 Mar 2012 |

8.60% |

| 01 April 2012 - 31 Mar 2013 |

8.80% |

| 01 April 2013 – 31 Mar 2016 |

8.70% |

| 01 April 2016 – 30 Sept 2016 |

8.10% |

| 01 Oct 2016 – 31 Mar 2017 |

8.00% |

| 01 April 2017– till date |

7.90% |

(Source: ACE MF, PersonalFN Research)

And over the years, as seen in the above table, PPF rate have been on a downhill. In April 2017, the Government lowered the PPF rate to 7.9%.

So, is saving through these pension funds enough?

Well as far as PPF goes, it still can't be said that it has become a redundant investment. It fetches you a decent rate of return which is tax-free at maturity and the contributions you make, too, are eligible for a tax deduction under Section 80C of the Income-Tax Act, 1961. Effectively PPF still enjoys an Exempt-Exempt-Exempt (E-E-E) status. So, if you are keen on a safe corpus, earning a decent tax-free rate of return, enjoying tax benefit; PPF is for you.

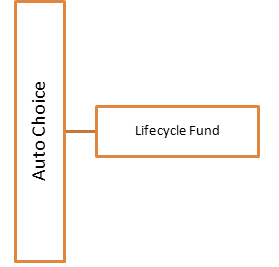

Coming to NPS, it also allows you, the applicant, freedom to decide where you wish to invest your hard-earned money vide two options: Active Choice and Auto Choice.

|

|

| (Source: PersonalFN Research) |

Under the Active Choice, the entire pension wealth can be invested in Asset Class C (Corporate debt) or G (Government securities) and up to a maximum of 50% in Equity (i.e. Asset Class E). While those investors lacking knowledge to manage their NPS investment can opt for Auto Choice (i.e. Lifecycle Fund). Here, the fraction of funds invested across three asset classes will be determined by a pre-defined portfolio.

Besides there's Tier-I and Tier-II account. If you opt for the Tier-I Account, which is a non-withdrawal account, you aren't allowed to withdraw the contributions made. The objective is to instil the needed financial discipline to build a retirement corpus.

The good news is, as an applicant under Tier-I account, you are eligible to claim tax benefits upto Rs 1.5 lakh under Section 80CCD(1) in case for mandatory deduction from salary. This deduction is under the overall Rs 1.5 lakh limit under Section 80C. However, if your company contributes i.e. upto 10% of basic pay into NPS on your behalf as an employee, the deduction under Section 80CCD(2) is not restricted. Further, under a new Section 80CCD(1b), as a tax payer if you voluntarily contribute to NPS additional tax benefit upto Rs 50,000 is eligible.

On the other hand, Tier II Account is a voluntary savings account and it isn't linked to retirement. An as an applicant, you are free to withdraw from this account as per your requirement but aren't eligible to claim tax benefits on the contributions made.

Retirement Planning through mutual funds

A better way to create your retirement nest-egg is by investing in Equity Linked Savings Schemes (ELSSs), also known as tax saving funds, where you receive a tax benefit and you're exposed to diversified equity vide a fluid fund management style.

How have ELSS funds fared?

|

6 Months |

1 Year |

3 Years |

5 Years |

| Avg. Return of ELSS Funds |

21.18 |

26.19 |

15.92 |

19.72 |

| Avg. Return on PPF Account |

7.90 |

8.05 |

8.70 |

8.80 |

| Avg. Return of NPS Funds |

6.68 |

15.76 |

11.55 |

12.14 |

(Source: PersonalFN Research, ACE MF & www.valueresearchonline.com )

Equity Linked Savings Schemes (ELSS) over the long-term have delivered better returns vis-à-vis pension funds and PPF, albeit with a higher risk exposure. But their performance seems to be justifying the risk, if we consider the average Sharpe Ratio of 0.18. While this is just an average of the returns generated by ELSS, if you select the best mutual fund and even add other diversified equity mutual fund schemes to your portfolio, the chance of clocking better return is even more facilitating you to build a larger retirement corpus.

Plus, your portfolio would be far more liquid compared to PPF and NPS.

Besides, it will be unfair to expect equally high returns by your PPF account as compared to NPS and mutual funds.

ELSS funds have a lock-in of only three years and have the capability to create wealth over a period of time. You can also claim upto Rs 1.5 lakh for tax deduction under Section 80C .

Hence, while planning for a blissful retirement planning , complement investment planning with tax planning. If you have fairly a long investment horizon before you hang up your boots, consider taking a bit of risk and invest in ELSS and other diversified equity funds; because as you know interest rates on many SSS and tax saving FDs have gone down, plus they’re not tax efficient investment avenues.

Don’t flock to ELSSs in the last quarter of the financial year to save tax, or pick any diversified equity fund in the pursuit of living a blissful retirement. The key is in selecting winning mutual fund schemes for your investment portfolio, whereby you can create significant wealth for your retirement. PersonalFN’s FundSelect service can help you zero-in on the top-performing funds across varying market caps and investment style. Be it large cap, mid cap, multi cap, value-based, opportunities-styled or balanced funds, along with our top recommendations we highlight the underperforming or average performing ones too. With over 15 years’ experience in fund research, PersonalFN has established a methodology to select funds that beat the market by a whopping 70%! We highly recommend to opt for our unbiased, research-backed service here.

Adopt the prudent path to wealth creation. To mitigate volatility, opt for Systematic Investment Plans (SIPs) as they provide you the benefits of rupee-cost average and compounding.

Happy investing!

You can also access Personalfn EPF calculator here.

Add Comments