|

| November 06, 2015 |

| |

| Weekly Facts | | | Close | Change | %Change | | S&P BSE Sensex* | 26,265.24 | -391.59 | -1.47% | | Re/US $ | 65.24 | 0.07 | 0.11% | | Gold Rs/10g | 25,875.00 | -800.00 | -3.00% | | Crude ($/barrel) | 47.59 | 0.40 | 0.85% | | F.D. Rates (1-Yr) | 6.25% - 8.00% | Weekly changes as on November 05, 2015

*S&P BSE Sensex value as on November 06, 2015 |

Impact

If you keep binging on high-calorie food and live a sedentary lifestyle, you are likely to face weighty issues. On the other hand, for those who are already overweight and want to get fit, adapting a balanced diet plan and burning as many calories as they can is a healthy way forward.

Until two years ago, India depicted a similar hedonistic trait. The Indian Rupee was under tremendous pressure, as were India’s exports. However, mounting imports resulted in higher trade and current account deficits. An assessment of the working group by the RBI revealed that India was importing gold like there was no tomorrow and sitting idle on these heaps of precious metal. As a remedial measure, India decided to lower its dependence on gold and the Government took several measures in the past to attain this objective.

As a part of this attempt, India’s Prime Minister, Mr. Narendra Modi, recently sanctioned the following two gold schemes open to Indians:

- Sovereign Gold Bond Scheme 2015:This can be considered as a direct alternative to buying physical gold, or even gold Exchange Traded Fund (ETFs)

- The Gold Monetisation Scheme (GMS), 2015: This entails the government to collect physical gold from the public and pay 2.5% interest p.a. towards it (the minimum deposit size is 30 grams with no upper limit).

As an investor, you might be keen to know more about the Sovereign Gold Bond Scheme as it allows passively investing in gold.

Here are the salient features of the Sovereign Gold Bond Scheme 2015: - The bonds will be issued by the Reserve Bank of India (RBI)

- You are eligible to invest in bonds if you fall in any one of these categories; individuals, HUFs, trusts, Universities, charitable institutions.

- Non Resident Indians (NRIs), Foreign Institutional Investors (FIIs), or foreign nationals are not eligible to invest.

- You need to buy minimum of 2 units and in multiples of 1 unit thereafter. (1 unit of the scheme is equivalent to 1 gram of gold). There is an upper limit of 500 grams per person per Financial Year (FY)

- The interest will be paid at the rate of 2.75% on initial value of investment. The frequency of payment will be once in six months

- The bonds will mature for repayment after 8 years. However, an exit option is available after 5 years.

- The bonds can be held in demat or in a paper form as a certificate.

- The Price of Bond will be fixed in Indian Rupees on the basis of the previous week’s (Monday–Friday) simple average of closing price of gold with a .999 (point 999) purity published by the India Bullion and Jewellers Association Ltd. (IBJA).

- The tax treatment remains the same as it is for physical gold. The interest component is taxable too.

- The bonds will be tradable on exchanges from a date that the RBI will notify in future.

PersonalFN is of the view that the Sovereign Gold Bond Scheme 2015 is an attractive scheme for investors. Apart from opportunity to benefit from appreciation in gold prices, the additional interest offered by the scheme makes it a good alternative to Gold ETFs.

Before you rush to the nearest post office or to your bank for investing in the scheme, please note that if gold prices depreciate, the Government won’t bear your loss. No other avenue offers you that assurance either. So if you want to diversify your portfolio, consider investing in this scheme. PersonalFN maintains that you should have 10%-15% of your investment portfolio in gold.

Do you think the recently launched Gold Bond Scheme is an attractive investment option? Share your views here

|

Impact

The glaciers are likely to melt faster this winter.

If you think this is to do with the rising temperatures this winters; you’ve probably missed the context. The statement was in reference to the possibility of the sudden slippages from the market peaks. Whether it’s glaciers melt or toppling markets, the results would be pretty similar—unpleasant and maybe devastating.

Rising temperatures, changing weather patterns, depleting snow-caps and shrinking ocean ice layers are the results of global warning. Draughts in California, floods in Florida, deficient rains in India, and typhoons in China showcase how erratic the climatic conditions are these days. Intriguingly, climatic changes share a bizarre similarity with market shifts. Just as global warming causes most of the climatic changes witnessed today, synchronised monetary policy interventions of central banks across the globe affect world markets.

For a while, the elephant in the room has been the Federal Reserve’s (Fed) monetary policy stance in the United States. Many experts believe a likely reversal in the policy stance of the Fed, i.e. it hiking the interest rates, has already been factored in by markets. However, the fact is the Fed has been flirting with markets for considerable time now. It has kept its plans under wraps, giving rise to uncertainty and speculation. If the Fed actually hikes rates, emerging markets may be worst-hit places.

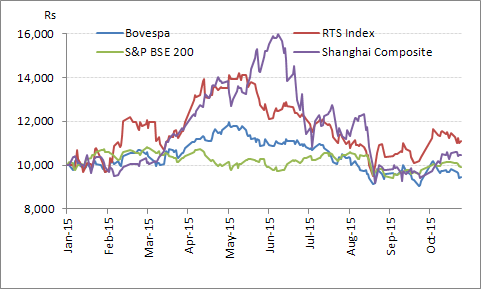

Data as on November 02, 2015

(Source ACE MF PersonalFN Research)

The chart above shows you, Indian markets depicted extremely insipid movement from the beginning of 2015 till present day. This happened despite reasonably well-placed fundamentals. On the contrary, Russia proved to be the best place for investors in the BRIC pack (Brazil, Russia, India and China). The trend is clear. Investors are dumping expensive markets and preferring inexpensive alternatives. Brazilian equities are the most expensive among the four, while Russian equities are the most inexpensive. India stands as the second most expensive market among four.

A Market meltdown might be at the door step…

India has shown no significant recovery in spite of investors having high expectations from the NDA Government. Yet, little has changed at the grass root level despite the Government efforts on several fronts. It seems that it lacks the required strength in the Rajya Sabha to pass crucial bills, and looks handicapped for introducing strong legislative reforms. Under such circumstances, global liquidity has been propelling the Indian markets. Consequently, should the Fed hike rates, the liquidity scenario may change swiftly.

Commenting on likeliness of the Fed hiking rates in the December meet, the Fed Chair said, “What the committee has been expecting is that the economy will continue to grow at a pace that is sufficient to generate further improvements in the labor market and to return inflation to our 2 percent target over the medium term. If the incoming information supports that expectation then our statement indicates that December would be a live possibility.”

The Fed is scheduled to meet mid-December and this is an important event to track in the near future. Flows to Indian markets, thus, may be affected for two reasons: first, the decision of Fed; second, the year-end profit booking.

Other important factors to watch out for:

Outcome of Bihar election:Although sentimental, the poll results in Bihar will have their bearing on Indian markets. If the NDA losses out to the Nitish Kumar led grand alliance, it will not only affect the chances of the NDA Government to improve its tally in Rajya Sabha, but also signals the ebbing popularity of Modi led NDA among the masses. India’s political climate vastly affects the sentiments of global investors.

Success of the winter session: The winter session is very crucial for the NDA Government as it aims to table new bills and pass a few bills pending for the parliamentary node for long time. :

Growth in Corporate Earnings: The development is unfortunately found only on the electoral manifestos. Corporate earnings continue to disappoint despite the number of advantages such as falling crude oil prices and the relatively stable Rupee value.

What to do?

For one, avoid getting carried away by the market movement. If you are investing in equity markets through mutual funds, it’s better to stagger your investments for now as markets are likely to experience a bumpy ride ahead. Best opt for Systematic Investment Plans (SIPs), which is the best way to deal with market volatility. If the proportion of equity assets in your portfolio has crossed the desired limit, mentioned in your personalised asset allocation, now is the time to rebalance.

|

Impact

When you go to a shopping mall, the transaction is quite simple. You look for the things you want to buy, check the price tag and offers, and pay the cashier for your purchases. The end. It's hassle-free and the store manager doesn't inquire about your personal details, buying habits, colour preferences, etc.

But when you go to a bank or any other financial institution, this includes a mutual fund or an insurance house, you will be asked to divulge bits of personal information. This process is called Know Your Client (KYC). So every institution, from a bank to an insurance company or a stock brokerage house, would like you to be KYC-compliant.

Why KYC?

When a financial transaction is accomplished by money obtained through illegal means or performed as an attempt of avoiding tax; the Government loses revenue. On the other hand, the ownership of any asset obtained by deceiving authorities can be morally hazardous. In brief, the Government has to know the source of money and pattern of ownership for every financial transaction. The KYC records help specifically in this endeavour.

To know more about this and PersonalFN’s views over it, please click here.

|

Impact

"I bargain for the best deal."

"I need to earn more to improve my lifestyle."

"I have two job opportunities to choose from; which one will be the best for me?"

The human mind constantly seeks, creates, and evaluates options...

This ability makes us human beings special. But, there are always influencers that affect our decision making process. Sometimes, what you are convinced about may actually be disadvantageous to you. Interestingly, greed and fear are two forces that always volley at the back of our minds when making a decision. If we part ways with rationality, we may end up making wrong decisions.

Let's say, you want to borrow money. First, you'd understand why you want to borrow and then may decide from whom to borrow, depending on the rate of interest and attractiveness of the deals. Here, you want to save as much as possible. You expect zero-loan processing fees, the lowest possible interest rate, and lenient repayment conditions. Clearly, the driving force is fear. You don't want to lose money just because you couldn't get the best deal. You'd also keep an eye on the repayment schedule. The chances of making a wrong decision could arise when you pay too much attention to saving the interest cost, while ignoring the catch in repayment rules.

To read more about this news and our views, please click here..

|

The festival of lights, Diwali, is around the corner and a shopping frenzy for clothes, gadgets, home appliances, new LED lights, and of course sweets commences. Nobody really wants a budget constrain when enjoying shopping and so many opt for festival loans.

In addition to using credit cards, people have started borrowing against their fixed deposits as well. This happens when banks slow down on disbursing consumer loans and lending against shares. In the recent times, the vehicle loan category has dipped too however, loans against fixed deposits have increased to 13.0% this season as against the 8.0% decrease recorded last season.

PersonalFN believes an alternative is worth considering is though it’s perfectly acceptable to spend this festival season, it always helps to ensure you don’t overshoot to the point where your borrowing begins affecting your finances negatively. Alternatively, plan your goals in advance, save to fulfil them and enjoy festivals the way you want to, without putting pressure on your finances.

|

Collateral: Property or other assets that a borrower offers a lender to secure a loan. If the borrower stops making the promised loan payments, the lender can seize the collateral to recoup its losses. Because collateral offers some security to the lender in case the borrower fails to pay back the loan, loans that are secured by collateral typically have lower interest rates than unsecured loans. A lender's claim to a borrower's collateral is called a lien.

(Source: Investopedia)

|

Quote : "People who lie to themselves about investing are the same as overweight people who blame their genes for their obesity" - Robert Kiyosaki

|

| |

| © Quantum Information Services Pvt. Ltd. All rights reserved.

Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667 |