As we are approaching the end of the financial Year 2013-14, we are sure that many of you may be looking for some tax savings investments. Our experience reveals that, very often investors opt-in for a life Insurance policy, which offers the feature of an insurance-cum-investment plan in their endeavour to save some tax as well as earn a return on their investment. ( Download our: Equity Guide for FREE to know how to build a stock portfolio)

You see, while there are various types of Life Insurance policies which can help you save tax, in this article we shall compare an Endowment Policy to a Money Back Policy and try to analyse which could suit your requirement better.

But first let’s understand what these policies mean.

Endowment Policy

It is a Life Insurance policy in which part of the premium paid is utilized towards providing insurance cover, the rest of the portion is invested. The invested amount provides you the return at the time of maturity.

Money Back Policy

Here as well, a part of the premium paid is utilized for providing an insurance cover while the rest of the premium portion is invested. The fundamental difference between an Endowment and a Money Back policy is that, the insured get survival benefits at regular intervals in addition to the maturity value. Survival Benefits are generally 20-25% of Sum Assured (SA) which is paid after every 4-5 years.

Now that the difference between the two is known to you, let’s dig a little deeper and evaluate each of them with the help of an example.

| Policy Details |

Endowment Policy |

Money Back Policy |

| Sum Assured |

1,000,000 |

1,000,000 |

| Policy Term |

20 |

20 |

| Premium |

48,353 |

63,796 |

| Maturity Value |

1,910,000 |

1,220,000 |

In the above table we have considered premiums for a 30 year old individual with a sum assured of Rs 10 lakh and for 20 year policy term, for both Endowment and Money Back policy. The Endowment policy premium is Rs 48,353 and maturity value is Rs. 19,10,000. The premium for the Money Back policy on the other hand is Rs 63,796 and offers a maturity value is Rs 12,20,000. As you have observed, the Money Back policy is charging a higher premium and providing less maturity value than the Endowment policy. This is because; the Money Back policy will also provide Rs 2 lakh as survival benefit after every 5 years.

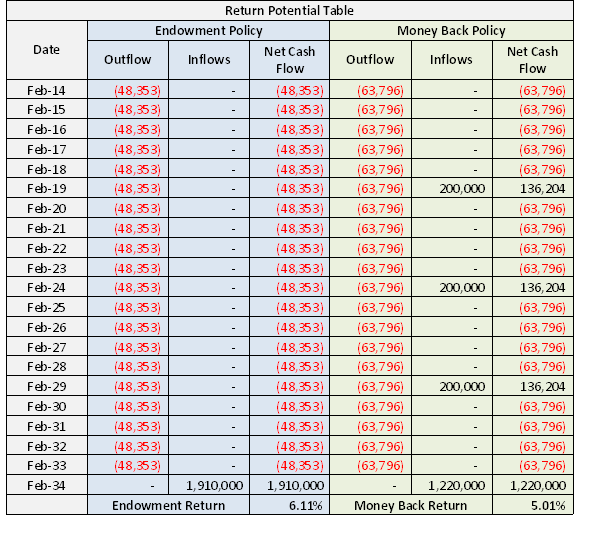

Now let’s have a look at the return potential of these 2 policies:

In the above table we have considered premium as an outflow and maturity proceeds & survival benefit (applicable only in case of Money Back policy) as an inflow. Net Cash flow is: inflow minus outflow. As evident from table above, the return in case of the Endowment policy is higher than the Money Back policy, although money back policy is providing cash flow before maturity as well. So it means that we can expect around 6% returns from Endowment and Money Back policy with + 1-2%. (

Also Read:

Is Your Endowment Policy A Waste of Your Money? to know whether to Continue or Surrender if you already have an Endowment policy)

Which is better?

It is noteworthy that considering long term of such policies, the return on investment is too low. Even if you want to invest in the safest investment, then investing in a

Public Provident Fund (PPF) which provides a return of 8-9% p.a. and at the same time offers the much required tax benefit to you (just as what a life insurance does) is a better option. So at PersonalFN, we do not recommend investing in such policies neither to indemnify risk to life nor from a tax saving and return generation point of view. For indemnifying risk to life and to fetch a tax benefit (on account of premium paid), a pure term insurance plan is the ideal most, as the cost-to-benefit derived from such a product is optimal. For example, a term insurance plan from the Life Insurance Corporation (LIC) of India for a 30 year old individual with the same sum assured of Rs 10 lakh for a policy term of 20 years costs a meagre Rs 3,393. So you can clearly see the difference in premium of Term Plan vis-à-vis Endowment plan and Money Back plan.

Remember, it is imperative to separate your insurance needs from investment needs for optimal return generation and save tax the prudent way. (

Download our: Tax Guide for FREE to know how to you can save tax on your hard earned money)

Add Comments