When Mr. Narendra Modi was the Chief Minister of Gujarat, he took potshots at the UPA Government for its ineffective economic policies. As Prime Minister, one would naturally expect his Government to take corrective steps to get the economy back on track. While it remains the job of the Government to analyse what went wrong in last 1 year and 6 months; the fact is, nothing has changed significantly at the grass-root level.

So far we’ve seen only the opposition slamming the Modi Sarkar for failing to deliver on promises made before the 2014 Lok Sabha Elections. However now, the dissent has been growing among his party leaders. Sure, the Prime Minister is doing all the hard work and visiting nations, trying to strengthen bi-lateral and multi-lateral relations, attracting foreign investments and attention. But when you look at numbers screaming neon-bright—the economy isn’t out of the woods yet. Take the example of the recently released data on industrial growth and retail inflation.

Here’s how it works. The Index of Industrial Production (IIP) that captures the level of industrial activity and the Consumer Price Index (CPI) that tracks trends in retail inflation are two important economic indicators. Currently, they appear discouraging.

Sagging growth and escalating inflation

|

|

|

Data as on November 12, 2015

(Source:MOSPI, PersonalFN Research)

|

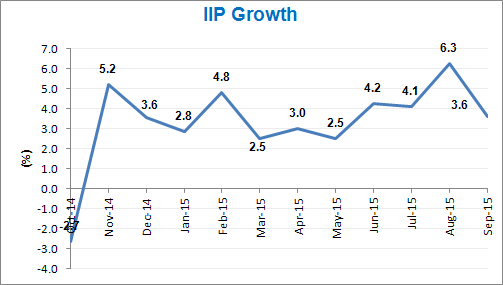

Growth in industrial output as measured by the movement of IIP fell to 3.6%, a 4-month low point in September.

IIP fell to a 4-month low in September

- Manufacturing growth looked disappointing at 2.6%

- Capital Goods segment grew at 10.5%, but it failed to pump up manufacturing growth

- Activities in Electricity and Allied sectors gathered pace, sector posted 11.4% growth

- Mining continued to rumble under pressure, growing at 3.0% in September

- At 8.4% growth in consumer durable looked pinkish but the non-durable segment disappointed at a fall of 4.6%

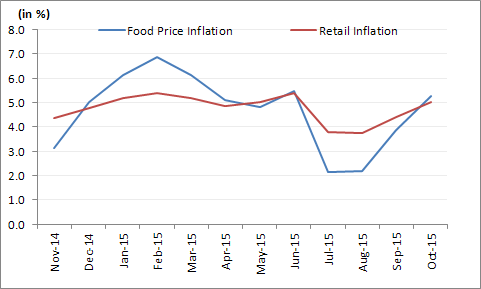

On the other hand, retail inflation measured by the movement of CPI shot up to 5.0% in October 2015 as against 4.41% in September 2015, and 4.62% in October 2014. Food inflation rose sharply to 5.25% from 3.45% in September 2015, and 3.88% in October 2014.

No respite from rising prices

- Inflation in Clothing and Footwear stayed high at 5.62% in October 2015

- At 5.32% in the Fuel category and 5.34% in Health, inflation remained above the average inflation

- Prices of pulses rose at whooping 42.2% in October 2015

- Snacks and sweets became dearer by 6.83%

- Prices of spices rose about 10%

Market reaction

Markets have been on the downward spiral for a number of reasons. Adding to investors’ woes, IIP and CPI numbers turned up very weak indeed. As a result, the market reaction was negative. Let’s face it, markets weren’t hoping for a significant recovery, but there was a general expectation that the numbers wouldn’t be as discouraging as a “lost cause”. A spike in the prices of pulses has been a significant area of high-pressure concern. It projects us at the mercy of vagaries of nature and India’s storage and distribution (mal)practices, and highlights the impact of constantly rising food prices on overall policy measures. As far as IIP is concerned, better performance of the manufacturing sector could have saved the day.

How RBI might read the numbers

The RBI has projected inflation to reach 5.8% by January 2015. This means, as long as the actual inflation stays below 5.8%, there won’t be much change in the policy. Having said this

, RBI will closely monitor the quality of inflation. If the food price inflation keeps climbing; at some point it will pressurise the central bank. to arrest the expectation of an inflation high, which is a negative for household savings. High inflation expectation delays the progress of investment cycles as corporations hold back their capacity addition plans.

What to expect?

While the Modi Sarkar is busy launching high profile campaigns such as “make in India”, our industry is still struggling. The confidence of business houses appears low, which is why they are still shying away from committing big-ticket investments. While the PM has been trying to influence the global investor community, the harsh reality is that—his Government is struggling to pass some important bills such as Good and Service Tax (GST) on home soil. To start a business, investors and corporations will have to pass through many bureaucratic hurdles. And though India’s ranking on the World Bank’s list of “ease of doing business” has slightly improved, overall its image remains very low. The Government is challenged to change this environment.

Developmental agenda is feared to have taken a backseat. Intolerance has started polluting the social environment. Such instances, affect the sentiment of investors and corporates. The Government claims it’s trying hard to rein but going by the flatline developments at the grassroots level, situation seems unlikely to change soon.

In other words, the seesaw movement of IIP and CPI may start making investors crankier and the market shakier. The time has come to be more cautious than liberal about future market movements. The question remains on the monetary policy stance, the central bank is likely to remain consistent with its accommodative monetary policies; however, further rate cuts would squash expectations of any recovery, let alone growth.

Investors should:

- Stay calm

- Remain invested

- Avoid speculation

- Stick to their personalised investment plans

- Follow their personalised asset allocation

Unfortunately, political parties turn 180 degrees on their views of the growth agenda when they are in opposition, as compared to when they’re in the Government. Growth continues to suffer in any case.

Add Comments