Impact

The status quo on policy rates at the RBI's second bi-monthly monetary policy review may not have surprised those who understand the monetary policy stance of Dr Rajan. As pointed out, the unexpected rise in retail inflation during April 2016 has been a cause of concern for policymakers. Lower inflation has always been a precursor to accelerated economic growth. The Government has been dreaming about achieving 8% + economic growth and has been appealing the opposition to allow more reforms.

Any discussion about reform-led growth would be incomplete without having a mention of the Goods & Service Tax Bill (GST), considered to be a revolutionary change in India's taxation since independence. Many experts and industry veterans have predicted that a neatly devised GST can lift India's GDP by 2.0%.

Despite having grabbed so much of attention, the GST Bill remains stuck in the Rajya Sabha where the Congress and other opposition parties have adequate numbers to impede the passage. Nevertheless, the Government has gone all out to persuade the Congress, yet thus far all efforts have gone in vain. The Congress has submitted three demands, which it insists, should be fulfilled, if the Government expects it to support GST.

The demands are...

- Incorporate the GST rate of 18% in the Constitution Amendment Bill;

- Eliminate the provision that allows additional levy of 1.0% for 'manufacturing' state; and

- A separate dispute resolution mechanism

Although the Government is willing to drop the additional levy and consider a separate dispute resolution mechanism, it has rejected the two other proposals. The Finance Minister has gone to an extent of calling this demand, "preposterous". Both the parties, the Congress and BJP are not letting any opportunity go to settle old scores. Contesting the demand of the Congress party, Finance Minister Arun Jaitley said, "The wisdom which dawned on my friends in the Congress party had not dawned on them when Pranab Mukherjee (the then finance minister) introduced the GST (in 2011)." He further made his point by questioning the silence on the issues that Congress raises now during the tenure of Mr P. Chidambaram. The parliamentary standing committee headed by Mr Yashwant Sinha, at the time, had also insisted that decisions on rates and other related issues should be taken through rules and laws rather than through Constitutional Amendments.

So do the demands of the opposition hold merit?

Congress vice president, Mr Rahul Gandhi has justified their stand saying: "We don't want any Government in this country to have an unlimited window of tax. We represent the poor people of this country. We represent the farmers. We represent the labourers. We do not want them to have a massive weight on top of them. We do not want Government servants and others to have a huge tax burden. That is why we want to put a roof on it. We want to put a limit on it. They (BJP) don't. That's the difference."

So, is GST really going to create inflationary pressure?

Well, there are fears that initially a tax rate of 18% may exert pressure on inflation. But to quell these fears, the Committee headed by the Chief Economic Advisor Dr Arvind Subramanian on Possible Tax rates under GST has already submitted its Report to the Finance Minister where it has proposed a two-rate structure.

Let's understand the structure of GST in a little detail...

The GST shifts the focus of taxation from the current origin-base taxation to destination-based tax. In other words, under the current tax regime the State in which the goods are produced, collects the tax. However, in the destination-based tax system, the consuming states collect the tax. This puts producing States at a huge disadvantage, especially in cases where there is more outbound trade. As compared to, the States that consume more and produce less tend to be reluctant to increase production leading to unjust treatment for producing states.

To overcome this difficulty, the rate of GST becomes crucial. Hence, working out a Revenue Neutral Rate (RNR) becomes necessary to offer a level playing field to all states. RNR is the single rate, which preserves Central as well as State revenues at desired levels. In practice, there can be a spectrum of rates, but for the sake of statistical clarity and precision, it is appropriate to think of the RNR as a single rate. So the rate of 18%, that the Congress has repeatedly been referring to is the single tax rate.

At present, the aggregate tax rate on manufactured goods considering various state and centre administered taxes runs as high as 25%-26%. Therefore, the assumption while arriving at the RNR is that lower effective tax rate on manufactured goods will offset the higher effective rate on services. At present, the services are taxed at 15% including additional levy of cess.

Accepting the demand of Congress to keep a constitutional cap of 18% will make the Government (of any party) run to the opposition to raise rates on alcohol and tobacco (the list runs long). These have been the items that all Governments have used to increase revenues quickly during times of economic slowdowns. On the other hand, having too many exclusions to lower RNR on other services would defeat the whole principle of GST.

Will the GST bill be passed in the monsoon session?

If you want to know the fate of GST in the coming monsoon session of Parliament, one can't ignore the remarks of Finance Minister, Mr Arun Jaitley. Here's what he said in a media interview, "a delayed GST is better than a flawed GST."

Once implemented, GST would be another factor RBI may have to, at least initially, consider while framing monetary policies.

The idea of capping the GST rate at 18% is as bizarre as allowing it to climb upto 25%, where it will offer no incentive at least from the taxation standpoint. Income tax, black money bill, and GST are closely linked.

But a well-designed GST can put strong checks on the corruption prevailing across tax departments. It would also act as the deterrent for those business people who generate black money through "unreported" transactions.

Impact

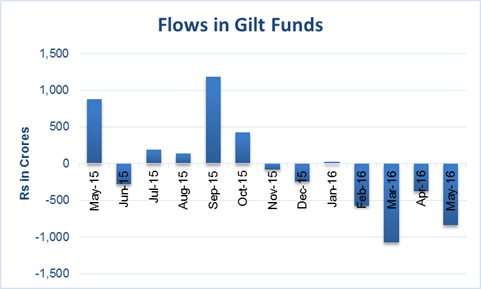

Ever since India adopted the approach to target inflation when framing monetary policies, investors of Government securities have become more cautious to inflation trends. The movement of interest rate is the single most important factor, besides political stability, that affects the flow of capital into Government securities.

Mutual Funds have been feeling the heat of outflows that have accelerated since February 2016. Since then, investors have pulled out Rs 2,854 crore from gilt funds, reflecting their bearish views on the interest rate movement. Unexpectedly high food inflation recorded in April 2016 was alarming as it made the future uncertain. The RBI intends to curb the retail inflation at 5.0% by March 2017. It made it clear at the second bi-monthly monetary policy that, the stance of the monetary policy will remain accommodative, but the future rate cuts would be subject to lower inflation and the improvement monetary transmission. However, both these factors face uncertainties. Implementation of 7th pay commission is also likely to put upside pressure on inflation. Therefore, investors have been keeping away from gilt funds, at least for now. In the recent past, the speculations about Dr. Rajan not getting an extension for the post of RBI Governor also drove investors away from gilt funds.

Gilt funds—losing flavour

Data as on May 31, 2016

(Source: AMFI, PersonalFN Research)

The Government has been working on taking out the bottlenecks in food supplies chains. Along with this, if better monsoon abates food price inflation, the RBI may signal more rate cuts. In such a case, investors might return to gilt funds.

PersonalFN believes, you shouldn't try to time the market speculating on some events. Although the movement of interest rates remains a crucial factor for investing in gilt funds that shouldn't be the only factor. You would be better off focusing on your risk appetite and time horizon. Unless you have a longer time horizon, investing in long-term gilt funds may prove to be risky.

Impact

When you have multiple choices with no real or identifiable differences, you are likely to buy two things almost identical. Mutual fund investors have been facing this dilemma for long. There have been multiple schemes from the same fund house which have similar features, orientation, and objectives. As a result, investors get more confused and end up either making a wrong choice or conclude, mutual funds are not meant for them. They are too complex. No wonder, the spread of mutual funds in India is extremely low.

Why mutual fund industry offers so many schemes when a few are enough?

In reality, a fund house can be very successful even with a briefer portfolio of select schemes. What it needs indeed is a unique product in each category. However, the work-shy mutual funds initially thought, they can satisfy their distributors by incentivising them to push their products. To garner higher Assets under Management (AUM) under existing schemes, it takes more efforts. Unless the scheme performs consistently and generates superior returns across market cycles, it becomes difficult to push the existing scheme.

On the contrary, swanky ad campaigns and aggressive promotion through channel partners who often lured potential investors by 10-Rupee NAV, helped mutual funds collect a good deal of money quickly through New Fund Offers (NFO). This country has witnessed how distributors and promoters sold 10-Rupee NFOs as if a company is coming with an Initial Public Offer (IPO) at a face value of 10. This created an illusion.

Today, every fund house has an extensive list of schemes whose performance has nothing much to speak about. Don't you find it weird that mutual fund houses offer two open-ended midcap funds along with a number of close-ended funds targeting midcaps? No matter how deeply a man loves his fiancée, he cannot buy her five engagement rings. A fund house might be bullish on midcaps, but what stops it from buying all stocks it finds attractive under one scheme?

Similarly, only fund houses can tell us, how they justify 3-4 offerings in the ELSS category and a couple of balanced funds and multiple Monthly Income Plans (MIPs).

To ready more about this story and Personal FN's views over it, please click here..

Impact

It is rare to find a person who doesn't want to make big bucks in quick time. Those active in equity markets often construe Initial Public Offers (IPOs) as a way to make sure shot gains at listing. Even the experienced investors forget that equity as an asset class is essentially for the long term.

The record says IPOs have been a mixed bag for investors. Some stocks such as Page Industries and Yes Bank which were listed in the last decade have become multi-baggers by making as high as 2,000% gains over their offer price. Yes, you read it right. Although these stories might excite you to go more bullish on IPOs; you should also take out time to read about failures. Can you forget the IPO of Reliance Power? The IPO, which hit the market at a time when laymen spoke like stock market gurus. The IPO which investors hoped to have provided eye-popping returns ruined their expectations.

To ready more about this story and Personal FN's views over it, please click here..

|

| © Quantum Information Services Pvt. Ltd. All rights reserved.

Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667 |