Company Overview

Muthoot Finance Limited (MFL) is a non-deposit taking Non Banking Financial Corporation (NBFC) headquartered in Kerala. Company has the long history of 72 years in the gold financing business. As of September 30, 2011, MFL is the largest gold financing company in India in terms of loan assets under management as per IMaCS Research & Analytics Industry Reports, Gold Loans Market in India, 2009 (IMaCS Industry Report, (2010 Update)). It has a branch network of 3,274 spread across 20 states. The total employee strength of the company is 21,543 as on the same date. The main business of the company is to lend against the pledged gold jewellery and used household gold.

Business Analysis

It generates its revenues mainly from the gold loan business. The total share of gold loan in the revenue pie of MFL was 99.01% for the year ended September 30, 2011. It also provides money transfer services through its branches, provides collection agency services (recently started) and has been operating three windmill projects in Tamil Nadu. Both the businesses have not been contributing much to the revenues of the company. MFL’s interest income has jumped from Rs 223.5 crore in March 2007 to Rs 2,012.6 crore in September 2011. Net retail loan assets under management stood at Rs 20,940 crore as on September 30, 2011.

Company has been expanding its business fast in a last few years, which is clear from the revenue growth recorded by the company. Thus to finance various activities such as lending and investments, company is raising money through issuance of Non-Convertible Debentures (NCDs). The proceeds may be used for repaying existing liabilities or may also be used for funding operational requirements of the business such as Capex and working capital requirement.

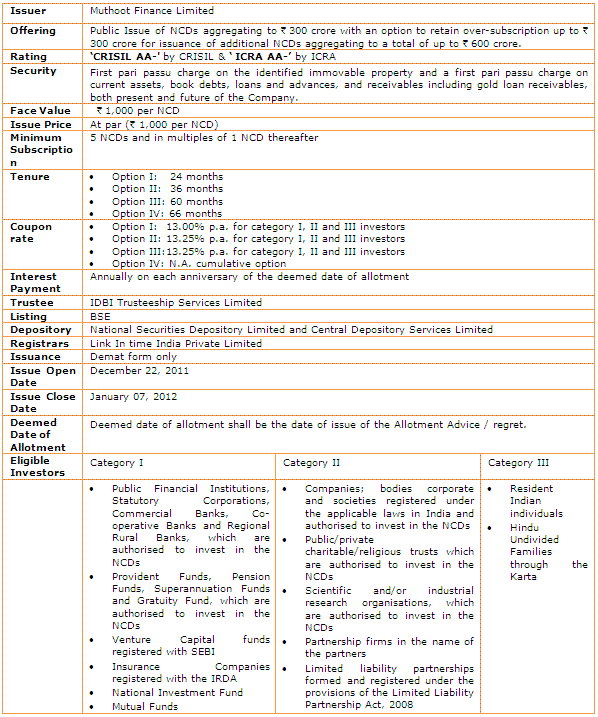

The details of the offering (NCD) are as follows:

Note: PAN card is mandatory for subscribing to these NCDs. A self attested copy shall be enclosed along with the application form.

Investors (across all categories) will also have the following options available at the time of subscribing to the issue:

(Source: Draft prospectus registered with SEBI. & PersonalFN Research)

Well, after reading the details of the NCD (as provided above), there may be still some more questions popping up, which are answered hereunder:

- Will I get any tax benefit if I invest in these NCDs?

No, these NCDs do not entitle you to any tax benefit nor are these any "infrastructure bonds", which make you eligible for an additional tax deduction under section 80 CCF.

- Is interest on these NCDs Tax Free?

No, the interest on these NCDs is not tax free - it is chargeable to tax. The interest income will be taxed under "income from other sources", and will be brought to tax at the respective income tax rates you fall under. However no tax will be deducted at source as these NCDs are issued in demat form and are listed on the exchange.

- What is the Tax Treatment on Capital Gains for these NCDs?

If you happen to sell these NCDs before 365 days, you will have to pay short term capital gain tax (@ applicable to you as per your tax slab) arising on the profit. Provisions of long term capital gain tax will be applicable for any sale of securities after 365 days. Any long term capital gain on these securities will be taxable @ 10% without indexation benefits or 20% with indexation benefits.

- Can a minor apply to these NCDs?

Yes, a minor can apply for these NCDs, but only and only through a guardian.

- Can one apply in joint names?

Yes, one may apply in a joint name. However, the demat account will also be required to be held in joint name and the order of applicant shall be the same as appearing in the demat account. Moreover, all payments will be made out in favour of the first applicant as well as all communications will be addressed to the first named applicant whose name appears in the application form and at the address mentioned therein.

- Who will get the interest in case of joint application?

In case of joint application, interest will be accounted to the first holder only.

- My demat account is in joint name, but I want to apply is a single name?

In case of a single application, demat account of the same single applicant would be necessary. Joint demat account would not do.

- If I’m an NRI can I invest in these NCDs?

No, NRIs are not eligible to invest in these NCDs.

- Is there a lock-in period while investing?

No. There is no lock-in period for these NCDs. In terms of providing liquidity, these NCDs are proposed to be listed on the National Stock Exchange and the Bombay Stock Exchange.

- In whose favour the cheque is to be made?

Cheques/Drafts have to be made in the favour of "Escrow Account Muthoot Finance NCD- Public Issue" and crossed "A/C PAYEE ONLY" "

OUR VIEW:

In our opinion the yields on investment offered by MFL are attractive. The credit rating too, allotted to the issue is stable (‘CRISIL AA-/Stable’ by CRISIL and ‘ICRA AA-/Stable’ by ICRA). Minimum ticket size has purposefully been kept low at Rs 5,000 to encourage the retail participation. Capital adequacy ratio also looks robust at 18.24% (against the 15% prescribed by RBI). Net NPA (Net Non-Performing Assets) constituted 0.58% (a little above from the March 31, 2011 figure, 0.33%) of the total loan book as on September 30, 2011, which is fairly low. Lower the net NPA better it is for the health of the company. Moreover, lower NPA ratio indicates that the company has been cautious to the quality of loans.

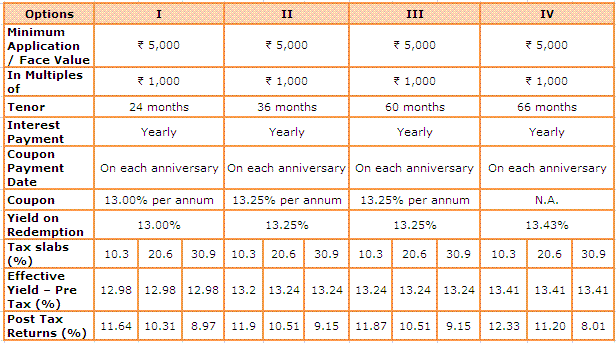

Thus taking into consideration a holistic view, we believe that investors who wish to earn regular income through interest payments may opt for option II and those investors who wish to receive lump-sum amount instead of regular interest payments may go in for the option IV.

In case you wish to invest in the above instrument, you can email us at info@personalfn.com or contact us on 022-6136 1200

Disclaimer: This note / article is for information purposes and Quantum Information Services Limited (PersonalFN) is not providing any professional / investment advice through it. The recommendation service, views, articles and other contents are provided on an "As Is" basis by PersonalFN. The facts mentioned in the note are believed to be true and from a public source. The Service should not be construed to be an advertisement for solicitation for buying or selling of any scheme / financial product. PersonalFN disclaims warrants of any kind, whether express or implied, as to any matter/content contained in this note, including without limitation the implied warranties of merchantability and fitness for a particular purpose. PersonalFN and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be responsible for any direct/indirect loss or liability incurred by the user as a consequence of his or any other person on his behalf taking any investment decisions based on the contents of this note. Use of this note is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. PersonalFN does not warrant completeness or accuracy of any information published in this note. All intellectual property rights emerging from this note are and shall remain with PersonalFN. This note is for your personal use and you shall not resell, copy, or redistribute this note, or use it for any commercial purpose. Please read the terms of use.

Add Comments

| Comments |

csChaitanya@yahoo.com

Dec 26, 2011

Nice one, I esp. like the 2nd table with thorough analysis. But I wish this was written/published last week, before NCD opened to public because such offers get subscribed in first few days and may close by the time we read this post and decide to subscribe for it.

In future, I expect you guys to publish such excellent articles atleast few days before the issue opening date. Many other sites are doing the same already, but I value your opinion more than anyone else's, so I wish to see your views before the issue opens, so that we've time to plan for such offers after reading your opinion. |

docgaurav@gmail.com

Dec 27, 2011

My concern regarding the above recommendation stems from a "conflict of interest" situation.

If you are highlighting the end of the article and asking us to call you for buying your recommendation, I believe that this is quite inappropriate, and would put reasonable doubt in the mind of any rational person.

Perhaps you should not do both the things,i.e., recommend and sell a product, since that is how we trust personal fn. |

vb_naveen2001@yahoo.com

Dec 30, 2011

Why muhtoot going for just NCD of 3% of thier current AUM or 30% of annual Income??

THanks |

lathamspottery@emarqmail.com

Jan 20, 2012

That's way the best est answer so far! |

1