(Image source: Image by F1 Digitals from Pixabay)

(Image source: Image by F1 Digitals from Pixabay)

In this fast-paced life, most people (millennials) are chasing the "retire rich and early" dream. They live by the adage, "Every penny saved is a penny earned". Hence, they are head-on with frugal spending, higher savings, careful planning, and wise investing for their blissful future.

[Read: Are You Thinking About Joining The FIRE Movement?]

Thus, they decide to invest any surplus cash in some investment product (mutual fund, plain equities, bank FDs, Small saving schemes, gold, etc.) without considering asset allocation.

What is asset allocation?

Asset allocation is an investment strategy that helps you optimise the returns on your investments. When you do an asset allocation exercise, you will understand the various investment risk levels associated with each suitable investment avenue as against the investment returns you want. This is because asset allocation helps you balance your returns with acceptable investment risks.

Since each person is different, has different life goals, wants, needs, and risk profiles the asset allocation strategy should differ. A personalised asset allocation strategy is based on a financial plan that takes into account your financial goals, financial positioning, risk appetite, and the investment time horizon of each financial goal.

Successful investors build a robust investment portfolio of mutual fund schemes that generates adequate returns despite market volatility with intelligent asset allocation. The reason being mutual funds:

-

Provide a level of diversification that allows you to invest across various investment instruments and investment styles.

-

Balance out the risk and provides better inflation-adjusted returns, hence mutual fund portfolio can be customised to suit any type of risk profile- aggressive, moderate, and conservative.

-

Are professionally managed by an experienced person.

-

Allow minimum investment amount via SIP.

-

Accelerates wealth accumulation if done sensibly.

As mentioned earlier, mutual funds allow you to have a fair diversification across asset classes that do not have a direct or positive correlation to each other.

Basically, a healthy portfolio takes exposure to any/all asset class which does not gain or lose at the same point of time. While different assets may have different moods based on the market fluctuations, a proper allocation across asset class and investment style may protect you from significant ups and downs of any single asset class and scheme in your portfolio.

Equities/equity funds are the most preferred when you have long term financial goals to achieve, but what about your day-to-day expenses or goals that are to be accomplished within a span of few months or years.

For this you require cash. Cash is the only asset class that will provide you with a return of principal in the short run. It is equally important to have some portion to hold in cash like your savings for retirement, a new house, or children's future (education and expenses) as well.

Why is it important to hold some portion in cash?

-

Cash in hand provides easy liquidity and allows you to meet your daily living expenditures & short-term goals. The advantage of having cash in hand is that you can spend it as per your wants to fulfil your gratifications. Despite the digitised payment systems, cash serves as the mode of currency exchange at various small retail stores, groceries, and for small purchase items.

-

Even to make down payments of some large items or to meet near-term planned and foreseen expenses you need instant cash.

-

Emergency situations or unforeseen events like accidents, wedding invitation from relative, loss of job, hospitalization, unexpected rise in your child's school fees, etc., can happen at any time and leave you high and dry. So, prepare yourself financially whereby you have a sense of security and strength to overcome those testing times.

[Read: Have You Built A Rainy Day Fund Wisely?]

-

Besides, when you are almost nearing your goal, your motive is to protect your capital, that time you can transfer it to cash or near-cash investment avenue for instant liquidation.

-

It even acts as a buffer or provides investment opportunities during market crashes. If you have cash, you can own an investment product at a reasonable price when it's available at a reasonable price. If you maintain a 'c(r)ash fund' and if an investment opportunity presents itself, you have the means to immediately invest. Else you would either be forced to sell shares or other investments, perhaps at a time when the market is down, or let go of the investment opportunity altogether.

When the time horizon on the goal is nearing, i.e. 3 years or less, the investment should be shifted to safer avenues such as bank accounts or fixed deposits, liquid funds, overnight funds, and floater funds.

So, here are a few avenues to park your money that will provide you with easy access to cash:

-

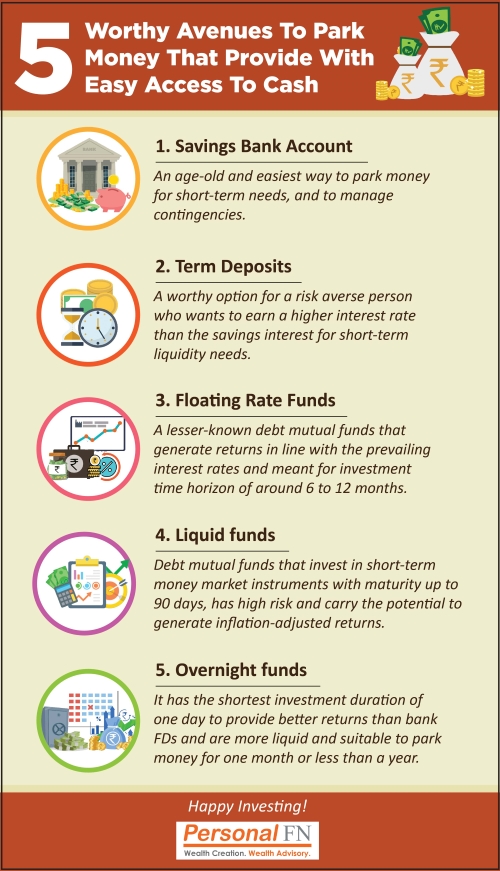

Savings Bank Account and Term Deposits

Well, this is an age-old and easiest way to park short-term needs, and even keep aside some money to manage contingencies. You'll earn around 4%-6% p.a. interest, depending on the bank you opt to park your savings.

But if you wish to battle inflation (which erodes the purchasing power of your hard-earned money) while managing your short-term liquidity, you may consider recurring deposits (RD), Fixed Deposit, a Sweep-in Account, or a Flexi/Recurring Deposit. The interest rates will be a few percentage points higher than the savings interest you earn.

-

Floating Rate Funds

It is one of the lesser-known debt funds that have a lower degree of sensitivity to changes in interest rates. As the rates payable on a floating rate instrument oscillates in line with the defined interest rate level, so these funds are less sensitive to duration risks

So, if interest rates go up, a floater fund will yield a higher level of returns. Hence, when the interest rates are expected to rise, choosing a floating rate fund is an attractive option for risk-averse investors.

They aim to generate returns in line with the prevailing interest rates and are suitable to hedge your corpus against interest rate risk.

While these funds carry a lower interest rate risk, they are meant for investments with a time horizon of around 6 to 12 months.

-

Liquid funds

Liquid funds are open-ended debt mutual funds that primarily invest in short-term money market instruments with maturity up to 90 days. Liquid funds invest in money market instruments such as Certificate of Deposits (CDs), Commercial Papers, Term Deposits, Call Money, Treasury Bills, and so on. Liquid Funds due to high liquidity are better than bank FDs as they carry the potential to generate inflation-adjusted returns. Also known as the real rate of return.

But a lot depends on selecting the best funds, as they do carry high risk given the market-linked nature of liquid funds, the return potential hinges on market conditions, and how efficiently the fund manager manages the portfolio. So, consider liquid funds only if you are open to taking credit risk to a certain extent. Otherwise, overnight funds can be an alternative.

[Read: The Best Liquid Funds For 2019]

-

Overnight funds

It has the shortest investment duration of one day and provides better returns than bank FDs and are more liquid. The interest rate risk involved therein is near zero. However, there can be a reinvestment risk, i.e. overnight funds may not be able to reinvest their proceeds at the same rate of return, but at least that doesn't cause any capital erosion.

Thus, it is suitable for conservative investors who want to park their money for one month or less than a year.

[Read: Liquid Funds v/s Overnight Funds: Where To Park Your Short-Term Money?]

But ensure you approach even short-term funds with your eyes wide open and paying attention to the portfolio characteristics and quality of the scheme. Prefer safety of principal over return. Stick to mutual funds where the fund manager doesn't chase returns by taking higher credit risk. Further, asses your risk appetite and investment time horizon while investing in debt funds.

While investing in short-term debt funds, consider keeping an investment horizon of at least 2-3 years.

Ideally, up to 50% of the emergency fund should remain highly-liquid by keeping it in a savings account or a mix of a savings account and liquid funds/overnight funds with an instant redemption facility. The remaining corpus can be invested over the other products relatively offering higher returns.

Watch this video to know more.

PS: If you are looking for high rewards with moderate risk, consider PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025(2019 Edition)".

With this you gain access to a ready-made portfolio of top recommended equity mutual funds for 2025 based on the core & satellite approach to investing.

If you haven't subscribed yet, do it now!

Add Comments