All You Need To Know About Equity Mutual Funds

Due to the massive gains over the past few years, the attractiveness of equity mutual funds has increased. There is no doubt that mutual fund investors are flooding the market. The quantum of growth in new investments becomes clear when looking at the increase in mutual fund folios over the past year.

Mutual Funds recorded an addition of 1.6 crore investor accounts in FY2017-18, taking the total tally to over 7 crore. This is more than double the addition of over 67 lakh folios in FY2016-17 and 59 lakh in FY2015-16. Retail investor accounts grew by over 1.5 crore to 5.94 crore during FY2017-18.

The Mutual Fund “Sahi Hai” catchphrase seems to have encouraged a new wave of investors. Apart from existing retail investors, there are new and inexperienced investors that are parking their money into mutual funds.

Are the new flocks of investors acquainted with the volatility in the market? Or will we see money flowing out as soon as the market goes through a correction? If left to their behavioural biases, we may see an exodus of funds from retail investors in the face of volatility.

If you are a newbie investor, don’t get lured by the performance of equity mutual funds over the past few years. Instead, invest in lines with your financial goals after drawing up a sound financial plan.

For those of you who are new world of mutual funds, there will be several questions that cross your mind – Questions ranging from something basic like what is a mutual fund and how does it work to something more complex like what are the risks involved in equity mutual funds.

Thus, PersonalFN has put together this guide to answer all questions, both basic and advanced on Equity Mutual Funds.

What is the meaning of Equity Mutual Funds in India?

Let’s first understand what is a mutual fund. A mutual fund scheme in India is a shared fund that pools money from multiple investors and invests the collected corpus in stocks, bonds, short-term money-market instruments, other securities or assets, or a combination of these investments. The investments are in accordance with the investment objectives as disclosed in offer document.

Likewise, an equity mutual fund scheme will invest predominantly in a set of stocks. Based on the investment objective of the scheme, the equity fund manager may invest the pooled assets in a category of stocks based on the market capitalisation or investment strategy of the fund. For example, the fund may adopt a Value style or dividend yield style of investing.

All mutual funds are required to be approved by the market regulator - the Securities and Exchange Board of India (SEBI) before it can collect funds from the public.

How do Equity Mutual Funds work?

Mutual funds issue units to the investors in accordance with quantum of money invested by them. Investors of mutual funds are known as unitholders.

The combined securities and assets the mutual fund owns is known as its portfolio, which is managed by a qualified investment professional also known as a fund manager. Each unit an investor holds represents a portion of the portfolio. The value of the units held fluctuates with respect to the underlying value of the portfolio. The value of each unit is represented by the Net Asset Value (NAV) of the fund.

The organisation that manages the investments is termed as the Asset Management Company (AMC). The AMC employs various employees in different roles who are responsible for servicing and managing investments.

The AMC offers various products (schemes/funds) in mutual funds, which are structured in a manner to benefit and suit the requirement of investors’. Every scheme has a portfolio statement, revenue account and balance sheet.

How is the Equity Mutual Fund NAV calculated?

In simple words, NAV or net asset value is the market value of the securities held by the Equity Mutual Fund scheme. Since market value of securities changes every day, NAV of the Equity Fund also varies on day-to-day basis. The NAV of the fund is used to judge its performance.

NAV is the current market value of all the fund’s holdings, minus liabilities, divided by the total

number of units. For example, if the market value of all securities held by a mutual fund scheme is

Rs 150 lakh and the mutual fund has issued 10 lakh units to the investors, then the NAV per unit of the fund is Rs 15 (i.e.100 lakh/10 lakh).

If an investor bought 1,000 units of the above fund at an NAV of Rs 10, his investment would now be worth Rs 15,000 (1000 units* Rs15 NAV). Or in other words, his mutual fund investment has grown by 50% (15000/10000-1)

NAV is required to be disclosed by the mutual funds on a daily basis.

What are the benefits of an Equity Mutual Fund?

Equity Mutual funds offer several important advantages.

-

Diversification

Investing in directly in stocks has one serious drawback - lack of diversification. If you plan to invest Rs 5,000 every month, you will not be able to buy many securities to add to your portfolio. Thus, you can subject yourself to considerable risk. With a concentrated portfolio, a decline in a single investment can have an adverse impact on your investments, damaging the returns of your portfolio.

An equity mutual fund, by investing in several stocks , tries to overcome the risk of investing in just 3-4 stocks. By holding say, 30 stocks or more, the fund avoids the danger of one bad stock spoiling the whole portfolio. Equity Funds own anywhere from a couple of dozen to more than a hundred securities, depending on the investment objective.

A diversified portfolio may thus fall to a lesser extent, even if a few stocks or investments fall dramatically. Also, a mutual fund's NAV may certainly drop with market forces, but mutual funds tend to not fall as freely or as easily as stocks or other individually traded market securities. The legal structure and stringent regulations that bind a mutual fund do a very good job of safeguarding investor interest.

-

Professional management

Active portfolio management requires not only sound investment sense, but also considerable time and skill. By investing in an equity mutual fund, you as an investor do not have to track the prospects and potential of the companies in the mutual fund portfolio. Skilled research professionals appointed by the mutual fund house continuously research and monitor a wide list of companies.

-

Lower entry level

There are very few quality stocks today that investors can buy with Rs 5,000 in hand. This is especially true when valuations are expensive. Sometimes, with as much as Rs 5,000 you can buy just a single stock. In the case of mutual funds, the minimum investment amount requirement is as low as ` 500. This is especially encouraging for investors who start small and at the same time take exposure to the fund’s portfolio of 20-30 stocks.

-

Economies of scale

By buying a handful of stocks, the stock investors lose out on economies of scale. This directly impacts the profitability of portfolio. If investors buy or sell actively, the impact on profitability would be that much higher. On the other hand, in case of mutual funds, frequent voluminous purchases/sales results in proportionately lower trading costs than individuals thus translating into significantly better investment performance.

-

Innovative plans/services for investors

By investing in the market directly, investors deprive themselves of various innovative plans offered by fund houses. For example, mutual funds offer automatic re-investment plans, systematic investment plans (SIPs), systematic withdrawal plans (SWPs), asset allocation plans, triggers etc., tools that enable you to efficiently manage your portfolio from a financial planning perspective too.

These features allow you to enter/exit funds, or switch from one fund to another, seamlessly - something that will probably never be possible in case of stocks.

-

Liquidity

A stock investor may not always find the liquidity in a stock to the extent they may want.

There could be days when the stock is hitting an upper/lower circuit, thus curtailing buying/selling. Further, if an investor is invested in a penny stock, he may find it difficult to get out of it.

On the other hand, mutual funds offer some much-required liquidity while investing. In case of an open-ended fund, you can buy/sell at that day's NAV by simply approaching the fund house directly, or by approaching your mutual fund distributor or even by transacting online.

As highlighted above, investing in mutual funds has some unique benefits that may not be available to stock investors. However by no means are we insinuating that mutual fund investing is the only way of clocking growth. This can also be done even by investing directly into the right stocks. However, mutual funds offer the investor a relatively safer and surer way of picking growth minus the hassle and stress that has become synonymous with stocks over the years.

On account of the aforementioned advantages which mutual funds offer, they (mutual funds) have emerged as immensely popular asset class, especially for retail investor, and for the investor looking for growth with lower risks.

What is a Diversified Equity Mutual Fund?

A diversified equity mutual fund invests over a variety of stocks and is not focused on a single sector or theme for investment. Due to this diversification, diversified equity funds tend to be less volatile than sector specific funds. Hence, diversified funds are a preferred route for majority of investors.

What are the types of Equity Mutual Fund schemes?

In 2018, mutual funds adopted SEBI’s Categorisation of mutual fund schemes. Thus under this regime, equity mutual funds have 10 different sub-categories.

In the table below, we have explained the characteristics of each category.

| Sub-categories (classes) |

Characteristics |

| Large cap Fund |

Minimum 80% investment in equity & equity related instruments of large cap companies. The scheme will invest predominantly in large cap stocks |

| Large & Midcap Fund |

Minimum 35% investment in equity & equity related instruments of large cap companies and simultaneously maintain minimum 35% allocation to mid cap stocks. The scheme will invest in both large cap and midcap stocks. |

| Midcap Fund |

Minimum 65% investment in equity & equity related instruments of mid cap companies. The scheme will invest predominantly in mid cap stocks. |

| Small cap Fund |

Minimum 65% investment in equity & equity related instruments of small cap companies. The scheme will invest predominantly in small cap stocks. |

| Multi cap Fund |

Minimum 65% investment in equity & equity related instruments. The scheme will invest across large cap, mid cap, small cap stocks. |

| Dividend Yield Fund |

The scheme should predominantly invest in dividend yielding stocks and hold a minimum 65% investment in equities. |

| Value/Contra Fund |

The scheme should follow a value / contrarian investment strategy and maintain minimum 65% investment in equity & equity related instruments. |

| Focused Fund |

The scheme will focus on the number of stocks (maximum 30), and invest a minimum 65% of its assets in equity & equity related instruments. |

| Sectoral/Thematic Fund |

The investment in equity & equity related instruments of a particular sector/particular theme should be minimum 80% of total assets. |

ELSS

(Equity Linked Savings Scheme) |

The scheme will invest minimum 80% of total assets in equity & equity related instruments (in accordance with Equity Linked Saving Scheme, 2005 notified by Ministry of Finance) and will carry a statutory lock in of 3 years and offer tax benefit under section 80C. |

Here’s how the market capitalisation categories are defined by SEBI to ensure uniformity in respect of the investment universe for equity mutual fund schemes:

-

Large caps: First 100 companies on full market capitalisation basis

-

Mid caps: All companies from 101st to 250th on full market capitalisation basis

-

Small caps: 251st company onwards on full market capitalisation basis

For this, mutual funds are supposed to adopt the list of stocks prepared by AMFI that classifies them as large caps, mid caps, or small caps.

As per the new categorisation norms, only one scheme per category is permitted, except:

-

Index Funds/ ETFs replicating/ tracking different indices;

-

Fund of Funds having different underlying schemes; and

-

Sectoral/ thematic funds investing in different sectors/ themes

It means offering two different schemes within the same category won't be permitted.

Moreover, a fund house can offer more than one scheme in the sectoral and thematic category, but more than a scheme within each sector/theme subcategory will not be allowed. For example, one can offer banking sector fund, FMCG fund, pharma fund, and so on.

However, offering two different schemes within the banking or pharma category won't be permitted. Same is the case with index funds, ETFs and Fund of Funds too, provided they meet prescribed conditions.

Dividend option or Growth option of Equity Mutual Funds?

With so many options such as dividend payout, dividend re-investment, growth and bonus, provided by mutual fund houses while investing in equity mutual fund schemes often leaves investors confused. Which is the most suitable option for you?

It is imperative that before you signify your choice of option, you are aware what they mean and how they function.

-

Dividend payout option – This option proposes to timely pay distributable surplus / profits to you in the form of dividends (either through cheques or ECS (Electronic Clearing Service) credits), thereby facilitating you to liquidate profits.

-

Dividend re-investment option – Under this option instead of paying dividend cheques or providing ECS credits, the dividend amount declared by a mutual fund scheme, goes in buying additional units of the same scheme (where you are invested), and you continue to book profits and keeps re-investing them in the same scheme.

-

Growth option – Under this option, you do not receive any dividends. Instead continue to enjoy compounded growth in value of your mutual fund scheme, subject to the investment bets taken by the fund manager.

-

Bonus option – Under bonus option you are not paid regular dividends. Instead you continue to receive bonus units in accordance to a ratio declared by the fund house. (very few mutual fund houses have this option)

Now as far as question of which is the correct option is concerned, it depends upon what your financial plan calls for. Your financial plan drawn by your planner should ideally be a function of your age, income, expenses, nearness to goals and risk appetite.

So say if you are young, your income is higher, your commitment towards certain expenses are lower, your willingness to take risk is high and you are many years away from your financial goals; then you may opt in for the growth option (while investing in mutual funds). And remember at a young age, since one generally doesn't look for a regular cash flow (as generally a regular income flows in the form of earnings), one should ideally opt in for the growth option.

However, despite the financial planning aspects stated and the regular income earned, if you are still looking for a cash flow (in the form of dividend) or want to book profits at regular intervals, then you may consider the dividend payout option while investing in mutual funds.

Please note: The dividends paid out by equity mutual funds are now taxable. Dividend Distribution tax of 10% will be deducted by the fund house from the dividend payout. Dividends of non-equity funds (such as debt funds & debt –oriented hybrid funds) attract a Dividend Distribution Tax (DDT) of 28.84%, which is deducted by the scheme.

Direct Plan or Regular Plan of Equity Mutual Funds?

Almost all mutual funds offer you broadly two plans to invest in their schemes, namely direct plans and regular plans.

Direct Plan — Opting for this plan while investing in mutual funds, you eliminate the services of a mutual fund distributor / agent / relationship manager. The transaction may be performed online or even physically by visiting the registrar’s or the asset management company’s office.

Regular Plan — This has been the conventional way wherein, you push your request to transact vide mutual fund distributor / agent / relationship manager.

Direct plans offered by mutual funds make a positive difference to your investments every year. The direct plans generate roughly 0.5% to 1.0% additional returns every year. However, if you sow seeds of these small savings, you may harvest rich rewards over 15- 20 years — thanks to the power of compounding.

There’s another benefit of investing through direct plans. You can easily avoid commission driven distributors and agents who often misguide you. You get a chance to do your research on available investment options.

But many investors find this job very tedious and time-consuming. If this has been your reason for not investing, it’s time you re-examine. Many platforms offer you ready tools to compare funds just at a click and control of the mouse.

Alternatively, you can always seek help of an independent mutual fund advisor who offers an unbiased research-based view for a fee, and you’re always free to invest in a direct plan. For your long-term financial wellbeing, it is essential that you review your portfolio so that corrective measures can be taken at the right time.

Mutual fund direct plans make a positive difference to your investments every year. These plans generate roughly 0.5% to 1.0% additional returns every year, thanks to lower costs. It may not seem much at first, but, if you sow seeds of these small savings, you may harvest rich rewards over 15- 20 years — thanks to the power of compounding.

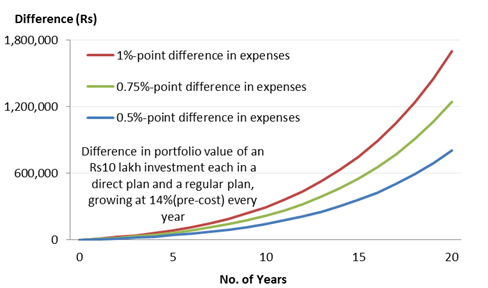

Save Huge Costs Over The Long Term

(Source: PersonalFN Research)

As can be seen in the chart above, a small difference in costs can result in savings of anywhere between Rs8-17 lakh over 20 years, on a Rs10 lakh investment. Yes, you can earn an additional amount of as much as Rs17 lakh, if the difference in costs is as much as 1% point. The final portfolio value varies with the magnitude difference in expenses. Every 0.25%-point difference in the expense ratio works out to an additional earning of Rs4.50 lakh in 20 years’ time, if Rs10 lakh is invested.

This Rs10 lakh investment is just as assumption. In reality, if you are saving for your long-term goals such as retirement, you will be targeting a corpus of over Rs1 crore for sure. Just imagine the costs then. Surely, you do not want to lose your hard-earned money in the form of costs that can be easily avoided. Moreover, the additional saving to such an extent can make huge difference to your financial goals.

So, if you are compromising on long-term returns by availing the services of so-called free robo-advisors, it’s high time to look for transparent alternatives before it’s too late.

If you are looking for the best mutual fund to invest in, then ‘FundSelect’ is something you should try right away.

Are Equity Mutual Funds risky?

Mutual fund schemes invest in a variety of securities and the risk depends on the underlying assets and securities it carries in its portfolio. As the market fluctuates, the value of stocks and bonds also move in a direction. This movement is reflected in the Net Asset Value (NAV) of a respective mutual fund scheme.

Your investments might generate returns as per your expectations, or it might not. This connotes the ‘risk’ involved. There are various factors that result into any kind of risk. Let’s take you through different important types of risk while investing in Equity Mutual Funds that you should be aware of. As follows:

-

Liquidity Risk

Liquidity risk arises when you are unable to sell your asset at a desired price at any given point. In other words, it arises when it is difficult to liquidate your assets/holdings. In such scenarios, fund managers are obliged to continue holding their position, and at times, it may even result in them selling these at much lower price that results in a loss.

-

Price Risk

This is especially pertinent to equity investing. Equity markets in short-term can be highly volatile. Noted economist, John Maynard Keynes has aptly articulated: “The market can remain irrational longer than you can remain solvent.”

Hence, it becomes vital to look at the price risk, because it can move in any direction. This price risk can affect the NAV of your fund, while volatility is integral to equity and equity related securities.

But when you invest in equity mutual fund schemes, invest for long-term, and so short-term volatility or price changes will not deter you. Having said, that, you ought to prudently select mutual fund schemes, and past performance should not be the only parameter to consider, as this trend may or may not continue. A holistic evaluation is necessary to select winning mutual fund schemes after considering a variety of facets.

-

Macroeconomic Risk

Besides the risk we discussed above, mutual funds, in general, are also exposed to macroeconomic risk. Macroeconomic factors such as growth, corporate earnings, inflation, interest rates, etc. do affect the overall value of the securities of a mutual fund scheme. So, when the economy at large is in good light, the positivity will also reflect upon the mutual fund schemes, and when it is not in good shape, that will have a bearing on the NAV too.

As mentioned before, you ought to select mutual fund schemes carefully for your investment portfolio, so as to leave you with only the winning mutual fund schemes for your portfolio. To distinguish the wheat from the chaff, carefully analyse the consistent performers.

What is an Equity Mutual Fund SIP?

Simply put, a SIP refers to Systematic Investment Plan, which is mode of investing in mutual funds in a systematic and regular manner. The method of investing is similar to your investment in a recurring deposit (RD) with a bank, where you deposit a fixed sum of money (into your recurring deposit account), but the only difference here is, your money is deployed in a mutual fund scheme (equity schemes and / or debt schemes) and not in a bank deposit, and hence your investments (in mutual funds) are subject to market risk.

Must read: All You Need To Know About SIPs

A SIP enforces a disciplined approach towards investing, and infuses regular saving habits that we all probably learnt during our childhood days when we used to maintain a piggy bank. Yes, those good old days where our parents provided us with some pocket money, which after expenditure we deposited in our piggy banks and at the end of particular tenure we saw that every penny saved became a large amount.

SIPs too work on the simple principle of investing regularly which enable you to build wealth over the long-term. In case of SIPs, on a specified date which can be on a daily basis, monthly basis, or on a quarterly basis, a fixed amount as desired by you, is debited from your bank account (either through a ECS mandate or through post-dated cheques forwarded) and invested in the scheme as selected by you for a specified tenure (months, years).

Today some Asset Management Companies (AMCs) / mutual fund houses / robo-advisory platforms also provide the ease and convenience of transacting online. They have set up their own online transaction platforms, where one can do SIP investments by following the procedure as made available on the websites.

So, you have fewer hassles while investing as well as tracking your investment dates.

Which are the best Equity Mutual Funds in India for 2018?

When market sentiments are high, investors often go scouting for the best equity mutual funds to invest in. However, one should not get lured by the double-digit returns generated over the past few years. Investors need to adopt a cautious approach.

Instead of chasing the best performing funds or the top performing funds, you need to take a step back and ensure to pick the right equity mutual, which is much more important for your financial well-being.

Invest as per your financial plan that's been drawn up after evaluating aspects such as your age, risk profile, financial health, investment horizon, financial goals and so on. It's better to have your investment right than timing it wrong.

If you have a financial plan in place, stick to it. If not, you should invest as per your risk profile below:

High Risk

You may be able to take on high risk, if you have age on your side, a steady source of income, and financial goals that are five years or more away. For such investment goals, you can invest in value funds, multi-cap funds, flexi-cap funds, and opportunities funds.

These categories of funds will provide an adequate mix of stability and growth. Value funds and multi-cap funds invest in a mix of mid-cap and large-cap stocks, while flexi-cap and opportunities style funds hold a mandate to invest across market capitalisation and sectors.

Even though mid- and small-cap funds are suitable for your profile, with valuations stretched, these funds pose a high downside risk. You should be cautious of the higher risk in these funds. But if you have long term goals that are over a decade way, you should consider these funds as a part of your portfolio.

Taking the SIP route enables you to average out your buying when markets drift down and compound your money when markets scale up. Choose funds with an established record of delivering superior risk-adjusted returns.

Additional reads:

Planning To Invest In The Best Multicap Funds In 2018? Think Again

Best Midcap Funds For 2018. Look Before You Leap!

What Is Value Investing And Why Invest In Value Funds

Moderate-to-High Risk

If you have a moderate-to-high risk profile and an investment horizon of over five years, opt for large-cap funds or balanced funds. In times of high market volatility and chances of a market correction, large-cap funds and balanced funds are better equipped to withstand a selloff.

If you are new to the world of equities, then you should get started with balanced funds (now to be renamed as Aggressive Hybrid Funds). About 65-70% of the assets are invested in equity, with the balance invested in debt. A combination of these asset classes offers a high level of diversification, hence, lowering the risk as compared to a pure equity fund.

For a newbie investor, such funds with a lower equity exposure can offer several benefits. You get the benefits of both worlds—equity and debt—in a single fund. Balanced funds have the potential to deliver inflation-beating returns, while keeping the risk in check.

Additional reads:

Are These Top Large Cap Mutual Funds Worth Your Investment in 2018?

Best Balanced Funds In 2017: Should You Invest?

Low Risk

If you have a low risk appetite and an investment horizon of less than five years, you may want to avoid equity-oriented funds altogether. You could find it difficult to deal with the high market volatility. However, in order to earn a decent return on your investment, consider debt funds. If you have an investment horizon of over three years, you can consider short-term funds or dynamic bond funds.

Considering bond yields are trending up with expectations of an interest rate hike, it is risky to invest in long-term debt funds now.

If volatility is not your friend or if you have an investment horizon of less than three years, then liquid funds or ultra-short term funds (liquid plus funds) will be an apt choice. These funds will earn you returns in the range of 6-7% (pre-tax) with extreme low volatility.

Do read: All You Wanted To Know about Liquid Funds Is Here

As the volatility in debt funds are low, the effect of rupee cost averaging through SIP is muted. Nonetheless, investing in debt funds through SIP will certainly keep your savings plan on track.

If you are unsure about which mutual fund schemes to invest in, try PersonalFN's unbiased mutual fund research services—Mutual Fund Research. Along with quantitative parameters such as performance, PersonalFN also considers qualitative parameters such as portfolio characteristics while analysing mutual fund schemes.

If you prefer doing your own research, download PersonalFN’s FREE Guide: 10 Steps to Select Winning Mutual Funds. The guide will help you select winning mutual funds and build a solid portfolio.

How to select the top Equity Mutual Funds for SIP?

How do you pick the best mutual funds for SIP?

Don’t worry, you are not alone. Every day hundreds of investors, like you, are seeking the ‘best sip plans’ or the ‘best mutual funds’ on Google.

After understanding the benefits of mutual funds, newbie investors look for the best mutual fund schemes. But, buying into a mutual fund without understanding how it fits into your whole financial future is a common newbie mistake.

Most websites that come up on the Google search engine usually provide a list of top mutual funds in India solely based on their past performance. Little do nascent investors know that tracking past performance can be misleading.

Even if you pick the best performing mutual fund, it may NOT always be the best mutual fund when invested though a Systematic Investment Plan (SIP).

Strange, isn’t it? But it’s a fact.

On analysing the performance data of equity diversified schemes, it has been found that the performance ranking differs when comparing the point-to-point performance and returns generated via a SIP in the fund. Read more about the analysis here - How To Pick The Best Mutual Funds For SIPs in 2018

The key lesson from the study is that irrespective of the fund’s point-to-point performance, the performance via a SIP will differ.

When investing via a SIP, you need to keep this in mind.

Therefore, instead of chasing performance or the scheme with the best returns over a period or multiple periods, you need to select the right mutual funds.

Because the best mutual fund today, may not be the best mutual fund tomorrow or the best mutual fund for a SIP.

You could however pick a top quality fund that has not only performed consistently in the past, but which has delivered strong returns via a SIP as well.

When picking mutual fund schemes, you need to analyse the risk-return parameters vis-a-vis other schemes and the quality of fund management. Not all mutual funds have the wherewithal to perform consistently under varied market conditions.

You need to analyse the historical data of returns from large cap funds across multiple periods and market cycles. Shortlist funds that have consistently outraced the market and their peers. Select the one that matches your risk profile and suitably meets your investment goals.

Well, no one has a magic crystal ball that can foretell which mutual fund schemes will top the list over the next decade. However, through years of experience, one can define a process that can be used to shortlist potentially the best mutual fund schemes for the future.

PersonalFN understands that not all investors are equipped with wherewithal to select the best mutual fund schemes for their portfolio. One would have to spend hours analysing mutual fund schemes in order to arrive at the right list for them. Thus, PersonalFN saves you the trouble and does all the tedious number-crunching work for you.

As mentioned in the article, SIP is only a method of investing in mutual funds. To support this investment method, you also need to pick the right mutual funds. PersonalFN offers a report titled "The Super Investment Portfolio – For SIP Investors."

After a rigorous shortlisting process, PersonalFN goes a step ahead when selecting funds that are SIP-worthy. Under this, PersonalFN conducts a detailed analysis on how SIPs in the top shortlisted funds have performed across multiple market conditions and timeframes. Only those funds that successfully pass this evaluation are suggested.

You can read more about the report and the subscription details here: The Super Investment Portfolio – For SIP Investors. Don’t miss out on special discounts. Subscribe Now!

Which are the best Equity Mutual Funds for long term?

By nature, all Equity Mutual Funds are meant for the long-term, which is defined as a holding period of 5-7 years or more. However, as explained a couple of questions above, you need to pick the right mutual fund rather than the best or top performing equity fund for your long-term goals.

At the same time, you may want to avoid taking exposure to sector funds or themed funds. This is the riskiest choice you can make. When you are betting on a particular sector, there is always exposure to a risk of a sudden reversal. About 4-5 years ago, the Pharmaceutical funds were offering fabulous returns; however, burdened by a whole host of issues, they have fallen out of flavour with large investors. As a result, individual investors who had invested in pharma funds are now sitting on glaring losses. So, invest in diversified equity funds instead.

Which are the top Equity Mutual Funds for tax-saving?

Under Section 80C of the Income Tax Act, you can claim a deduction of up to Rs 1.50 lakh. There is a wide range of investments that qualify for a deduction, such as, Public Provident Fund (PPF), 5-year Tax-saving Bank Fixed Deposit, Equity Linked Saving Schemes (ELSS) of mutual funds, National Savings Certificate (NSC), etc. You can claim an additional deduction of up to Rs 50,000, if you have invested in the National Pension Scheme (NPS).

Those who do not mind the high risk of equity investments prefer to invest in ELSSs among all the other tax-saving products. Due to the massive gains over the past few years, the attractiveness of equity mutual funds has increased.

Among the tax-saving products, ELSSs are the most liquid with the shortest lock-in period of three years. They are also among the riskiest. When investing in ELSSs, you should keep a long-term investment horizon of five years or more. By keeping a long-term investment horizon, you can benefit from compounding and multiply your wealth.

There is no dearth of choices in the ELSS mutual fund category. Hence, you need to analyse the fund performance minutely before investing. Remember, that under ELSS, the lock-in is three years. Thus, if you pick the wrong fund, you will have to bear the cost of underperformance for the entire period.

The performance of ELSS funds can vary wildly over the years. A top ELSS fund in one period may not necessarily be the best ELSS fund for the next period. Thus, you need to pick the right ELSS fund, one that has performed consistently and one that has generated a superior risk-adjusted performance.

When selecting ELSSs or any mutual fund for that matter, you need to choose wisely and look for consistency in performance. However, when it comes to ELSS, you need to pay attention to one more aspect. You also need to pay heed to tax planning. While there are a host of provisions under the Income Tax Act and numerous investment avenues. Also, the aspects you must consider while investing in them, so as to save tax through this investment instrument the prudent way.

While we acknowledge that, even the best systems and processes cannot predict the top ELSS funds of the future, as an investor, you need to pick the right and suitable ELSS funds to meet your financial goals.

If you are looking for the top ELSS funds, subscribe to PersonalFN's Exclusive Report - 3 Tax-Saving Mutual Funds For 2018.

In this report, you will find the Top 3 ELSS that are geared to grow your investment multi-fold over long term while saving your taxes. These Top 3 ELSS are handpicked through our special 7-point Selection Matrix methodology, and are considered to be potentially the best tax-saving mutual funds in the Indian market.

How to select the top Equity Mutual Funds in India?

You can pick potentially the best equity mutual funds by doing your own research. Here is what you need to consider:

Quantitative Parameters

- Performance and risk analysis

This is to analyse if the fund has shown consistency in performance across various market periods with decent risk-adjusted returns. Under this, the fund needs to be ranked on quantitative parameters like rolling returns across short-term and long-term periods such as 1-year, 3-years and 5-years, and on risk-reward ratios like Sharpe Ratio, Sortino Ratio and Standard Deviation over a 3-year period.

- Performance across market cycles

You need to ensure that the fund has the ability to perform consistently across multiple market cycles. Compare the performance of the schemes vis-à-vis their benchmark index across bull phases and bear market phases. A fund that performs well on both sides of the market should rank higher on the list.

Qualitative Parameters

- Portfolio Quality

Adequate Diversification - The scheme should not hold a highly concentrated portfolio. The portfolio should be well diversified and the exposure to the top 10 holdings should be ideally under 50%.

Credit Quality - For debt portfolios, you need to ensure that the fund does not hold a high proportion of low-rated (securities rated AA or below) or unrated debt instruments. A fund with a higher credit quality should be ranked higher.

Low Churn - Engaging in high churning can result in trading and high turnover cost. Therefore, you also need to consider the portfolio turnover ratio and expenses, and penalise funds involved in high churning, i.e. those funds with a turnover ratio of above 100%.

- Quality of Fund Management

You also need to consider the fund manager’s experience, his workload and consistency of the fund house. Therefore, you could check -

The fund manager’s work experience – He/she should have a decent experience in investment research and fund management, ideally over a decade.

The number of schemes managed – A fund manager usually manages multiple schemes. Thus, you need to check if the fund manager is not loaded with a large number of schemes. If he is managing more than five open-ended funds, it should raise a red flag.

The efficiency of the fund house in managing your money - You need to check if the fund house is consistent in performance across schemes or if only a few selected schemes are doing well. A fund house that performs well across the board is an indication of sound investment processes and risk management techniques in place.

Yes, we know that the above list is a lot for an average investor to look at. It involves a lot of number crunching and much of the data is not easily available at one place. But if you do need to narrow down on the top funds, these factors are of utmost importance.

Save yourself the time and energy that goes into fund selection, opt for PersonalFN’s Premium Mutual Fund Research service ‘FundSelect’

Every month, our FundSelect service will provide you with an insightful and practical guidance on equity funds and debt schemes – the ones to buy, hold or sell, thus assisting you in creating the ultimate portfolio that has the potential to beat the market.

Check out the exciting offers that can be availed on subscriptions to FundSelect here.

Go ahead and subscribe to PersonalFN’s FundSelect NOW!

Equity Mutual Funds Vs Equity Shares or Stocks – Which is a better?

Within the domain of investments, two options that investors regularly grapple with are stocks (i.e. direct equity investing) and mutual funds. Both have their advantages, although this note does not get in to that debate. Instead, in light of the present discussion about investing being a full-time activity, let's see how stocks and mutual funds face off against one another.

1. A matter of time

Investing directly in the stock markets is a full-time activity. It may sound like a one-time activity, but trust us, it isn't. There is research to be done pre-investment and pre-disinvestment. And research on a company does not just involve knowing its business. The investor is expected to master several subjects i.e. prospect of the sector, other companies operating in that sector and how the company (under review) is superior to them. The investor is also expected to study the economic and political climate of the country to gauge the bearing they can have on the sectors and companies in them. Having done this research before investing, the investor is expected to continue doing it even after he has invested in it so as to ensure he is invested in the right company/companies.

On a more serious note, if you believe that you can take out time from your work to invest directly in equities, then it is advisable to invest in proportion to your free time. Moreover, if you are busy today and expect to get even busier tomorrow, then re-consider whether you should be investing directly in equities at all. No point in starting something that you will unlikely finish.

Conversely, investing via the mutual funds route is far less time consuming. Sure, it might take a while to select the right mutual funds (your financial planner should be able to help you with that); however beyond that, a better part of the responsibility lies with the fund manager and your financial planner.

2. Investing skills

If you have the time to take up investing then you have cleared the first hurdle. There are other hurdles to be cleared like investment skills. A successful fund manager hasn't got where he has, only because he has the time to invest; he has something even more scarce the skill and knack of investing. And the skill sets to invest are not acquired overnight. Fund managers earn their stars over the years after going through several market trends and cycles (ups and downs) and after making several mistakes. So apart from the time factor, investing demands a lot of skill and experience.

3. Access to research

Most investors who wish to take up investing as a full-time activity are likely to hit a roadblock in getting unrestricted access to quality research. While conventional wisdom suggests that the annual report should prove sufficient in this regard, the bad news is that the annual report is just the starting point. For more information, you have to read up extensively on sectors and companies in those sectors. While some of this information could be available for free (in libraries or on the internet for instance), the quality inputs (read updated and insightful research) are usually available for a stiff fee.

Mutual fund managers on the other hand have no problem with these issues. For them, accessing research (regardless of the price) is never a problem. Meeting up with the company management and industry bigwigs is something they do on a regular basis. In fact, investment decisions are rarely taken without these inputs. On the other hand, the lay investor will often be compelled to take an investment decision devoid of these inputs. It is not surprising then, that there is usually a wide chasm between the quality of investments across both these categories (fund managers and lay investors).

While it may appear that we have done everything possible to discourage investors from investing directly in equities, the harsh reality is that investing directly in stock markets is easier said than done.

It's something that catches the fancy of every lay investor, but as we have seen, it's something that is beyond most of them. The solution to this problem is that investors delegate this responsibility to a competent money manager (fund manager) who is best placed to invest their monies in the best possible manner. The investor on his part can go about his own business, which is where his expertise and skill sets lie.

What is the tax implication of Equity Mutual Fund investments in India?

Capital gains on sale of equity mutual fund units are taxable like most other investment. Right until March 31, 2018, long-term capital gains arising out of sale of equity investments (held for 1 year or more) were exempt from tax. However, from May 1, 2018, investors would have to shell out a LTCG tax of 10% on the gains in excess of Rs 1 lakh.

Short-term Capital Gains arising out of sale of equity fund units held for less than a year, will attract a 15% tax. There has been no change in this tax treatment for equity funds. Hence, before buying and selling mutual funds, always consider and factor in the tax implications.

What is the Equity Mutual Fund taxation for NRIs?

NRI investors face the same tax implications as an individual investor. However, in the case of the former, tax is deducted at source by the fund house. Hence, for equity mutual funds, the Tax Deducted at Source (TDS) for NRI Investors is 15% for STCG and 10% for LTCG (exceeding Rs 1 lakh).

Are Equity Mutual Fund dividends taxable?

Earlier, mutual fund investors enjoyed tax-free dividends. However, from April 1, 2018 onwards, a dividend distribution tax of 10% is applicable on the dividends payable by the fund house. The total tax including 12% surcharge and 4% cess amounts to 11.648%. This tax is deducted by the fund house from the total dividends declared. Hence, unlike earlier, the NAV of the scheme will fall more than before to the extent of DDT paid.

How to buy or invest in Equity Mutual Funds?

Before you embark on the journey of investing in mutual funds, you need to complete your KYC (Know Your Customer) formalities. KYC is a prerequisite for investing in mutual funds (and almost all financial instruments). It is vital compliance on the part of financial product manufacturers, to know their investor better.

If you’ve opted for a regular plan, i.e. investing in mutual funds through a distributor, they will assist you with KYC compliances. However, if you plan to invest in mutual funds through the direct route, you can complete your C-KYC through five simple steps outlined here.

If you are investing in mutual funds through a distributor such as a bank or investment broker, they will assist you with the transaction forms and other required documentation. Some big distributors may offer online investment facilities to add to the convenience, while local distributors may offer purely offline services. The advice and service might be more personalised in the latter. Some may charge an additional fee for services offered, in addition to the commissions earned from your mutual fund investments.

If you would like to save on costs, it is best to opt for the direct route.

Investing through Mutual Fund Utilities gives you access to all the major mutual funds. Hence, if you are solely seeking a transaction portal, as of now, this is the best offering. There is no additional charge for mutual fund investments made through this portfolio. The cost of the platform is shared by the participating fund houses.

Investors should remain focused on their long-term financial goals and invest in the right mutual funds to fulfil these goals. The basics of investing in mutual fund schemes remain the same.

You may also invest through ‘PersonalFN Direct’, our proprietary and exclusive Robo Advisory platform. It is an online portal where you can carry on your investment endeavors in the most optimal way possible.

Backed by solid research experience of 15+ years, ‘PersonalFN Direct’ stands out against other Robo Advisory platforms run by commission driven fintech companies and startups.

All you need to do is answer a few basic questions to judge your risk appetite and you get instant access to the most optimum portfolio suitable for you.

So what are you waiting for?

Do away with the hassle of documentation and multiple form filling while investing in mutual funds. Just fill in your details, click and invest in the most optimum portfolio for you. Read more about the service here.

Author: PersonalFN Content & Research Team