|

| April 21, 2017 |

|

|

|

|

Impact

Are you sick and tired of the heavy-handed tactics of builders?

Don't worry!

From May 01, 2017 onwards, consumers will have more bargaining power.

These are the problems usually real estate buyers face…

- The deals are not transparent. Buyers are often charged as per the super-built-up area.

- Property buyers can't do much if there's a deficiency in the construction or in the amenities provided.

- Projects are often delayed. Consumers are not compensated when builders fail to keep deadlines, but if their payments are delayed, they are usually charged penalties.

- Funds are sometimes siphoned off and projects are permanently terminated. In such cases, recovering money from the builder becomes a herculean task for the individual home buyers.

The Rajya Sabha cleared the way for Real Estate Regulation and Development Act (RERA Act) in March 2016. The Government is now planning to implement it from May 01, 2017, after completing all formalities associated with the implementation of the law.

What will change for the developers and the real estate buyers?

- The developers are expected to maintain minimum 70% of the money collected from potential buyers in an escrow account opened with a bank, to be utilised exclusively to meet the cost of that project.

- Every project with the proposal of developing 8 flats or acquiring 500 square meters of the plot will have to be registered with the regulator. If the project is to be completed in phases, each phase needs to be registered separately. If the developer fails to do so, he will have to pay a penalty of upto 10% of the project cost, and if he /she becomes a habitual offender, he/she can be jailed for 3 years.

- Developers will have to sell flats on the basis of carpet-area. Selling apartments at built-up and super-built up rates is prohibited under RERA.

- The builder would be held responsible for structural defects in the first 5 years.

- If the project is delayed, the developer will have to pay the interest to the customer.

- The developer need permission from a minimum of 2/3rd of allottees to make changes to the original plan.

- Availing insurance for the land titles would become possible.

- Appellate Tribunals and Regulatory Authorities will have to dispose of complaints within a stipulated time period.

- Even property brokers will also have to register themselves under RERA. Furthermore, they can advise their clients only about registered projects. They shall operate only within the specified territory or state. If they are found violating any of these provisions, they can be penalised. In other words, brokers can't scuffle shrug off their responsibility and accountability towards their clients.

- Buyers will have to ensure that they take possession of property within 2 months of project receiving the Occupancy Certificate (OC)

Although RERA is a comprehensive law, implementation is the key. It fails to fix the accountability of the Government departments involved in sanctioning the projects. There is no provision of single-window clearance system for obtaining approvals. This might cause inconvenience to genuine developers.

If RERA is implemented effectively, real estate buyers can hope to become the King of their castle someday soon. But as prudent customers you need to be cautious while dealing with the real estate developers. So, your property search may start with identifying…

- Who is the builder?

- What has been his track record?

- Has he completed the construction of his projects as per schedule?

- Visit the site and inspect the quality of construction

- The rate which he is offering for the amenities offered

- You may also visit other sites developed by the same builder just to check whether he has fulfilled all promises made and offered amenities as promise

- Title of the property on which the construction is taking place or has taken place (to ensure that it free from any encumbrances and litigations)

- Has he obtained all statutory permissions

- In case of a ready property - i.e. newly constructed or a resale property, has a society being formed

- Is the builder listed or recognised by the housing finance company (in case if you want to avail a home loan facility)

Also keep a check on your affordability while you are exploring a property. One must assess the available options on some predetermined parameters given below, but shouldn't restrict to these…

- Locality

- Time lag for getting the possession (in case of on-going construction)

- Age of the property (in case of already constructed properties)

- Quality of Construction

- Maintenance cost

PersonalFN believes that if you are buying a house for dwelling, anytime might be a good time to invest (assuming you have assessed the affordability). But if you want to buy a house for the purpose of investment then you should take a holistic view of your portfolio. You must assess whether your current financial circumstances allow you to purchase property.

PersonalFN is of the view that investments should be made keeping your goals in mind. Real estate as an asset class is illiquid.

|

Impact

The boom in new client acquisition that some e-wallet companies experienced in the aftermath of demonetisation, is perhaps heading for an ugly ending, if their claims are to be taken seriously. Why so?

The RBI has released draft guidelines for the licensed issuers of Prepaid Payment Instrument (PPI) which include e-wallet companies.

E-wallet companies believe that when the master directions will be issued, compliance requirement will shoot up substantially, eventually spoiling their cost-arithmetic. Moreover, the general reaction of the industry players to the draft guidelines is that, if the rules are finalised as they are proposed, without modification, we might end up complicating the simple processes.

The industry players have expressed their concerns in an official feedback to the draft guidelines. A member of the industry delegation told media that, "Some clarifications were sought on certain clauses, while PPIs discussed issues around KYC, especially since it could be an overkill for small transactions."

What's going to change so much?

As you might be aware, at present, e-wallets allow you to transact with minimum Know Your Customer (KYC) requirements if your transaction value is upto Rs 20,000 per month. However, as per the draft guidelines, such e-wallet accounts should be made fully compliant with the KYC norms advised for the semi-closed PPIs, within a period of 60 days from the date of issue of PPI. If an e-wallet user fails to comply with the KYC requirements, he/she won't be able to use an e-wallet until he/she furnishes the necessary information.

E-wallet companies see this as a big loss of business since people might get discouraged from using e-wallet owing to burdensome compliance requirements for petty transactions.

An industry member speaking to the media on the condition of anonymity stated that, "In the feedback given to RBI, the main request is that minimum KYC be retained or that the deadline for implementing full KYC be extended to 18-24 months, since by then telecom companies would have done Aadhaar linking of mobile numbers. That will help mobile wallets do full KYC for all customers."

"The other ask is that RBI should publish the interoperability guidelines for wallets", he added.

Clearly, the Government, RBI, and the e-wallet companies are not on the same page. While the Government wants to encourage people to use digital modes of payment, the industry players are overtly dissatisfied with the RBI's draft rule and want a free run.

What's more startling is, how one-time compliance can affect cost-arithmetic of companies so much that, they are worried about losing business.

Even if we consider, initially the people might get discouraged to use e-wallets for their compliance requirements, how long will they be able to resist? E-wallet companies are showing the signs of desperation and this adds only to the claims of their critics who publicly expressed that their business models are unsustainable.

Lastly, the Government as well as the RBI are enthused to link Aadhaar to the financial transactions, both are strikingly silent about the data security of the e-wallet holders. This responsibility can't be entirely shifted to companies handling the business.

If India's dream for a digital revolution needs to take-off the ground, all the stakeholders will have to reconcile the differences and work on the common agenda.

|

Impact

It's happened all across the globe, not just in India…

Financial planners charged hefty fees and delivered little results. Investment advisers gave biased advice eyeing the high commissions. …

Investors with nominal capital face another difficulty.

As you would know, only a handful of advisers and financial planners are keen to offer them services.

Otherwise, acquiring "High-Net-worth Individual (HNI) clients" is the primary objective for advisers.

Would you like to know what their rationale behind this is?

"All clients irrespective whether they are HNIs or small investors, want top-quality services. As a result, servicing small investors becomes a loss-making proposition."

There might be some merit in this argument, but only to a certain extent.

It's often said that retail investors in India don't want to pay for service. This is a partial truth.

If somebody ever wondered why the average retail Indian investor has been depending on friends and relatives for investment advice, it's because professional advisers avoided him/her.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

The S&P BSE Sensex delivered a CAGR (Compounded Average Growth Rate) of 11.44% over the last five years (as on April 14, 2017), while the Nifty Midcap 100 Index, a CAGR of 18.23%. Those who had invested in equity mutual funds over this period made bountiful gains — are proud of their decision — and those who missed the bus, or weren't courageous to invest in equities are regretting it, and perhaps even envious of those who did.

In which category are you?

If you're one of those who missed the bus, here's another opportunity…

But, you need to START INVESTING REGULARLY RIGHT NOW!

PersonalFN acknowledges the fact that the Indian equity market is at its peak, and one should buy low and sell high, a basic tenet of investing.

However, we have a sound reasoning and method for our suggestion. Here's our viewpoint…

To read more about this story and Personal FN's views over it, please click here.

|

Impact

What did you do on May 09, 2016?

You might think it's a bizarre question.

But it is not…

Most of you who believe in buying gold only on auspicious days might have bought the precious yellow metal on May 09, 2016—on the propitious day of Akshaya Tritiya.

Has been it a profitable investment for you? Numbers suggest, no.

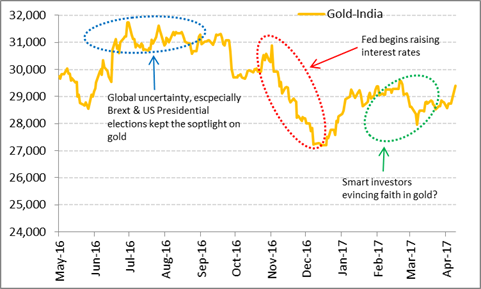

The last Akshaya Tritiya saw gold being quoted at Rs 29,750 per 10 grams. As on April 17, 2017, the precious yellow metal traded at 29,388 per 10 grams.

Tough time for the precious yellow metal…

Data as on April 17, 2017

(Source: ACE MF, PersonalFN Research)

As you can see in the graph above, gold had a tough time in the second-half of 2016, for a variety of reasons. During this period, gold prices fell lower than where it was on the day of Akshaya Tritiya.

There is nothing wrong with buying gold on Akshaya Tritiya. However, that's to be symbolic in nature. You can't make serious investments which will have long-term implications, just based on your faith and beliefs. Follow an agnostic's approach with your investments instead.

So before you invest in gold this Akshaya Tritiya, let's understand the factors that drive gold prices up or down.

To read more about this story and Personal FN's views over it, please click here. |

The Government has been lowering the administration rates on Small Savings Schemes (SSS) ever since it started reviewing them on quarterly basis. But the finance ministry seems to have gone overboard with the exercise.

It's trying to meddle in the decisions of the other ministries. For instance, the Central Board of Trustees (CBT) of the Employees' Provident Fund Organisation (EPFO) had recommended 8.65% rate for FY17. There were reports in the media suggesting finance ministry insisted that the labour ministry should cut interest rates by 50 basis points, at least, a basis point is one hundredth of a per cent.

Responding to that, Mr Bandaru Dattatreya briefed the media about the developments. He said, "It is not like that. The CBT had decided to give 8.65%.Our ministry keeps on discussing with Finance Ministry. We would have surplus of Rs 158 crore on providing 8.65%," Dattatreya said on being asked whether the Finance Ministry is making a case for lowering the interest rate.

He also added that, "I will talk to them (Finance Ministry). I have requested them to approve 8.65%. In any case this amount (interest income) will be given to workers. But how and when it will be provided, this is the question."

Mr Jaitley needs to understand that interest rates on EPF are already at a 7-year low. And, in absence of a social security system the finance ministry shouldn't go overboard with the discipline. If it has to, then how will it justify the farm loan waivers, although announced at the state levels?

|

SIPs Vs. EMIs: Which Is Better?

5 Ways to Ensure That Your Dream Vacation Won't Leave You Bankrupt

5 SIP Features That Every Mutual Fund Investor Should Know

|

Intrinsic Value: The intrinsic value is the actual value of a company or an asset based on an underlying perception of its true value including all aspects of the business, in terms of both tangible and intangible factors. This value may or may not be the same as the current market value. Additionally, intrinsic value is primarily used in options pricing to indicate the amount an option is in the money.

(Source: Investopedia)

|

|

|

|

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667

SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013

|