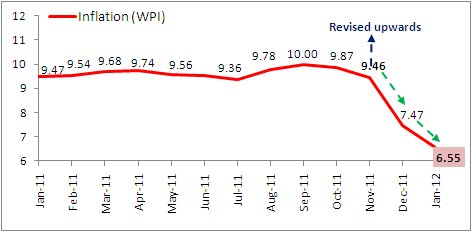

The Wholesale Price Index (WPI) inflation, after ending the month of December 2011 at 7.47% its lowest level in two years cools down further to 6.55% for the month of January 2012. Also, the inflation for the month of November 2011 was revised upwards at 9.46% from 9.11% earlier.

Further analysis reveals that the inflation is now on a cooling path wherein we may see the headline WPI inflation mellowing down further. Also, the food inflation being under the negative terrain may further give impetus to inflation cooling down (weekly food inflation data has been discontinued and instead there will be a monthly figure going forward). Moreover, if the winters are extended (possibly as forecasted by the meteorological department) there is a possibility of high food grain production (Kharif crops) which in turn may keep food inflation under check.

Inflation on a cooling path!

(Source: Office of the Economic Advisor, PersonalFN Research)

However, the crude oil price (Brent crude) which has been hovering over $117 per barrel may be a worrisome factor as rising crude oil prices may shoot up the import bill. Also, development taking place between Iran and the rest of the Developed nations will have to be closely monitored as any supply disruptions of crude oil from Iran may push the prices exponentially high.

So, would RBI go in for a rate cut in the upcoming monetary policy review?

We believe that until March 2012, it is unlikely that the RBI will go in for a rate cut soon. However, there could be a further cut in the CRR to ease the liquidity crunch in the banking system.

Policy Rate Tracker

|

Increase / (Decrease) since March 2010 |

At present |

| Repo Rate |

375 bps |

8.50% |

| Reverse Repo Rate |

425 bps |

7.50% |

| Cash Reserve Ratio |

50 bps |

5.50% |

| Statutory Liquidity Ratio |

(100 bps) |

24.00% |

| Bank Rate |

Unchanged |

6.00% |

(Source: RBI website, PersonalFN Research)

Our View on inflation:

We believe that the inflation numbers in the ensuing months may cool down further partly on account of the slowdown in the economy and partly due to the high base effect. However, if food inflation jumps back from the negative terrain to positive and if there are any supply disruptions in crude oil we may see the WPI inflation hardening. If things pan out positively, we expect WPI inflation to be in the range of 7.00% - 7.50% by March 2012.

What should equity investors do?

Equity investors should adopt calm and compose approach by staying invested and also investing further as, valuations in the Indian equity markets look fairly attractive and there is potential for robust future growth.

However, as fear of downbeat economic data being disseminated from the Euro zone still remains, staggering your investments would be an appropriate approach. We recommend that you invest in diversified equity funds as this will help reduce risk. However one should stay away from U.S. or Euro oriented offshore funds in such a scenario, and instead look at investing in domestic value style equity funds. Ideally you should opt for the SIP (Systematic Investment Plan) mode of investing as this will help you to manage the volatility of the equity markets well (through rupee-cost averaging) and also provide your investments with the power of compounding .

Remember, while investing select only those equity funds which follow strong investment processes and systems, and invest with a long-term horizon of at least 5 years.

What should debt investors do?

Well, we think that the current situation is attractive to take exposure to debt mutual fund instruments as interest rates are likely to consolidate at these higher levels before they start going down.

You can now gradually take exposure to pure income and short-term Government securities funds. Since longer tenor papers will become attractive, longer duration funds (preferably through dynamic bond / flexi-debt funds) can be also considered, if one has a longer investment horizon (of say 2 to 3 years). However, one may witness some volatility in the near term as there is always an interest rate risk associated with the longer maturity instruments.

With liquidity in the system being tight (ahead of advance tax payment obligation in mid-December), yield on the short term instruments are expected to move up slightly (say by 15 bps to 25 bps) thus making short term papers more attractive. Hence investors with a short-term time horizon (of less than 3 months) would be better-off investing in liquid funds for the next 1 month or liquid plus funds for next 3 to 6 months horizon. However, investors with a medium term investment horizon (of over 6 months), may allocate their investments to floating rate funds. Short term income funds should be held strictly with a 1 year time horizon.

Fixed Maturity Plans (FMPs) of 2 months to 1 year will yield appealing returns and can also be considered as an option to bank FDs only if you are willing to hold it till maturity, but you may not have a very attractive post tax benefit, as indexation benefit will not be available on FMPs maturing within 2 months. You should invest in longer duration funds, if the time horizon is of over 2 to 3 years. You can consider investing your money in Fixed Deposits (FDs). At present 1 yr. FDs are offering interest in the range of 7.25% - 9.40% p.a.

What should investors in gold do?

With the global economy being on an edge with the debt-overhang situation in the Euro zone, the risk of a contagion spreading still remains. This we think would make the precious yellow metal continue its northward journey, with sideways movement as well, if some intermediate positive news is disseminated from the Euro zone. Moreover, as long as WPI inflation continues to remains stubborn we think that smart investors would prefer to take refuge under the precious yellow metal, thus hedging themselves against volatility of equity markets.

Hence, nothing has changed for gold and we believe it will continue to maintain its upward trend in the long-term.

Add Comments

| Comments |

ctanada@i-manila.com.ph

Feb 25, 2012

Hiya. Very cool site!! Man .. Beautiful .. Amazing .. I'll bookmark your blog and take the feeds additionally I'm happy to locate a lot of helpful info right here in the post. Thanks for sharing.. |

boeker@dwi.rwth-aachen.de

Oct 15, 2013

Thank you for your site post. Manley and I have already been sanivg to buy a new e-book on this topic and your post has made us all to save all of our money. Your notions really clarified all our concerns. In fact, in excess of what we had known in advance of the time we discovered your great blog. I actually no longer nurture doubts and also a troubled mind because you have actually attended to our needs above. Thanks |

1