The effects of demonetisation on consumer demand seem to have remarkably faded in February 2017.

Retail inflation, measured by the movement of Consumer Price Index (CPI), increased from 3.17% in January to 3.65% in February. Food inflation jumped from 0.61% in January to 2.01% in February.

It’s noteworthy that the core (non-food, non-energy) inflation quickened at a faster pace vis-à-vis CPI inflation.

What drove core inflation?

- Clothing and Footwear: 4.38%

- Housing: 4.90%

- Miscellaneous (includes personal care, healthcare, education, household goods and services and transportation): 4.79%

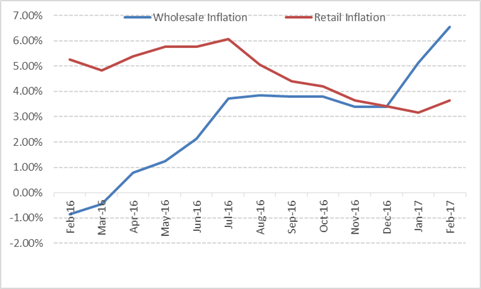

Interestingly, the Wholesale Price Index (WPI) too, an indicator of the industrial inflation, accelerated at a much faster pace in February. The WPI inflation for February came in at 6.55% (39-month high on cost of fuel and food items) vs. 5.22% in the previous month.

CPI Vs. WPI

(Source: MOSPI, PersonalFN Research)

The divergence between industrial inflation and the retail inflation can be attributed to several factors which include:

- The difference in the base year for both indices—CPI uses 2012 as the base year, while WPI is calculated using 2004-05 as the base year.

- Weights of the various items in CPI and WPI are different—for example, food articles account for a little over 14% in WPI, while constituting over 54% of CPI.

- A massive increase of 21.02% in fuel and power cost at the wholesale level and the lower base effect drove WPI higher.

- On the other hand, the impact of higher base effect on CPI has begun to wane.

So, what do these inflationary trends suggest?

Well, primarily two things:

- Higher WPI and comparatively lower CPI would indicate that the retailers’ profits are under pressure.

- Likewise increase in input cost for manufacturing activities, and revival of capex cycle in the private sector may also drive the WPI upwards.

Impact on policy decisions

Going by the recent trends in inflation, it seems the RBI’s assessment of the inflationary trends was right.

As far as the monetary policy is concerned, RBI uses retail inflation as the benchmark to determine the policy stance and direction. At the

sixth and final bi-monthly monetary policy review for 2016-17, it surprised trackers of the policy action by moving its monetary policy stance from ‘accommodative’ to ‘neutral’. It also held rates unchanged at 6.25%.

What led RBI to shift its policy stance from accommodative to neutral?

- Global recovery has been driving the inflation expectations up globally, mainly on account of rising energy prices

- Anticipated exchange rate volatility, owing to global uncertainties

- Sticky nature of core (non-food, non-energy) retail inflation back home

Although the future movement would depend on a variety of global and domestic factors, what looks almost certain is, RBI is unlikely to lower policy rates in a hurry.

At the sixth bi-monthly monetary policy for 2016-17, RBI had stated that surplus liquidity in the system on account of demonetisation may spur the policy transmission. In other words, it is unlikely to reduce policy rates further until banks pass on the full benefits of all previous rate cuts to the borrowers.

What to expect?

Going by the present trends, if the global growth picks up, fuel, and commodity prices might may rise. Higher commodity prices (especially the crude oil prices) would work negatively for India, since it’s one of the largest importers.

But thankfully, the Indian Rupee (INR) has been demonstrating unusual strength against the US dollar (US$). And After

BJP’s landslide victory in the Uttar Pradesh elections, INR has strengthened even more, recently touched a 16-month high, despite the constant buying of US$ by RBI.

This suggests that INR is one of the strongest emerging-market currencies. If it continues to outperform its global peers, the impact of rising global commodity prices might get negated.

But it remains to be seen how RBI interprets these developments. It might also take cognizance of the divergence between CPI and WPI numbers for making policy decisions more inclusive and effective.

Also, it may await more structural reforms from the Government for changing its policy stance. The Government is expected to find a formidable solution to the problem of poor asset quality of banks.

A message for investors in debt markets…

If you are investing in debt markets, please note that with change in the RBI’s monetary policy stance from ‘accommodative’ to ‘neutral’ and the inflation trajectory; it appears that there may not be any rate cuts in the ensuing fiscal year 2017-18.

On hopes of rate cut, most of the rally has already been captured on the longer-end of the yield curve. Expecting yields to drop would be mindless. In fact, since the day of the sixth bi-monthly monetary policy 2016-17, the 10-yr 7.59% 2026 G-Sec benchmark yield has inched-up by 15 bps until March 14, 2017, and since the start of January 2017, by 46 bps.

Therefore, it would be imprudent to take exposure at the longer end of the yield curve. Yet, if you hold a high risk appetite and have a long time horizon (of at least 3 years), not more than 20% of your entire

debt portfolio may be allocated to long-term debt funds via dynamic bond funds (as they are enabled by their investment mandate to take positions across maturity profile of debt papers).

In case you have a time horizon of less than a year and the risk profile doesn’t permit it, stay away from funds with longer maturities.

If you have a short-term investment horizon of 3 to 6 months, you could consider investing in ultra-short term funds (also known as liquid plus funds). And if you have an extremely short-term time horizon (of less than 3 months), you would be better-off investing in

liquid funds. Remember that investing in debt funds is not risk-free.

A message for investors in equity markets…

PersonalFN discourages its readers and investors from speculating on the direction of interest rates, when investing in equity markets.

When you select equity funds, be careful. Prefer those

mutual fund schemes that follow strong investment processes and systems as against those indulging in momentum playing.

A staggered approach amid times when valuations appear pricey would be prudent. Prefer the Systematic Investment Plan (SIPs) and / or Systematic Transfer Plan (STP) mode of investing. This will help you to mitigate the risk better, while you endeavour to achieve your financial goals.

Besides, invest as per your personalised financial plan. In case you haven’t prepared one, don’t hesitate to opt for services of a

Certified Financial Guardian, who can handhold in your journey of wealth creation.

Happy Investing!

Add Comments