Sure the traditional approach of parking surplus money in the short-term is in a Savings Bank Account and/or Bank Fixed Deposits. But did you know that Liquid Funds can offer reasonably better returns than a savings account as well as better liquidity and complete flexibility with the investment timeline compared to fixed deposits?

In fact, as the name suggests, you can expect Liquid funds to offer you the liquidity at low risk whenever a need arises. Fund managers of liquid funds prioritize preservation of capital over maximizing returns. With Liquid Funds your surplus money could earn reasonable returns over the short-term and have access to it whenever you need.

Image source - www.freepik.com

Image source - www.freepik.com

What are Liquid funds?

Liquid funds are debt mutual funds that invest in debt and money market instruments such as Certificate of Deposits (CDs), Commercial Papers (CPs), Term Deposits, Call Money, Treasury Bills and so on, with a maturity of up to 91 days. They are perceived to be among the safest in the debt funds category.

So if you are looking to park your surplus money for the short-term, to build a contingency fund, to address short-term goals, and/or to tactically shift money into an equity fund (via the Systematic Transfer Plan) to offset volatility, Liquid funds can be a worthwhile option.

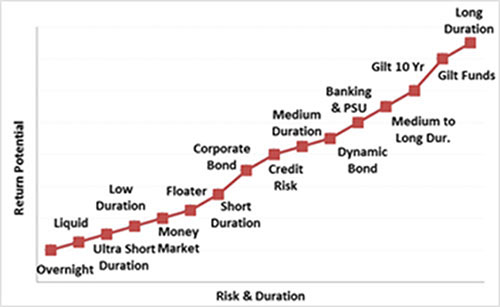

Graph: How is a Liquid Fund placed on the Risk-Return spectrum?

For illustration purpose only

For illustration purpose only

The primary objective of a Liquid Fund is to provide optimal returns with a low level of risk and high liquidity through judicious investments in money market and debt instruments. This means a Liquid Fund entails low risk; it is placed at the lower end of the risk-return spectrum vis-a-vis other debt mutual funds as depicted by the graph above.

A Liquid Fund should ideally follow the spirit of the product. The portfolio of a Liquid Fund should be constructed in a way that ensures the investors' hard-earned money is prudently parked in safe and liquid instruments, whereby it can earn a slightly higher return than the interest on a savings bank account (just not extraordinary returns).

Table: Performance scorecard of Liquid Funds

Data as on March 18, 2021

(Source: ACE MF)

*Please note, this table only represents the best performing Liquid Funds based solely on past returns and is NOT a recommendation. Mutual Fund investments are subject to market risks. Read all scheme related documents carefully. Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

So when you invest in a liquid fund, remember that returns are secondary. The main objective is to keep your hard-earned money secure but highly liquid. In the past, there have been instances where the NAV of some liquid funds have taken a hit when the underlying securities were suddenly downgraded.

Since the holding period of such funds is low, a significant write-off of a particular asset in the portfolio means that investors have to hold on to their fund longer than expected to recover from losses. Thus, evaluating the quality of portfolio is of utmost importance to mitigate any credit risk.

As an investor, you should ask these crucial questions to ensure that you invest in a pure liquid fund:

-

✓ Is the quality of the securities held in the portfolio reliable?

-

✓ How reliable are the ratings assigned?

-

✓ What if the rating assigned to particular debt paper slips; does the fund house have adequate risk management measures in place in such a case?

-

✓ Does the fund manager compromise on the 'liquidity' aspects?

When you select a pure liquid fund, ensure that it prioritises safety and liquidity over chasing returns. Take the time to thoroughly assess the fund's portfolio. A fund may have delivered higher returns compared to its peers, but determine whether it was driven by a smart portfolio strategy, or was it because the fund manager chased higher yields by taking higher credit risk?

Best liquid funds to invest in 2021:

Some of the best liquid funds based on our analysis and research at PersonalFN are:

- Canara Robeco Liquid Fund

- Motilal Oswal Liquid Fund

- Parag Parikh Liquid Fund

- Quantum Liquid Fund

- Edelweiss Liquid Fund

Do not fall for liquid funds that have higher allocation to moderate rated instruments or those investing predominantly in instruments issued by Private issuers. If your preference is safety over returns, you should consider funds primarily focusing on Government and Quasi-government securities.

In addition, ensure that the portfolio is well diversified across a range of securities and that it is not concentrated towards a certain company or group of companies.

Most importantly, always give higher importance to fund houses that follow robust investment processes and systems along with sound risk management techniques in place. It is crucial that you understand the overall philosophy of the fund house; whether they aim to create wealth for investors, or are they in a race to garner more AUM by showcasing higher returns generated from chasing higher yields and taking higher risk.

Watch this short video on the lessons an investor can remember while investing in Debt Mutual Funds.

Outlook for Liquid Funds in 2021

The Union Budget 2021 focused on pro-growth measures and making structural reforms to get the economy back on track. It provided an extensive spending plan on long-term projects including infrastructure, capex, and healthcare, which comes at a cost of higher fiscal deficit. The government has also announced a higher borrowing programme at Rs 12.05 trillion for FY 2021-22.

The higher borrowing target for the next fiscal year is expected to push bond yields higher. As you may be aware, bond prices and yields are inversely related. A surge in yield will impact bond prices negatively, which leads to a loss in the investors' value.

Moreover, the RBI has reduced repo rate by 115 bps and reverse repo rate by 155 bps during the pandemic. The fall in yields to a multi-year low had led to a rally in bond prices; however, with yields at an all-time low, the return expectation on debt funds has diminished.

The longer duration instruments are more sensitive to interest rate changes as compared to shorter duration instruments. Remember that Debt funds with exposure to medium to longer duration instruments tend to be more volatile in a scenario where there is an upwards movement in interest rates.

Debt funds that have exposure to longer maturity instruments may be highly volatile going forward, while those focusing on shorter maturity instruments (such as liquid fund) and following an accrual strategy may still be better-placed to tackle the interest rate risk.

Therefore, in the present scenario, you would be better off investing in pure liquid funds that do not have high exposure to private issuers.

PS: If you are looking for quality mutual fund schemes, I recommend subscribing to PersonalFN's premium research service, FundSelect. Currently, with your subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect. Read full details here...

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds