Liquid funds, on the other hand, generate 200 to 300 basis points higher returns than what your savings bank account fetches you. A basis point is a hundredth of a per cent.

You can withdraw within a month. In other words, liquid funds offer you almost the same liquidity as your savings bank account does, but help you generate better returns.

(Image Source: Business photo created by freepik)

(Image Source: Business photo created by freepik)

What are Liquid Funds?

According to SEBI categorization and rationalization norms, Liquid Funds are mutual fund schemes investing in debt and money market securities with a maturity of upto 91 days.

They invest in money market instruments such as Certificate of Deposits (CDs), Commercial Papers, Term Deposits, Call Money, Treasury Bills, and so on. They are highly liquid in nature and entail low risk.

The primary objective of a Liquid Fund is to provide optimal returns with low-to-moderate levels of risk and high liquidity through judicious investments in money market and debt instruments.

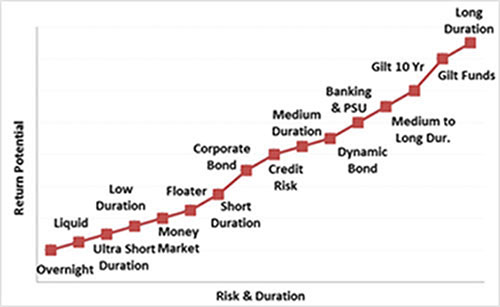

Graph: Risk-return spectrum of debt mutual funds

Note: Illustrative purpose only

Note: Illustrative purpose only

(Source: PersonalFN Research)

On the risk-return spectrum, a Liquid Fund is placed at the lower end (almost at the bottom) when compared to other debt mutual funds.

Do not assume a Liquid Fund to be absolutely risk-free. The risk perception about Liquid Fund changed in 2018 after certain corporates defaulted on their short-term debt obligations.

Liquid Funds were perceived to be 'safest' until the great debacle of IL& FS happened followed by more defaults. Few liquid funds had to be marked down as their investments in these companies owing to sudden credit rating downgrades took a hit.

[Read: How IL&FS Rating Downgrade Will Impact Your Mutual Funds...]

That being said, remember, Liquid funds aren't risk-free.

Fund houses and distributors aggressively promoted debt funds as an alternative to fixed deposits and other fixed income products. Unfortunately, they had failed to highlight the risk involved and investors learned this the hard way. The negative returns Liquid Funds clocked after the IL&FS case came as a shocker to debt mutual fund investors.

So, while Liquid Funds are an effective medium to park your short-term needs, it is essential to recognize how Liquid Funds work, and their risk-return traits.

Liquid Funds can make you jittery if the fund manager:

-

Chases yields without proper risk control measures in place

-

Depends excessively on credit ratings assigned by external rating agencies

-

Understates the role of liquidity management practices adopted by the borrower

-

Fails to gauge the changes in the systemic liquidity conditions

[Read: Is Your Investment In Debt Mutual Fund At Risk?]

Who should consider Liquid Funds?

While the returns on liquid funds are generally not as high as income funds, they do seek to provide some level of stability, and can, therefore, play an important role in your portfolio. Investors can use liquid funds to offset the typically greater volatility of bond and equity investments.

A Liquid Fund is a worthy investment avenue for...

-

✓ Individuals with a very low-risk appetite (for whom the safety of money is the primary objective and not high returns);

-

✓ Who wish to address short-term financial goals;

-

✓ Diversification purpose with an investment time horizon that is less than 3 months to a year;

-

✓ Individuals who intended to park money for contingency needs; and/or

-

✓ Tactically shifting money from an equity fund (via the Systematic Transfer Plan) to offset volatility

-

✓ A temporary holding place for assets while waiting for other investment opportunities to arise

Further, the quick redemption policy makes it an even more favourable option to address liquidity needs.

Performance of Liquid funds across various timeframes

Liquid Funds generated 6.32% returns in calendar 2019 and 4.74% returns for the ongoing FY 2019-2020.

Table: Performance of top 12 schemes.

Data as on February 25, 2020

(Source: ACE MF)

*Please note, this table only represents the best performing Liquid Funds based solely on past returns and is NOT a recommendation.

Mutual Fund investments are subject to market risks. Read all scheme related documents carefully.

Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

From the table above one can see in the calendar year 2019, Quant Liquid Plan and Franklin India Liquid Fund-Super Inst have managed to outperform the benchmark index. Whereas for a longer time frame of 2 and 3 years, all of the above schemes have beaten the benchmark and the category average returns.

And have shown superior performance and consistency on all parameters--quantitative as well as qualitative.

[Read: Why Qualitative Aspects Are So Important To Pick Mutual Funds]

When you select the best Liquid Funds, avoid schemes that haven't completed a 1-year track record in the interest of your investment portfolio.

How to select the best Liquid Fund?

When you choose a Liquid Fund to address your short-term needs/financial goals and/or for contingency needs, always pay careful attention to its portfolio characteristics to evaluate:

-

✓ Whether the quality of the securities held in the portfolio are reliable

-

✓ How reliable are the ratings assigned?

-

✓ What if the rating assigned to particular debt paper slips; does the fund house have adequate risk management measures in place in such a case?

-

✓ Is the fund manager compromising on the 'liquidity' aspects?

-

✓ ...and more such questions!

To reiterate, liquid funds are not risk free. Keep in mind that when you approach a Liquid Fund, returns should be secondary. Therefore, do not go after a Liquid Fund that has a high credit risk exposure. You should not invest in a liquid scheme solely based on past returns, as certain schemes may have achieved higher returns by taking additional risk.

Prefer a pure Liquid Fund that invests in G-Secs, Treasury Bills (T-Bills), and AAA/A1+ rated Public Sector Undertakings -- with no exposure to private corporate credit risk papers -- so that the safety and liquidity are not compromised. After all, it is the question of your hard-earned money.

So, apart from the above, it is important to evaluate the following to select the best Liquid Fund:

Concentration of portfolio

In the aftermath of the IL&FS and DHFL fiascos, concentration of a portfolio has become one of the most crucial parameters to watch out for while investing in Liquid Funds. If a fund house has a tendency to invest over 5% of its assets in single debt security and 10% in instruments issued by a single private issuer, you need to be careful. Moreover, you should also be wary of fund houses investing a significant portion of their assets in group companies.

Average Maturity and Modified Duration

The average maturity of the debt mutual fund scheme should be low at around 30-90 days so that it is less vulnerable to interest rate movements.

The interest rate sensitivity of a bond is measured vide its modified duration.

Modified duration measures the sensitivity spectrum of the bond price in relation to a change in interest rates.

It is a vital measure for you to consider because it includes all components of a bond: price, coupon, maturity date, and interest rate to calculate the modified duration.

Therefore, the modified duration can help you recognise that a bond portfolio with a higher modified duration will have high price volatility. Thus, Liquid Funds with a lower duration will be lower risk.

Yield-to-maturity (YTM)

YTM is simply an anticipated rate of return if the bond is held until the maturity date. It is also known as redemption yield. It measures the interest income generated by the bonds in the portfolio.

YTM takes into account the current market price, the face value, the interest payment that will fall due on the bond, and years left in its maturity.

YTM can be used as an approximate measure of the returns that a fund can generate over its average maturity period.

Cutting back excessive reliance on credit rating agencies

As you may know, debt instruments in India are rated on the basis of their creditworthiness by various credit rating agencies such as CRISIL, CARE, ICRA, amongst others.

Hence, credit ratings for debt instruments in the portfolio of a debt mutual fund scheme can throw some light on the qualitative aspects as it helps you assess the credit risk.

If the portfolio consists of securities with the highest credit rating, it implies that the portfolio's exposure to default risk is lower.

With the rise in the number of downgrades, it is very important to check how risk-averse the fund manager is and whether your risk appetite is in line with the fund you plan to invest in.

In the evaluation process, you should be concerned if the mutual fund house lacks robust risk management framework, depends excessively on ratings assigned by credit rating agencies; if the fund manager compromises on the quality of the portfolio, chases yields, and plays down on the liquidity aspects of the portfolio.

Outlook for Liquid Funds

The capital market regulator has recently made it mandatory for liquid funds to hold at least 20% of its net assets in liquid assets such as cash, Government Securities (G-Secs), treasury, and repo on G-Secs from April 1, 2020. And, in case the liquid assets drop below the prescribed level of 20%, then mutual fund houses are expected to make up for the shortfall.

[Read: Do The New Valuation Norms For Debt Mutual Funds Affect Your Investments?]

The regulator has also taken the following other measures in the interest of debt mutual fund investors:

-

Directed debt and money market instruments to value their portfolio on a mark-to-market basis (in wake of the credit crisis).

-

Disallowed Liquid Funds and Overnight Funds to invest in short-term deposits, debt, and money market securities having structured obligations or credit enhancements.

-

A 'graded exit load' on Liquid Funds, when redemptions are within 7 days (A move in the interest of retail investors, who are exposed to high risk when corporate or institutions invest and redeem large chunks of money)

-

Directed fund houses that fresh investments in Commercial Papers (CPs) shall be made only in listed CPs.

-

Capped the exposure of mutual fund schemes to 10% of their assets in debt and money market instruments with credit enhancements and restricted the group exposure to such securities to not more than 5%.

-

Directed fund houses to have at least 4 times security cover for investment by mutual fund scheme in debt securities having credit enhancements backed by equities directly or indirectly.

-

And even pulled up rating agency for laxity and issued guidelines to enhance disclosure by rating agencies

End note:

PersonalFN is of the view that sensible and astute investment strategy paves the path to wealth creation and is always good for your long-term financial well-being.

So, it would be sensible to evaluate the portfolio of a Liquid Fund with care. The portfolio, ideally, should be constructed in a way that ensures your hard-earned money is prudently parked in safe and liquid instruments, and the fund is managed well to earn a slightly better return than the money in a savings bank account (but not extra-ordinary returns). Hence, scheme selection plays a pivotal role.

It is essential that the Liquid Fund follows the true spirit of the product. A pure Liquid Fund will maintain its risk exposure moderate-to-low; prioritise safety, liquidity, and will not chase yields or credit risk for high returns.

Nevertheless, assess your risk appetite and investment time horizon while investing in debt funds.

Author: Aditi Murkute