DICGC Insurance Cover to Increase. Here’s How You Could Maximise Bank Deposit Insurance

Mitali Dhoke

Feb 24, 2025 / Reading Time: Approx. 8 mins

Listen to DICGC Insurance Cover to Increase. Here’s How You Could Maximise Bank Deposit Insurance

00:00

00:00

Since its introduction in 1962, the deposit insurance limit has been revised upwards six times. It was initially set at Rs 1,500 per depositor and increased to Rs 1 lakh in May 1993, before being raised to Rs 5 lakh on 4 February 2020.

Media reports now suggest that the government may nearly double the existing limit.

Speaking at a post-Budget press briefing in Mumbai on February 17, 2025, Mr M Nagaraju, the Secretary to the Department of Financial Services stated, "That [increasing deposit insurance] is under active consideration. As and when the government approves, we will notify it."

Finance Minister Ms Nirmala Sitharaman and other secretaries across various departments also attended the briefing.

This announcement came in the wake of the RBI's recent action against the Mumbai-based New India Co-operative Bank.

On 13 February 2025, the bank was placed under the Prompt Corrective Action (PCA) framework due to liquidity concerns. As a result, it was barred from issuing loans, accepting new deposits, or allowing withdrawals for six months.

The financial troubles of New India Co-operative Bank have been ongoing. Its annual report for the financial year ending March 2024 revealed a loss of Rs 22.78 crore, following a Rs 30.75 crore loss the previous year.

Investigations later uncovered that the bank's General Manager and Head of Accounts, Hitesh Mehta, had embezzled Rs 122 crore over a year, further destabilising the institution.

Bank fixed deposits (FDs) are considered a relatively safer investment option. However, instances like these - notably the Punjab and Maharashtra Co-operative Bank (PMC) scandal in 2019, which left nearly a million depositors unable to access their life savings - highlight the risks associated with banking failures.

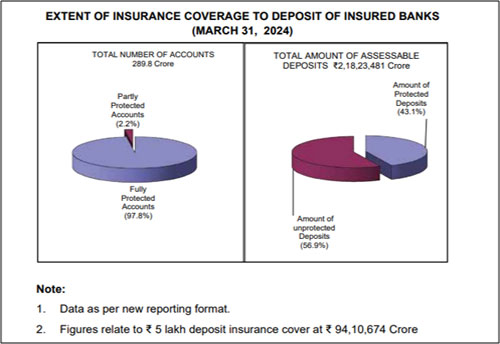

According to the DICGC Annual Report 2023-24, the current insurance coverage protects 98% of deposit accounts but only covers 43.1% of the total value of deposits.

Data as of March 31, 2024

Data as of March 31, 2024

(Source: DICGC Annual Report 23-24)

Raising the insurance limit shall provide greater financial security to depositors, particularly those with higher balances in banks.

Let's better understand how the bank deposit insurance by DICGC works and how you can make the most of your FDs in light of the potential increase in the insured limit.

The DICGC insures all deposits including savings, fixed, current, and recurring, except for the following:

-

Deposits of state/central governments

-

Deposits of foreign governments

-

Inter-bank deposits

-

Deposits of the State Land Development Banks with the State Co-operative Bank

-

Any amount due on account of India and deposits received outside India

-

Any funds that are exempted by the corporation with the previous approval of the RBI

Under the current rules, the RBI states, "Each depositor in a bank is insured up to a maximum of Rs 5,00,000 (Rupees Five Lakhs) for both principal and interest amount held by him in the same right and same capacity as on the date of liquidation/cancellation of bank's licence or the date on which the scheme of amalgamation/merger/reconstruction comes into force."

Let's work with the hypothesis that the deposit insurance limit would be increased to Rs 8 lakh.

This implies that all your accounts (savings, fixed, current, recurring, etc.) held in the same bank will be clubbed and you'll receive up to Rs 8 lakh in total insurance, including principal plus interest.

For example, assume that you have Rs 40,000 in interest accrued over the years from Rs 8 lakh that you deposited in a bank's savings and fixed deposit accounts.

In this scenario, you will receive up to Rs 8,00,000 in bank deposit insurance if the bank collapses.

Now, as stated by the RBI, the bank deposit insurance only applies to deposits held in the same capacity and in the same right. To get extra insurance coverage, you can maintain bank deposits in different rights and capacities.

This means that you would receive a maximum of Rs 8 lakh in bank deposit insurance if you hold all your bank deposits in your single name. However, if you split your deposits across distinct rights and capacities - such as joint accounts with your spouse, children, or siblings - you would be eligible for separate insurance cover for each deposit.

Here's an illustration of how this might work:

| Account Holder |

Right and Capacity of the Account |

Savings A/C (Rs) |

Current A/C (Rs) |

FD A/C (Rs) |

Total Deposits (Rs) |

Deposit Insurance Eligible for the Amount (Rs) |

| Mr Rajesh |

Individual account in PQR Bank |

4,20,000 |

25,000 |

85,000 |

5,30,000 |

Up to 8,00,000 |

| Mr Rajesh + Mrs Pooja |

Joint account with spouse in PQR Bank |

5,00,000 |

4,80,000 |

55,000 |

10,35,000 |

Up to 8,00,000 |

| Mrs Pooja + Mr Rajesh |

Joint account with spouse (in a different order) in PQR Bank |

1,00,000 |

0 |

3,85,000 |

4,85,000 |

Up to 8,00,000 |

| Mr Rajesh + Arjun |

Guardian for a child (minor) in PQR Bank |

90,000 |

4,40,000 |

2,50,000 |

7,80,000 |

Up to 8,00,000 |

| Mr Rajesh |

Individual account in XYZ Bank |

4,50,000 |

30,000 |

80,000 |

5,60,000 |

Up to 8,00,000 |

| Mr Rajesh + Mrs Pooja |

Joint account with spouse in XYZ Bank |

5,10,000 |

4,90,000 |

60,000 |

10,60,000 |

Up to 8,00,000 |

| Total deposit insurance cover |

|

|

|

|

|

Up to Rs 48,00,000 |

(The above table is for illustrative purposes only)

This way, you can maximise your deposit insurance coverage with more such combinations of different rights and capacities, and spread your deposits across different banks.

A few parting tips to keep in mind...

-

Choose banks that are well-regulated by the RBI.

-

Regularly monitor the banks' financial health.

-

Stay informed about any regulatory changes that affect deposit insurance.

-

Be wary of unusually high FD interest rates, as they often indicate higher risk.

-

Diversify your investments across equity mutual funds, debt instruments, gold, and other asset classes.

To Conclude...

Given the increasing instances of banks failing in India, the proposed increase in the DICGC insurance coverage is a necessary measure for protecting the hard-earned money of lakhs of depositors in India.

To maximise your coverage, spread your FDs across multiple well-regulated banks and maintain deposits under different rights and capacities.

For a well-rounded investment strategy, diversify your portfolio across asset classes like equity mutual funds, debt instruments, and gold, tailored to your risk profile and financial goals.

Happy investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

MITALI DHOKE is a Research Analyst at PersonalFN. She is an MBA (Finance) and a post-graduate in commerce (M. Com). She focuses primarily on covering articles around mutual funds including NFOs, financial planning and fixed-income products. Mitali holds an overall experience of 4 years in the financial services industry.

She also actively contributes towards content creation for PersonalFN’s social media platforms in the endeavour to educate investors and enhance their financial knowledge.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.