India’s CPI Inflation for March At a 67-Month Low. What It Means for Interest Rates and Debt Investors

Rounaq Neroy

Apr 17, 2025 / Reading Time: Approx. 9 mins

Listen to India’s CPI Inflation for March At a 67-Month Low. What It Means for Interest Rates and Debt Investors

00:00

00:00

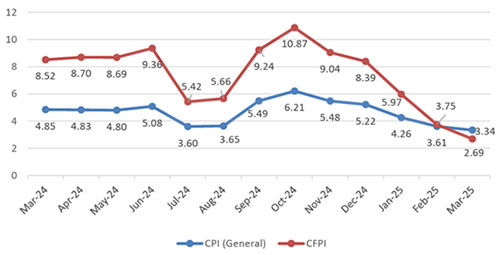

India's CPI inflation reading for March 2025 (data released in April) has come in at 3.34%. This is the lowest year-on-year (y-o-y) reading since August 2019. Sequentially too the retail inflation has declined by 27 basis points (bps). Having said that, the y-o-y CPI inflation reading in the urban region is slightly higher (at 3.43% in March 2025) compared to the previous month and relative to the CPI inflation for the rural region.

Lower y-o-y food inflation at 2.69% in March 2025 is the key reason for all-India headline inflation plunging to a 67-month low. Compared to the previous month, food inflation has declined by a good 106 bps and is currently the lowest since February 2021, as per the data released by the Ministry of Statistics and Programme Implementation (MOSPI).

Graph 1: All India Inflation Rates for CPI(General) and CFPI Are Easing

Data as of April 15, 2025

Data as of April 15, 2025

(Source: MOSPI)

Lower inflation readings for vegetables, pulses, cereals, milk, and protein-rich items such as eggs, meat, and fish have proved supporting.

Fuel & light inflation, however, moved out of disinflation for the first time in 18 months with data for March 2025 coming in at 1.48% versus -1.33% in the previous month.

Core inflation -- which excludes food and fuel -- remained sticky at 4.10%. This was mainly due to higher inflation in household and miscellaneous items, plus in education, healthcare, transport & communication, and prices of precious metals.

The RBI has observed that while core inflation in the fiscal year 2024-25 exhibited some signs of higher inflation variability when compared to the previous year, the level of inflation and its variability were much lower than in other post-COVID years. In its assessment, core inflation pressures in 2024-25, on average, were muted and broad-based.

A fact is that despite higher core inflation, the headline inflation reading has remained well within the RBI's inflation target (of 4.00% within a band of +/- 2.00%) in the last couple of months.

The fiscal year 2024-25 ended with the average headline inflation reading of 4.62% vis-a-vis the average of 5.40% in the previous fiscal year.

For the fiscal year 2025-26, the RBI has projected the headline inflation at 4.00% (with Q1 at 3.60%; Q2 at 3.90%; Q3 at 3.80%; and Q4 at 4.40%), considering that food inflation has turned decisively positive and assuming a normal monsoon in 2025.

India's Meteorological Department (IMD), as you may know, has recently forecasted an above-normal monsoon in 2025 (105% of the Long Period Average of 87 centimetres), which is expected to augur well for agriculture and keep food inflation low.

Furthermore, the fall in crude oil prices bodes well for the inflation outlook.

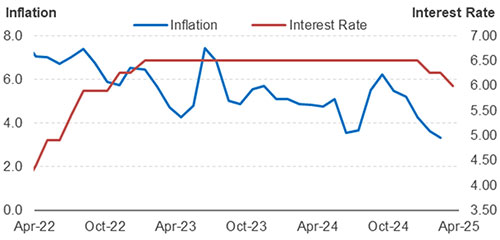

Impact of Lower Headline Inflation on Interest Rates

In the bi-monthly monetary policy meeting held earlier in April, the RBI stated that the challenging global economic conditions, the benign inflation, and the moderate growth outlook demand that the Monetary Policy Committee (MPC) continues to support growth.

Thus, the six-member MPC voted unanimously to reduce the policy repo rate by 25 bps to 6.00%. Moreover, the stance of monetary policy was changed from 'natural' to 'accommodative'.

It also noted that the rapidly evolving situation requires continuous monitoring and assessment of the economic outlook.

As per RBI's projections, there is now greater confidence of a durable alignment of headline inflation with the target of 4.00% over a 12-month horizon.

So far in CY2025, the RBI has already cut the policy rate by 50 bps. Given that inflation is now well within the target, it appears that the RBI would take this opportunity to cut the policy repo rate by another 25 bps in its ensuing bi-monthly monetary policy scheduled in June 2025 (to be held between June 4 to 6, 2025).

Graph 2: Inflation v/s Interest Rates

Data as of April 15, 2025

Data as of April 15, 2025

(Source: MOSPI, RBI Monetary Policy Statements)

In simple words, it means that interest rates in the economy would move down. As a result, there will be further transmission to the lending rates and deposit rates.

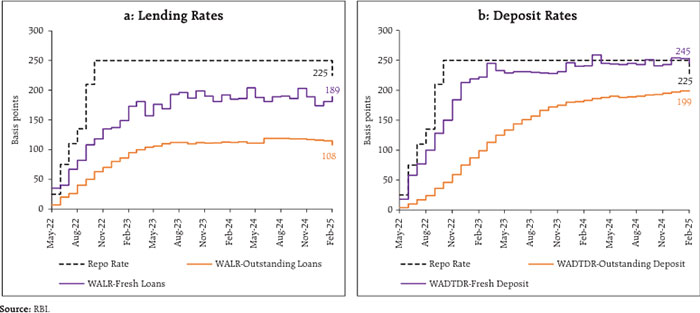

Graph 3: Transmission to Bank's Lending and Deposit Rates

(Source: RBI Monetary Policy Report, April 2025)

(Source: RBI Monetary Policy Report, April 2025)

For bank depositors, it implies that interest rates on fixed deposits (FDs) would go down in time to come. It would particularly impact risk-averse investors and retirees who prefer FDs to earn stable/fixed returns to manage their cash flow needs.

Before the RBI cuts the policy interest rates further, it makes sense to invest in bank FDs. To maximise the returns on the bank FD, consider following the laddering strategy whereby you can maximise returns and take care of your liquidity needs.

Investment Strategy to Invest in Debt Mutual Funds

As you may know, interest rates and bond yields are directly related to each other, whereas bond yields and bond prices are inversely related to each other.

In the current scenario where interest rates are headed down, it makes sense to take exposure to the longer end of the yield curve. Simply put, it would be meaningful to invest in medium-to-long maturity papers to benefit from the potential capital appreciation.

As interest rates decrease, the fund value or the NAV of Medium-to-Long Duration Debt Mutual Funds is expected to increase. You may allocate around 25% of your debt mutual fund portfolio to some of the best Medium-to-Long Duration Debt Funds, keeping an investment horizon of 3 to 5 years.

That being said, keep in mind that Medium-to-Long Duration Debt Funds are moderate-to-high-risk contenders. This is due to the interest rate sensitivity of these funds, as well as the fact that there is a slight credit risk. The higher the modified duration of the scheme, the higher will be its sensitivity to interest rates. To take a calculated risk, make sure the maturity profile of the scheme you zero in on is up to 5 years or so with G-secs making up around 30%. For this, evaluate the portfolio characteristics of the scheme and check the investment processes and systems followed at the fund house.

If you wish to play the interest rate cycle and have an exposure dynamically to short and medium-to-long maturity debt papers, some of the best Dynamic Bond Funds can be a meaningful choice, provided you have an investment horizon of 3 to 5 years. Around 25% of your debt mutual fund portfolio could be allocated to some of the best Dynamic Bond Funds.

Regardless of the direction in which interest rates move, Dynamic Bond Funds are capable of taking advantage of dynamic market conditions and can invest accordingly to create an all-season portfolio that generates optimal returns. Nevertheless, it is critical to invest in Dynamic Bond Funds that hold a robust portfolio of securities across maturities and high-quality debt & money market instruments.

Similarly, investing in some of the Banking & PSU Debt Funds can be a good alternative if you have an investment time horizon of around 2 to 3 years. Banking & PSU Debt Funds are mandated to invest predominantly (80% of their assets) in top-rated corporate debt instruments issued by Banks, Public Sector Undertaking (PSUs), Public Financial Institutions (PFIs), Municipal bonds, and other such securities. These entities are recognised for their robust credibility and liquidity compared to those from private issuers, making them a relatively safer investment option. Banking & PSU Debt Funds have exposure to debt papers across the yield curve but typically maintain a duration of around 3 to 5 years.

For a shorter investment horizon of up to a year or so, it would be better to stick to some of the best Liquid Funds having the least or no exposure to private issuers. Investing in some of the best Liquid Funds is a sensible way to hold some money safe, whereby it can offer you liquidity, help address unforeseen circumstances, and meet short-term financial goals.

Keep in mind that investing in debt funds, in general, is not risk-free, and hence choosing the safety of the principal over returns is imperative. Avoid debt funds that compromise on the portfolio characteristics and engage in yield hunting to clock higher returns.

[Read: Best Debt Mutual Fund Categories for 2025]

To conclude...

If you keep an eye on the evolving macroeconomic dynamics, consider the interest cycle, and devise a sensible investment strategy, the return from your debt mutual portfolio can improve as opposed to investing in an ad hoc manner.

Select debt mutual fund schemes that align well with your personal risk profile, investment objective, and investment horizon.

Moreover, make sure the debt mutual fund portfolio is well-diversified, and you are considering their portfolio characteristics, the risk ratios, and not making the decision merely by looking at historical returns (which are in no way indicative of future returns). This shall help you earn decent risk-adjusted returns.

Follow a sensible asset allocation model in CY2025 and beyond.

Be a thoughtful investor.

Happy Investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.