5 Best Mutual Funds for Your Retirement Trading at 10-20% Discount

PersonalFN Content & Research Team

Jun 20, 2022

Listen to 5 Best Mutual Funds for Your Retirement Trading at 10-20% Discount

00:00

00:00

Introduction to Retirement Mutual Funds

Something shocking is happening. Retail Indian investors, the ones who have never given priority to retirement planning, are suddenly showing renewed interest in planning for their retirement. As per google trends, the interest in 'best mutual funds for retirement' has skyrocketed 450%, while the search volume for 'retirement mutual funds' has surged 160%.

Now we must admit that this unexpected increase in searches for the best mutual funds for retirement perplexed us. Like you, we also wondered why this sudden craze for retirement planning? Russia-Ukraine remains at loggerheads; the US inflation data is at its 40-year peak. Brent crude is slumping everyday on the back of weak demand from China as Covid-19 cases surge, while the world economy grapples with the ever-present danger of a recession. So exactly what changed overnight that investors across the globe woke up from their slumber with fresh intent to invest for their retirement? And then, like a bolt of lightning, it hit us... the sheer uncertainties brought on by these global events are what triggered, encouraged or even forced retail investors to stop postponing planning for their golden years and look for the best mutual funds for retirement.

[Must Read: Ignore This Retirement Opportunity & Regret it Forever]

As luck would have it, we have shortlisted the five best mutual funds for retirement in 2022, spread across a variety of categories like large cap, mid cap, flexi cap, value, and hybrid mutual funds. And do you want to know the best part? All of these best mutual funds for retirement are available at a heavy discount of 10-20% from their October 2021 levels. As the broader stock market index, the Nifty moves in the attractively valued zone on the back of a PE ratio of 19.40, levels last seen during the stock market crash of March 2020; this is one of the best times to invest in these five best mutual funds for your retirement.

[Free Calculator: Find out how much money you need to retire peacefully]

Should you invest in Retirement Mutual Funds?

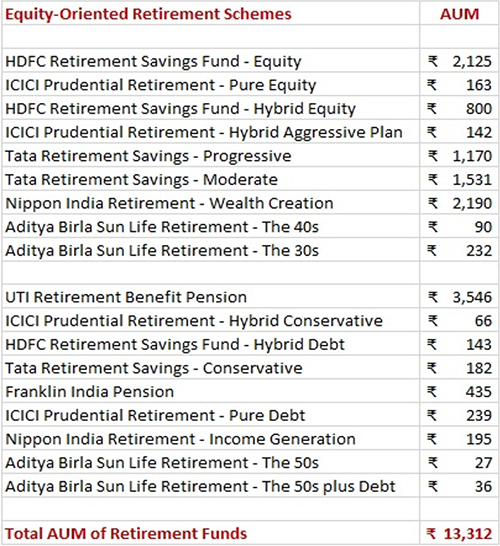

A heads up... if you are expecting us to recommend solution-oriented retirement mutual funds in this article, then you would be disappointed, but most importantly, you would be wrong. The growth of retirement mutual funds has been lacklustre, and even the performance of these funds is nothing to write home about. The AUM of the Indian mutual fund industry stands at a mammoth Rs 37.22 trillion as of May 31, 2022. Of this, the AUM of retirement mutual funds, both equity and debt oriented combined, stands at a meagre Rs 13,312 crores, which is 0.36% of the total AUM, so not even half a percent.

Table 1: AUM of Retirement Funds

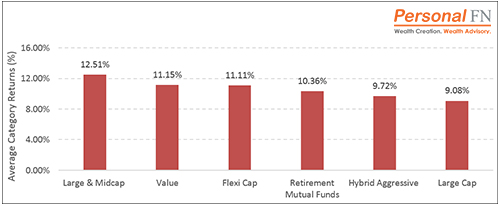

The mediocre demand for retirement mutual funds isn't entire unwarranted as these funds have posted substandard performance compared to their equity counterparts. The table below shows the average performance of retirement mutual funds in the last one, three and five-year periods as of June 16, 2022.

Table 2: Performance of Equity-oriented Retirement Mutual Funds

| Retirement Mutual Fund |

1-Year |

3-Years |

5-Years |

| HDFC Retirement Savings Fund - Equity |

3.05% |

16.99% |

13.26% |

| ICICI Prudential Retirement - Pure Equity |

16.51% |

15.29% |

-- |

| HDFC Retirement Savings Fund - Hybrid Equity |

-0.68% |

11.88% |

10.85% |

| ICICI Prudential Retirement - Hybrid Aggressive Plan |

2.88% |

10.56% |

-- |

| Tata Retirement Savings - Progressive |

-5.60% |

9.96% |

9.40% |

| Tata Retirement Savings - Moderate |

-3.35% |

10.18% |

8.94% |

| Nippon India Retirement - Wealth Creation |

-1.47% |

5.10% |

6.05% |

| Aditya Birla Sun Life Retirement - The 40s |

-6.50% |

6.65% |

-- |

| Aditya Birla Sun Life Retirement - The 30s |

-8.21% |

6.60% |

-- |

| Average Returns |

-0.37% |

10.36% |

9.70% |

Source: ACE MF, PersonalFN Research

Data as on June 16, 2022

As you can see, the average returns generated by equity-oriented retirement mutual funds in a 3-year period is 9.70%, which is subpar compared to large-cap funds (12.51%), Flexi-cap funds (11.11%), mid-cap funds (16.35%) and even value funds (11.15%).

Graph 1: Performance of Equity-oriented Retirement Mutual Funds

Source: ACE MF, PersonalFN Research

Source: ACE MF, PersonalFN Research

Data as on June 16, 2022

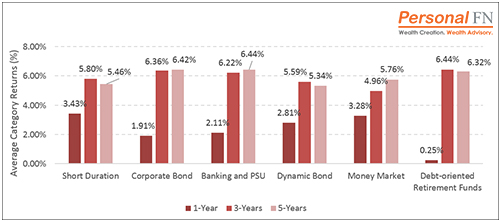

Even debt-oriented retirement mutual funds failed to show any magic and have trailed other debt fund categories like money market funds, short duration, and dynamic bond funds. The performance has been especially poor in the last one year, where even money market funds, with a return of 3.28% in the last one year (as of June 16, 2022), have beaten debt-oriented retirement funds.

Graph 2: Performance of Debt-oriented Retirement Mutual Funds

Source: ACE MF, PersonalFN Research

Source: ACE MF, PersonalFN Research

Data as on June 16, 2022

Why Retirement Mutual Funds Aren't the Best Investment Option

While performance is one of the biggest criteria, it is not the only reason for the lack of interest in retirement mutual funds. The other drawbacks of retirement mutual funds are:

-

Compared to equity and debt funds, retirement mutual funds have a longer lock-in period. For instance, the lock-in period of Nippon India Retirement - Wealth Creation, one of the biggest retirement mutual funds in India with an AUM of Rs 2,190 (as of May 31, 2022), is 5 years. This is much higher than the one-year lock-in period of equity mutual funds. So, investors are (forcibly) locked in for a minimum of 5 years, even if the fund performs poorly.

-

Another issue with retirement mutual funds is the high expense ratio. Some retirement funds like Franklin India Pension Fund, a debt-oriented retirement fund, charge expense ratio as high as 1.51%, much higher than pure equity funds.

-

Some retirement mutual funds like Franklin India Pension Plan also offer tax benefits under section 80C, which prompted many investors to invest in these retirement funds. But post-2016, the SEBI has not allowed investment in any new retirement fund to qualify for an 80C deduction, squashing investor hopes for a tax benefit.

How are Retirement Mutual Funds Taxed?

The taxation of retirement mutual funds is often a point of contention. So, let us set the record straight once and for all. Equity-oriented retirement funds, ones which invest more than 65% of their corpus in equities, will follow equity taxation, wherein the minimum taxation period is one year.

Taxation of Equity-oriented Retirement Mutual Funds

-

If you sell your equity-oriented retirement fund before one year, you will have to pay a short-term capital gains tax (STCG) of 15%+ cess.

-

If you sell your equity-oriented retirement fund after one year and the capital gains are more than Rs 1 Lakh, then you will have to pay a 10% long-term capital gains tax. In case your capital gains are less than Rs 1 Lakh, then you do not have to pay any tax.

-

Dividends received under the Income Distribution cum Capital Withdrawal plan (IDCW) will be taxable as per individual tax bracket, however the fund house will deduct TDS @10% for resident investors and 20% for NRIs.

Taxation of Debt-oriented Retirement Mutual Funds

If you hold a debt-oriented retirement mutual fund, one which invests heavily (65%-80%) in debt instruments, then your taxation holding period is 36 months.

-

If you sell your units post three years, then you can claim the benefit of indexation, and the tax rate will be 20% (post indexation).

-

If you sell your units before three years, then your short-term gains will be added to your income and taxed as per applicable tax slabs.

-

The dividend treatment remains the same for both equity and debt-oriented retirement mutual funds, wherein dividends will be taxable as per individual tax bracket, and the fund house will deduct TDS @10% for resident investors and 20% for NRIs.

We hope that by now, you have a clear understanding of the world of retirement mutual funds, as it's now time to reveal the list of the five best retirement mutual funds in 2022.

Best Mutual Funds for Retirement in 2022

| Best Retirement Mutual Funds |

3-Year |

5-Year |

7-Year |

| Canara Robeco Bluechip Equity Fund |

14.05 |

13.04 |

12.92 |

| Kotak Emerging Equity Fund |

20.19 |

13.2 |

15.77 |

| Parag Parikh Flexi Cap Fund |

20.66 |

16.61 |

15.44 |

| Mirae Asset Hybrid Equity Fund |

11.53 |

11.28 |

- |

| ICICI Prudential Value Discovery Fund |

17.77 |

12.3 |

11.73 |

(Source: Ace MF, PersonalFN Research)

Returns as on June 06, 2022.

*Please note, this table only represents the best performing Small cap Funds based solely on past returns and is NOT a recommendation. Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not an indicator of future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

We will be beginning our list with the safest mutual fund category - large-cap mutual funds.

Best Mutual Fund for Retirement - Large Cap Category - Canara Robeco Bluechip Equity Fund

Large-cap mutual funds predominantly invest in blue-chip companies, which are the top 100 companies listed on the exchange in terms of market capitalisation. These companies are market leaders with well-established products and services, customer loyalty and strong economic moats, making them adept at handling economic downturns. Amongst the universe of large-cap mutual funds, the one which makes it to our list of best retirement funds is Canara Robeco Bluechip Equity Fund.

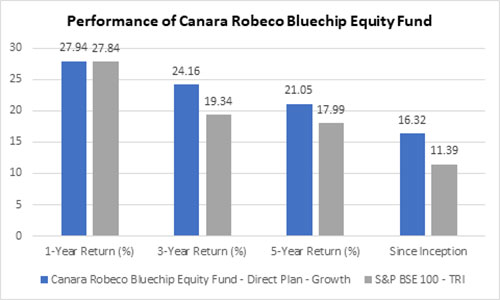

Graph 3: Performance of Canara Robeco Bluechip Equity Fund

Source: ACE MF, PersonalFN Research

Source: ACE MF, PersonalFN Research

Data as on June 16, 2022

A conservative large-cap fund, Canara Robeco Bluechip Equity Fund has generated a return of 14.05% in the last three years against a benchmark return of 10.97% and 13.04% against 11.01% in the last five years (as of June 16, 2022), making it the number one large-cap fund in the five year period. The fund is bullish on the financial (33.47%), technology (13.43%), energy (11.27%), and consumer staples sectors (7.28%).

The fund, with the NAV of Rs 40.07 as on June 16, 2022, is currently available at a discount of 16% to its October 18, 2021 high of Rs 48.20. With a price-to-equity ratio of 26.56 and a price-to-book ratio of 3.59, Canara Robeco Bluechip Equity Fund is indeed one of the best mutual funds for your retirement.

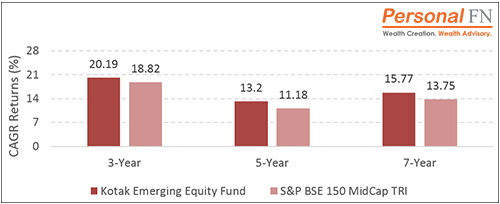

Best Mutual Fund for Retirement - Midcap Category - Kotak Emerging Equity Fund

Investing in midcap funds is one of the best things you can do for retirement. Midcap funds are inherently risky but have a history of superior performance in the long run, and since retirement is also a long-term goal, midcap funds and retirement planning are a match made in heaven. The midcap category hasn't disappointed either, with a three-year return of 16.54% as of June 17, 2022. So, which is the best midcap fund for your retirement? While it was a tough competition, Kotak Emerging Equity Fund wins the race for the best midcap fund for your retirement.

With an AUM of Rs 18,655 crore as of May 31, 2022, Kotak Emerging Equity Fund is one of the biggest midcap funds in India. Despite such a mammoth AUM, which can cripple a fund, Kotak Emerging Equity Fund has managed to remain in the top 5 best midcap funds across five, seven, and ten-year horizons. In a three-year period, the fund has outperformed its benchmark by generating a return of 20.19% against a benchmark return of 18.82% (as of June 16, 2022).

Graph 4: Performance of Kotak Emerging Equity Funds

Source: ACE MF, PersonalFN Research

Source: ACE MF, PersonalFN Research

Data as on June 16, 2022

The fund holds a well-diversified portfolio of 71 stocks, and its performance has benefitted greatly from its higher than category exposure to capital goods (17.75%), consumer discretionary (11.89%), financials, (11.56%) and chemicals sector (11.47%).

In terms of valuations, Kotak Emerging Equity Fund, with a NAV of Rs 71.48 (as on June 17, 2022), is currently available at a discount of 14% from its October 18, 2022 high of Rs 83.10. The fund is decently valued with a price to equity ratio of 27.33 and a price to book value of 4.28.

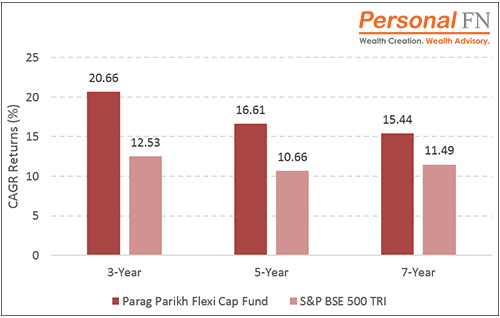

Best Mutual Fund for Retirement - Flexi Cap Category - Parag Parikh Flexi Cap Fund

If you don't want to commit to a single category and would rather have an expert fund manager decide the sector (large, mid, or small) to bet on, then Flexi cap funds are just what you need. A little more lenient than multi-cap funds, Flexi-cap funds have the freedom to invest across large, mid, and small-cap stocks without any fixed minimum allocation. So, if the fund manager fears an economic slowdown, then he can close his mid and small-cap positions and shift to large-cap stocks.

With a robust and compact portfolio of 26 stocks, Parag Parikh Flexi Cap Fund has managed to top the ratings in the Flexi cap category across all three, five, and seven-year time horizons. The fund has outperformed its benchmark, creating an enviable alpha of 10.30% over its benchmark index, S&P BSE 500 TRI.

Graph 5: Performance of Parag Parikh Flexi Cap Fund

Source: ACE MF, PersonalFN Research

Source: ACE MF, PersonalFN Research

Data as on June 16, 2022

The NAV of Parag Parikh Flexi Cap Fund on June 17, 2022, is Rs 45.43, which is at a discount of 18% to its October 18, 2021 high of Rs 55.14. With a price-to-equity ratio of 19.15 and a price-to-book value of 3.13, Parag Parikh Flexi Cap Fund is a must in your retirement portfolio.

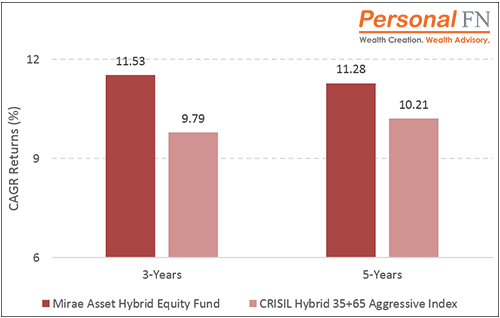

Best Mutual Fund for Retirement - Aggressive Hybrid Fund - Mirae Asset Hybrid Equity Fund

An aggressive Hybrid Fund is apt for first-time investors who want a taste of the equity markets without going all in. Aggressive hybrid funds invest in a mix of equity and debt with a minimum investment of 65%-80% in equity stocks and 20%-35% in debt instruments like bonds, debentures and other money market instruments.

The aggressive fund that makes it to our list of best mutual funds for retirement is Mirae Asset Hybrid Equity Fund. The fund is a bit conservative in its approach as it holds 73.30% of its portfolio in equities, 23% in debt, and 3.7% in cash and cash equivalents, which is higher than other aggressive hybrid funds. However, this helps the fund achieve a price-to-earnings ratio of 19.66 and a price-to-book value of 3.06. Currently available at the NAV of Rs 22.07, the fund is trading at a 13% discount to its October 18, 2021, high of Rs 25.43. The fund has put forth a decent performance and has even managed to create an alpha of 2.09% over its benchmark, the CRISIL Hybrid 35+65 Aggressive Index.

Graph 6: Performance of Mirae Asset Hybrid Equity Fund

Source: ACE MF, PersonalFN Research

Source: ACE MF, PersonalFN Research

Data as on June 17, 2022

And finally, our last recommendation for your retirement portfolio is from the value fund category.

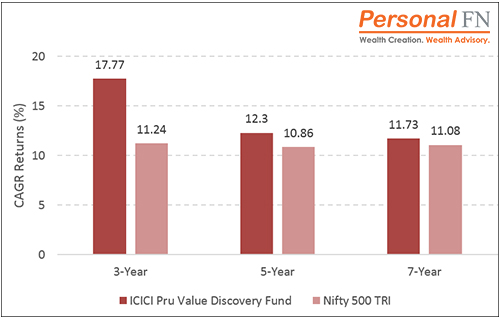

Best Mutual Fund for Retirement - Value Fund - ICICI Prudential Value Discovery Fund

While Value Funds are on the receiving end of brickbats from investors due to their substandard performance compared to growth stocks, value funds have proved their mettle, especially during economic slowdowns, as seen by a three-year category return of 11.40% as of June 17, 2022, surpassing the 9.29% return generated by large-cap fund category.

Our recommendation in the value fund category is ICICI Prudential Value Discovery Fund. The fund is the biggest value fund, with an AUM of Rs 23,732 crore as of May 31, 2022. It has generated a stellar return of 17.77% in the last three years and a return of 12.30% in the last five years as of June 17, 2022.

Graph 7: Performance of ICICI Prudential Value Discovery Fund

Source: ACE MF, PersonalFN Research

Source: ACE MF, PersonalFN Research

Data as on June 17, 2022

The fund invests in 67 stocks with the highest exposure to financial (18.19%), energy (17.49%), communication (13.52%), and the healthcare sector (11.83%). The fund is attractively valued with a price-to-earnings ratio of 12.33 and a price-to-book value ratio of 1.78. Fortunately for you, the fund is available at a discount of 10% at a NAV of Rs 249.17, compared to its October 18, 2021, NAV of Rs 277.02.

These were the five best mutual funds for your retirement in 2022, available at a 10-20% discount from their October 2021 highs. Akin to shopping during sales, investing in these five best retirement mutual funds will help build a strong retirement portfolio at a bargain price.

If bargain hunting is something that excites you, then you will love our latest offering, Active Wealth Multiplier 2030. Like peanut butter and jelly, this product is ideal for investors who want a readymade portfolio alongside active tracking. And before you think that you can get these schemes for free on other websites, then let us set the record straight. The strategies used in Active Wealth Multiplier 2030 are unique, distinct and time-tested. You will NOT get such top-notch recommendations for FREE anywhere. Check out PersonalFN's Active Wealth Multiplier 2030 now.

Get Our Premium Service “The Active Wealth Multiplier 2030” Now

Warm Regards

PersonalFN Content & Research Team

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds

DISCLOSURE AS PER SECURITIES AND EXCHANGE BOARD OF INDIA (RESEARCH ANALYSTS) REGULATIONS, 2014

About the Company including business activity

Quantum Information Services Private Limited (QIS) was incorporated on December 19, 1989.

QIS was promoted by Mr Ajit Dayal with an objective of providing value-based information/views on news related to equity markets, the economy in general, sector analysis, budget review and various personal products and investments options available to the Public. It was the first company to start equity research on an institutional level.

'PersonalFN' is a service brand of QIS and was started in the year 1999. In 1999, the Company registered the Domain name www.personalfn.com for providing information on mutual funds and personal financial planning, financial markets in general, etc. and services related to financial planning and research in various financial instruments including mutual funds, insurance and fixed income products to customers. It offers asset allocation and researched investment recommendations through its financial planning services.

Quantum Information Services Private Limited (QIS) is registered as Investment Adviser under SEBI (Investment Adviser) Regulations, 2013 and having Registration No.: INA000000680. In terms of the second proviso to Regulation 3 (1) of SEBI (Research Analysts) Regulations, 2014 the Company is not required to obtain Certificate of registration from SEBI.

Disciplinary history

There are no outstanding litigations against the Company, its subsidiaries and its Directors.

Terms and condition on which its offer research report

For the terms and condition for research report click here.

Details of associates

-

Money Simplified Services Private Limited;

-

PersonalFN Insurance Services India Private Limited;

-

Equitymaster Agora Research Private Limited;

-

Common Sense Living Private Limited;

-

Quantum Advisors Private Limited;

-

Quantum Asset Management Company Private Limited;

-

HelpYourNGO.com India Private Limited;

-

HelpYourNGO Foundation;

-

Natural Streets for Performing Arts Foundation;

-

Primary Real Estate Advisors Private Limited;

-

HYNGO India Private Limited;

-

Suresh Lulla;

-

I V Subramaniam;

-

Murali Ananthan Krishnan.

Disclosure with regard to ownership and material conflicts of interest

-

‘subject company’ is a scheme on which a buy/sell/hold view or target price is given/changed in this Research Report;

-

Neither QIS, it's Associates, Research Analyst or his/her relative have any financial interest in the subject Company;

-

Neither QIS, it's Associates, Research Analyst or his/her relative have actual/beneficial ownership of one per cent or more securities of the subject Company, at the end of the month immediately preceding the date of publication of the research report;

-

Neither QIS, it's Associates, Research Analyst or his/her relative has any other material conflict of interest at the time of publication of the research report except that QIS (PersonalFN) is, as per SEBI (Mutual Funds) Regulations 1996, an associate / group Company of Quantum Asset Management Company Private Limited and Trustees and Sponsor of Quantum Mutual Fund (QMF) and to that extent there may be conflict of interest while recommending any schemes of QMF. However, any such recommendation or reference made is based on the standard evaluation and selection process, which applies uniformly for all Mutual Fund Schemes. The payment of commission (upfront / annualized & trail), if any, for any Schemes by QMF to QIS (PersonalFN) is also at arm's length and as per prevailing market practices.

Disclosure with regard to receipt of Compensation

-

Neither QIS nor it's Associates have received any compensation from the subject Company in the past twelve months;

-

Neither QIS nor it's Associates have managed or co-managed public offering of securities for the subject Company;

-

Neither QIS nor it's Associates have received any compensation for investment banking or merchant banking or brokerage services from the subject Company;

-

Neither QIS nor it's Associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months.

-

Neither QIS nor it's Associates have received any compensation or other benefits from the subject Company or third party in connection with the research report

General disclosure

-

The Research Analyst has not served as an officer, director or employee of the subject Company.

-

QIS or the Research Analyst has not been engaged in market making activity for the subject Company.

Click here to read PersonalFN's Mutual Fund Rating Methodology

Subject Company means Mutual Fund Schemes

Quantum Information Services Private Limited CIN: U65990MH1989PTC054667 Regd. & Corp. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021

Email:info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013