Will Home Loan Rates Go Down in the New Year 2025? Here’s What to Expect

Hiral Bhuta

Feb 01, 2025 / Reading Time: Approx. 9 mins

Listen to Will Home Loan Rates Go Down in the New Year 2025? Here’s What to Expect

00:00

00:00

For many aspiring homeowners, securing a home loan is a vital step towards realising their dream of owning a home. However, the financial burden of substantial interest payments over the long term can strain borrowers' finances.

Unfortunately, the last couple of years have left borrowers bearing the brunt of elevated interest rates or borrowing costs.

As a measure to manage inflation and stimulate economic growth, the Reserve Bank of India (RBI) implemented a series of repo rate hikes, resulting in a cumulative increase of 250 basis points, between May 2022 and February 2023.

Consequently, lending institutions were compelled to increase their interest rates on home loans (and others), leading to a surge in Equated Monthly Instalments (EMIs) for borrowers with floating-rate loans.

But since February 2023, the RBI has maintained the policy repo rate at 6.50%. The December 2024 bi-monthly monetary policy meeting marked the 11th consecutive time, the six-member Monetary Policy Committee (MPC) of the RBI decided to keep the repo rate unchanged. A majority, i.e. 4 out of 6 members, voted in favour of keeping the policy repo rate unchanged considering the persistently high inflation.

------------------------------------------------------------------------------------

Want to Make Your Money Work While You Sleep?

Talk to Our Investment Advisors Today!

Schedule a First Consultation Call Right Now

------------------------------------------------------------------------------------

The MPC unanimously decided to continue with the 'neutral' monetary policy stance and to maintain an unambiguous focus on the durable alignment of inflation with the target, while supporting growth.

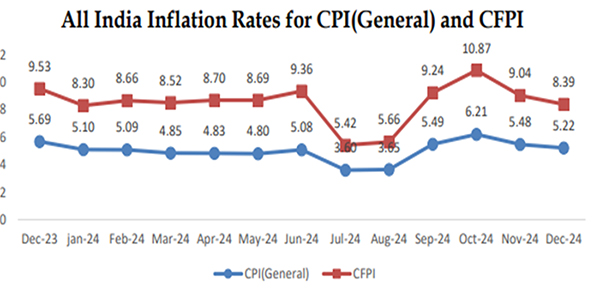

In October 2024, India's Consumer Price Index (CPI) inflation, also known as retail inflation, surged to 6.21%, reaching a 14-month high and breaching the RBI's tolerance threshold of 6%. This spike was largely attributed to rising food prices, which continue to exert upward pressure on overall inflation levels.

However, in the ensuing two months, November 2024 and December (as seen in the graph below) inflation has noticeably moderated - largely abetted by a decline in 'food and beverage' inflation (which has a weight of nearly 46% in headline inflation).

Graph: Food Prices Pushing Headline Inflation

Data as of January 13, 2025

Data as of January 13, 2025

(Source: MOSPI)

If the inflation continues to moderate and remains below RBI's target range of 4-6%, the RBI may consider lowering the policy repo rate in CY2025, possibly in the February 2025 or April 2025-26 bi-monthly monetary policy statement.

That being said, it would be important to monitor the global developments amidst the ongoing geopolitical tensions, as these could significantly impact global commodity prices and, in turn, contribute to 'imported inflation'. For the RBI, closely monitoring food prices would be crucial, as it directly impacts household budgets.

Will Home Loan Rates Go Down?

A significant number of home loan borrowers opt for floating or variable interest rates in India, owing to their responsiveness to shifts in monetary policy.

There is an advantage with floating interest rates: If the RBI reduces the policy repo rate, banks and housing finance companies reduce the interest rate and, as a result, the borrowers benefit by way of reduced EMIs or slightly earlier repayment of the loan, as the case may be.

In other words, it eases the repayment burden of existing borrowers and potentially increases demand from new home loan borrowers, thus helping the real estate sector.

Note that EMIs would gradually decrease with a repo rate cut, but the timing depends on the transmission mechanism adopted by the lender. Some lenders may adjust rates promptly, while others might take longer.

With effect from April 2019, banks are required to link their home loan rate to the EBLR. Earlier for loans taken between June 2010 and April 2016 it was the Base Rate, while for loans taken after April 2016 but before April 2019 it was MCLR.

The pace and extent of the rate cut will vary across these different interest rate structures and lending institutions.

But as a borrower, you need to keep watch on the upcoming bi-monthly policy meeting, which shall give you an indication of where interest rates are heading and accordingly proactively optimise your home loan by reaching out to the lending institution for an interest rate reset.

If you, the borrower, have a floating-rate home loan, consider negotiating with your lenders for a lower interest rate or rate reset.

A successful negotiation can make monthly EMIs more affordable or enable you to repay the home loan sooner.

[Read: How to Reduce Your Home Loan Interest? Here Are 7 Proven Strategies]

For the negotiation to work out in your favour, maintain a good credit score, a strong repayment history, and a positive relationship with your lender.

That said, the final decision to reduce the interest rate is solely at the discretion of the lending institution.

If the negotiation turns out to be unsuccessful, or if you are not satisfied with the new interest rate offered by your lender, you might want to consider a home loan balance transfer.

A balance transfer entails shifting your outstanding loan balance to a different lender that offers a lower interest rate or more favourable loan terms. However, before deciding to make the switch, there are several factors to consider.

For one, transferring a loan often comes with additional costs such as processing fees, administrative charges, and any prepayment penalties with the existing lender.

Any potential savings must outweigh these costs for the home loan balance transfer to be truly beneficial.

Additionally, a balance transfer is most advantageous during the early years of the loan, when the interest component of the EMIs is higher.

If only a few years remain in your tenure, any potential savings might not justify the time, cost, and effort involved in the transfer.

What Should Home Loan Borrowers With a Fixed Rate Do?

With the current expectation of a policy repo rate cut -- provided the CPI inflation continues to moderate -- switching over to a floating rate loan makes sense to benefit from eventual reduced EMIs or repaying the loan sooner than the original tenure.

Floating interest rates loans are set 1 to 3% lower than fixed-rate loans, meaning a switch would save on interest outgo right away.

Note that as per RBI's August 2023 circular, lenders are required to allow borrowers the flexibility to switch from floating-rate loans to fixed-rate loans, and vice versa (subject to applicable charges).

The lenders are required to specify the frequency at which borrowers can exercise the switch option during the loan tenure. They must also transparently communicate the potential effects of benchmark interest rate changes on both the loan and the EMI, allowing borrowers to make informed decisions.

Given the intricate nature of home loans, courtesy of the array of external variables at play, a strategic and thoughtful approach is required.

Your decision-making process should factor in your repayment capacity and opt for a choice that does not adversely impact your financial well-being.

To Conclude...

In recent years, the RBI's repo rate hikes to manage inflation have significantly increased EMIs for home loan borrowers, placing considerable financial pressure on them.

However, a period of relief may be on the horizon if the CPI inflation continues to ease, prompting the RBI to reduce the policy repo rate.

In the meanwhile, borrowers can optimise their loan repayment by negotiating for a lower interest rate, opting for a balance transfer, or switching from a fixed rate loan to a floating-rate loan.

However, each option should be carefully evaluated, taking into account associated charges and their long-term impact on the overall loan cost.

Sound financial planning and informed decision-making are imperative for home loan borrowers to manage the repayment burden effectively.

Happy Planning!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

Hiral Bhuta is a Investment Consultant & Principal Officer. She is a seasoned professional in the financial services industry, currently serving as an Investment Advisor and Financial Planner at PersonalFN. With her expertise, she plays a pivotal role as the Principal Officer appointed under SEBI's amended IA Regulation. Hiral holds distinguished certifications such as Certified Financial Planner (CFP) and NISM XA & XB, complemented by a post-graduate degree in commerce (M. Com). Her primary areas of focus encompass financial planning, investment advisory, and wealth management, where she leverages her knowledge and skills to provide tailored solutions to clients. With a cumulative experience spanning five years, Hiral brings a wealth of expertise and insight to her role at PersonalFN, ensuring clients receive expert guidance and support in navigating their financial goals.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.