Good News for NRIs Investing in Mutual Funds in India

Rounaq Neroy

Apr 22, 2025 / Reading Time: Approx. 6 mins

Listen to Good News for NRIs Investing in Mutual Funds in India

00:00

00:00

India is perceived as a "bright spot" in the global economy and currently is the fastest-growing major economy. For this reason, it is also a promising investment destination.

A lot of Non-Resident Indians (NRIs) who have settled abroad for better career opportunities and other reasons are also investing in India seeing better wealth creation opportunities.

Mutual funds are one of the most sought-after investment options for NRIs. This is because mutual funds are a relatively cost-effective way to diversify the portfolio (rather than investing in individual securities) and offer various categories and sub-categories each with a unique investment mandate.

The NRI investments into mutual funds in India are particularly coming from countries, such as the UAE, Bahrain, Qatar, Singapore, Mauritius, Hong Kong, the U.K., and many others.

The NRIs in the United States of America (USA) and Canada, due to stringent compliance procedures laid down under the FATCA (Foreign Account Tax Compliance Act), however, are required to submit additional documents as well as declarations to begin their investment journey. Currently not many mutual fund houses allow NRIs from the USA and Canada to invest in their schemes.

Tax Important Aspect of Investing

For most NRIs, the tax implications are the most important aspects of investing. In the case of mutual funds, it depends on the type of scheme, i.e. whether equity or debt and the holding period (to ascertain whether Short Term Capital Gain Tax or Long Term Capital Gain Tax) shall apply.

So far, the capital gain tax treatment for investing in mutual funds is as follows:

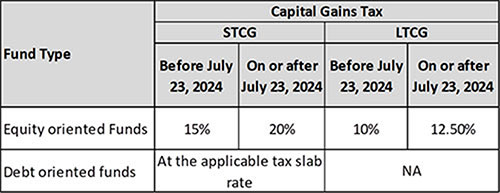

Capital Gains Tax On Equity Mutual Funds for NRIs

(Source: AMFI)

(Source: AMFI)

The Short Term Capital Gain (STCG) on equity-oriented mutual funds (units held for less than 12 months) made at the time of redemption is taxed at 20%, while in the case of non-equity, i.e. debt-oriented mutual funds (units held for less than 36 months), it as per the investor's/assessee's income-tax slab (as per the marginal rate of taxation).

The Long Term Capital Gains on equity-oriented mutual funds (units held for 12 months or more) at the time of redemption, over Rs 1.25 lakh in a financial year, is taxed at 12.5%.

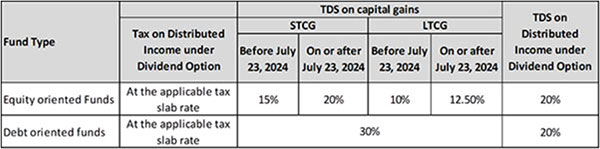

The capital gains are subject to Tax Deduction at Source (TDS) at the time of redemption for NRIs. In the case of equity-oriented funds for STCG earned by NRIs, the TDS rate is 20%, while for LTCG, the TDS rate is 12.5% for NRIs. For debt-oriented funds, the TDS is at 30%.

The Union Budget 2025-26 made no change in the capital tax regime.

TDS Rate Applicable on NRI Investments in Mutual Funds

(Source: AMFI)

(Source: AMFI)

In case you, the NRI, have opted for the IDCW option, the tax on the distributed income (i.e. the dividends) is taxable as per your income tax slab and will be first subject to TDS at 20% or the rate specified under the relevant double tax avoidance agreement, whichever is lower, as per section 196A of the Act.

To prevent the instance of investors having to pay double taxes on incomes arising in one country to a tax resident of another nation, India has signed the Double Taxation Avoidance Treaty (DTAA) with around 90 countries.

Under the DTAA, NRIs can claim tax credits in India on the earnings from their mutual fund units, provided India has signed such an agreement with the resident country of the investor. With the DTAAs in place, it is possible that the realised capital gains on your mutual fund investments would not be taxed in India.

Here's the BIG News...

Recently, the Mumbai Income Tax Appellate Tribunal (ITAT) has ruled that capital gains earned from Indian mutual fund units by NRIs will not be taxed in India. Its decision is based on the India-Singapore Double Taxation Avoidance Agreement (DTAA).

The case in the news is that of one Ms Anushka Sanjay Shah, a Singapore-based NRI. Shah had earned Rs 1.35 crore in short-term capital gains from the sale of equity and debt mutual fund units during the assessment year 2022-23.

She claimed that being a Singapore tax resident, the capital gains should not be taxable in India under the tax treaty between India and Singapore. The Assessing Officer (AO) earlier had rejected this and treated mutual funds units equivalent to shares in Indian companies and taxed the entire amount.

The ITAT asserted that mutual funds in India are created as trusts and not companies under the Securities and Exchange Board of India (SEBI) regulations. The term "share" is not defined in the DTAA, and mutual funds units are not treated as shares under the Companies Act and hence cannot be taxed, it said. The judgment clearly distinguishes between mutual fund units and shares for tax treatment.

The Impact of the ITAT Judgement

The recent judgement of the ITAT in Ms Anushka Sanjay Shah's case makes capital gains from mutual fund investment tax-exempt for NRIs.

It will not only have an impact on NRIs in Singapore investing in India but could also be positive for other non-residents investing in mutual funds in India where the DTAAs are in place, for example, Mauritius, Hong Kong, UAE, Portugal, Australia, France U.K, Germany and many others.

NRIs may be encouraged by this judgement of the ITAT to invest in India, which would result in higher inflows into mutual funds going forward and take the Assets Under Management of the Indian mutual fund industry to a new high.

That being said, it is better to have your Tax Residency Certificate (TRC) to avail of the DTAA benefit. The TRC for the domestic law should not be confused with one available for the DTAA benefit.

Be thoughtful in your approach.

Happy Investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.