5 Banks Offering Lower Home Loan Interest Rates After the RBI Repo Rate Cut

Hiral Bhuta

Mar 01, 2025 / Reading Time: Approx. 7 mins

Listen to 5 Banks Offering Lower Home Loan Interest Rates After the RBI Repo Rate Cut

00:00

00:00

For the past couple of years, home loan borrowers have been burdened with high borrowing costs due to elevated interest rates.

In an effort to control inflation and stimulate economic growth, the Reserve Bank of India (RBI) introduced a series of repo rate hikes between May 2022 and February 2023, resulting in a cumulative increase of 250 basis points.

This resulted in lending institutions raising their interest rates on home loans (and others), leaving borrowers with floating-rate loans to contend with higher Equated Monthly Instalments (EMIs).

Between February 2023 and the December 2024 bi-monthly monetary policy meeting, the RBI maintained the policy repo rate at 6.50%.

However, in the monetary policy review meeting held between February 5 and 7, 2025, the RBI finally announced a cut in the repo rate by 25 basis points, bringing it down to 6.25%. This marks the first rate reduction in nearly five years.

------------------------------------------------------------------------------------

Want to Make Your Money Work While You Sleep?

Talk to Our Investment Advisors Today!

Schedule a First Consultation Call Right Now

------------------------------------------------------------------------------------

One of the key reasons behind this decision was a decline in inflation.

[Read: Will Home Loan Rates Go Down in the New Year 2025? Here's What to Expect]

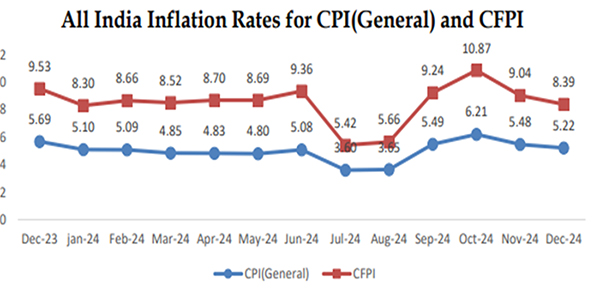

India's Consumer Price Index (CPI) inflation, also known as retail inflation, has been easing since its peak of 6.21% in October 2024, which crossed the RBI's tolerance band of 4-6%.

By January 2025, CPI inflation had moderated to 4.31%, the lowest year-on-year inflation after August 2024. This decline is primarily attributed to a decline in 'food and beverage' inflation (which has a weight of nearly 46% in headline inflation).

As you can see in the graph below, in January 2025, food inflation fell sharply by 237 basis points compared to December 2024, marking its lowest level since August 2024.

Graph: Food Prices Pushing Headline Inflation

Data as of February 12, 2025

Data as of February 12, 2025

(Source: MOSPI)

The RBI's Monetary Policy Committee (MPC) also acknowledged that while economic growth is expected to recover from the low of Q2:2024-25, it is still considerably below that of the last year.

If inflation continues to ease and stays within the RBI's target range, there is a possibility that the central bank may consider another 25 bps cut in the April 2025 bi-monthly monetary policy to support growth.

Transmission of the Repo Rate Cut to the Bank Lending Rates

The repo rate cut has brought relief to a large number of home loan borrowers that opt for floating or variable interest rates in India, owing to their responsiveness to shifts in monetary policy.

The advantage of floating interest rates is that when the RBI lowers the policy repo rate, banks and housing finance companies follow suit by reducing interest rates. This, in turn, benefits borrowers through lower EMIs or slightly earlier repayment of the loan, as the case may be.

While the EMIs would gradually reduce following a repo rate cut, the timing depends on the lender's transmission mechanism.

While some lenders implement rate adjustments promptly, others may take longer.

That being said, several banks have already started passing on the benefits of reduced interest rates.

[Read: Union Budget 2025: Will Home Loan Borrowers Get the Much-Needed Tax Relief?]

Generally, interest rates on home loans in India range from 8.10% to 15.00%, depending on factors such as the bank's internal policies, the loan amount and tenure, and the borrower profile.

Note that fixed-rate home loans are generally set 1 to 3% higher than floating-rate loans.

Below is a table highlighting major banks that have announced interest rate reductions in response to the RBI's repo rate cut:

Table: Revised Home Loan Interest Rates for Major PSU Banks

| Banks |

Earlier Interest Rate (% p.a.) |

Current Interest Rate (% p.a.) |

Rate Cut (bps) |

| State Bank of India |

8.50 |

8.25 |

25 |

| Union Bank of India |

8.35 |

8.10 |

25 |

| Bank of Maharashtra |

8.35 |

8.10 |

25 |

| Bank of Baroda |

8.40 |

8.15 |

25 |

| Canara Bank |

8.40 |

8.15 |

25 |

Interest rates as of Feb 26, 2025

Note: The above list is not exhaustive and not recommendatory

(Source: Websites of respective banks)

If the RBI cuts the repo rate further in April 2025 (subject to continued moderation of the CPI inflation), more banks may follow suit, making home loans even more affordable.

You, as the borrower with a floating-rate home loan, need to monitor the upcoming bi-monthly policy meeting to gauge the direction of interest rates and actively explore lenders offering competitive rates.

Home Loan EMI Calculator

If your bank continues to charge a relatively higher interest rate and negotiations for a lower rate are unsuccessful (which requires a good credit score, strong repayment history, and a positive relationship with the bank), you could consider a home loan balance transfer.

A balance transfer involves moving your outstanding loan to another lender offering a lower interest rate or more favourable terms. With a successful shift, you can benefit from more affordable EMIs or repay the home loan sooner.

However, before making the switch, several factors must be considered.

First of all, loan transfers often come with additional costs, including processing fees, administrative charges, and potential prepayment penalties from the existing lender.

For your transfer to be truly beneficial in the long run, any potential savings must exceed these expenses.

Furthermore, a balance transfer is most effective in the early years of the loan when the interest component of EMIs is higher.

If you only have a few years of tenure remaining, any potential savings might not justify the associated costs, time, and effort.

What Should Fixed Rate Home Loan Borrowers Do?

With banks already reducing interest rates - and the expectation of a further cut - switching to a floating-rate loan to benefit from reduced EMIs or repaying the loan sooner could be a prudent move.

As per the RBI's August 2023 circular, lenders are required to give borrowers the flexibility to switch between floating and fixed-rate loans, subject to applicable charges.

Lenders are also required to specify how often borrowers can exercise this option during the loan tenure. Additionally, they must transparently convey the potential impact of benchmark interest rate changes on both the loan and the EMI, so that borrowers can make informed decisions.

A thoughtful and strategic approach is required as multiple external factors influence floating-rate home loans.

When making a decision, you should consider your ability to repay and choose a course of action that won't negatively affect your financial well-being.

To Conclude...

The RBI's recent repo rate cut and subsequent reductions in home loan interest rates by several major banks have provided much-needed relief to borrowers dealing with high borrowing costs.

You, as an existing borrower, should proactively optimise your home loan by negotiating with your bank for a lower interest rate, switching to another bank offering a lower rate, or switching from a fixed-rate to a floating-rate loan.

Whichever option you choose should be carefully evaluated for the associated costs and the long-term impact on your financial health.

Be thoughtful in your approach.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

Hiral Bhuta is a Investment Consultant & Principal Officer. She is a seasoned professional in the financial services industry, currently serving as an Investment Advisor and Financial Planner at PersonalFN. With her expertise, she plays a pivotal role as the Principal Officer appointed under SEBI's amended IA Regulation. Hiral holds distinguished certifications such as Certified Financial Planner (CFP) and NISM XA & XB, complemented by a post-graduate degree in commerce (M. Com). Her primary areas of focus encompass financial planning, investment advisory, and wealth management, where she leverages her knowledge and skills to provide tailored solutions to clients. With a cumulative experience spanning five years, Hiral brings a wealth of expertise and insight to her role at PersonalFN, ensuring clients receive expert guidance and support in navigating their financial goals.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.