What Do Long-Term Bond Yields Say About Path to Interest Rates

Rounaq Neroy

Apr 25, 2025 / Reading Time: Approx. 11 mins

Listen to What Do Long-Term Bond Yields Say About Path to Interest Rates

00:00

00:00

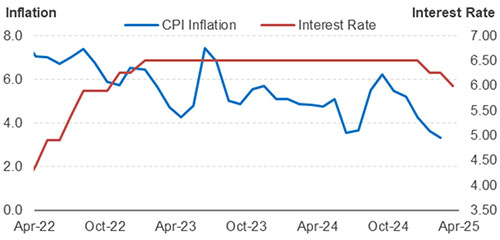

In CY2025, the Reserve Bank of India (RBI) has thus far cut the policy rate by 50 basis points (bps) - 25 bps in February and another 25 bps in April. The policy repo rate currently is 6.00%.

The successive easing of CPI inflation -- well within the target of 4.00% with a band of +/- 2.00% and greater confidence of it remaining in this range over a 12-month horizon (due to lower food prices) --has nudged the central bank to cut rates to support growth.

CPI Inflation v/s Interest Rates

Data as of April 15, 2025

Data as of April 15, 2025

(Source: MOSPI, RBI Monetary Policy Statements)

Moreover, challenging global economic conditions and a moderate growth outlook have demanded that the six-member MPC vote in favour of rate cuts to support growth.

Table: Voting on the Resolution to Reduce the Policy Repo Rate to 6.00%

(Source: Minutes of the Bi-Monthly Monetary Policy Committee Meeting, April 7 to 9, 2025)

(Source: Minutes of the Bi-Monthly Monetary Policy Committee Meeting, April 7 to 9, 2025)

In the last bi-monthly monetary policy meeting held in April 2025, the MPC also decided to change the stance of monetary policy from 'neutral' to 'accommodative'.

However, the MPC noted that the rapidly evolving situation requires continuous monitoring and assessment of the economic outlook.

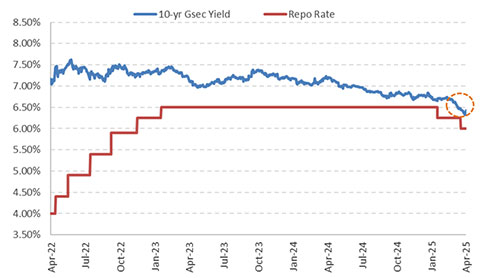

The Impact on Bond Markets

Now, those who are investing in the Indian debt market may know that interest rates and bond yields are directly related to each other.

Tracking interest rates, the long-term bond yields in the Indian debt market have also softened in the past couple of months.

The Benchmark 10-Year G-Sec Yield Has Softened

Data as of April 23, 2025

Data as of April 23, 2025

(Source: Investing.com, data collated by PersonalFN Research)

Since the February 2025 bi-monthly monetary, as the RBI cut the policy repo rate for the first time since the COVID-19 pandemic, India's 10-year G-sec yield has softened by a good 27 bps.

On a year-to-date (YTD) the reduction in benchmark yield is 35 bps. In April 2025 itself, the benchmark G-sec yield has eased by a decent 15 bps so far to 6.43% (as of April 23, 2024).

The yield of the 40-year 2064 bond is also down 7 bps since the start of April 2025 to 6.78% (as of April 23, 2024).

Even the yields of the medium tenor bonds of 3-year (maturing in 2028) and 5-year (maturing in 2030) have fallen by 28 bps and 22 bps to 6.04% and 6.12%, respectively (as of April 23, 2024).

Currently, bond yields in the Indian debt market are at a 3-year low with positive FPI flows in the Indian debt market.

The inclusion of Indian bonds in JPMorgan's emerging market debt index and RBI's timely liquidity infusion into the system in the recent past have also helped. Besides benign headline inflation outlook, and thus rate cut expectations, have proved abetting.

The fall in bond yields has augured well for the Indian debt market, as bond prices and yields are inversely related to each other. Simply put, when yields move down, bond prices go up and vice versa.

The current scenario is proving favourable for debt mutual funds, particularly the ones holding longer-maturity debt papers such as Medium to Long Duration Debt Funds, Long Duration Funds, and Gilt Funds.

Path to Interest Rates

The RBI has observed that there is a decisive improvement in the inflation outlook. CPI inflation is currently well below the target, supported by a sharp fall in food inflation. Now there is greater confidence of a durable alignment of headline inflation with the target of 4.00% over a 12-month horizon.

What is more, is that impeded by a challenging global environment and uncertainty remaining high, the MPC is of the view of supporting growth.

In the minutes of the last Monetary Policy Committee Meeting, April 7 to 9, 2025, RBI Governor, Mr Sanjay Malhotra states:

"The global economic landscape remains in a state of flux amidst heightened trade and policy uncertainties, with attendant implications for economies across the world, posing complex challenges and trade-offs in policy making.

The channels through which these global shocks could impact economies, particularly emerging market economies, include spillovers from global growth slowdown, elevated financial market volatility and dented consumer and investor confidence. The Indian economy remains relatively less exposed and better placed to withstand such spillovers with its growth driven largely by domestic demand. Nevertheless, we are not immune to the aftershocks and ripple effects associated with global disturbances."

As regards inflation, Governor Malhotra writes:

"There is now greater clarity on the food inflation outlook as the uncertainties related to rabi crops production have abated.

Core inflation (excluding fuel and food), although inching up to 4.1 per cent in February 2025 from 3.6 per cent in January, continues to be around the 4 per cent mark, suggesting that underlying inflationary impulses in the economy are benign and well-anchored.

Moreover, the decline in crude oil prices should impart a softening bias to the inflation outlook.

Coming to the imposition of tariffs, in my view, the implications for inflation are two-sided. On the upside, uncertainties may lead to possible currency pressures resulting in imported inflation. On the downside, slowdown in global growth will further soften commodity and crude oil prices, which would ease the pressure on inflation.

Overall, favourable factors for the inflation outlook outweigh those with possible adverse impact and should drive further disinflation in the headline CPI. It is expected that inflation will be well aligned to the target during the current financial year."

He has also expressed that going forward, considering the evolving growth-inflation trajectories, monetary policy needs to be accommodative.

Against the backdrop of the above and the fact all six members are on the same page as regards policy rates and accommodative stance, plus so far inflation is well within RBI's target, it is possible that the RBI would cut the policy repo rates by another 25 bps in the MPC next meeting in June (scheduled from June 4 to 6, 2025).

An additional policy repo rate cut would prove supportive for growth. It would nurture domestic demand, push private consumption and improve the growth momentum -- a critical aspect when the global uncertainties have amplified downside risk to growth.

Investment Strategy to Follow Now When Investing in Debt Instruments

Those preferring bank Fixed Deposits (FDs) for stable/fixed returns to manage their cash flow needs, such as risk-averse investors and retirees, should go ahead and invest now before interest rates on deposits go down further in time.

To maximise the returns on the bank FD, consider following the laddering strategy whereby you can maximise returns and take care of your liquidity needs.

Coming to investment in debt mutual funds, you need to be selective of the subcategories. As bond yields have dropped and the policy repo rate may be cut further, it would be meaningful to invest in Medium-to-Long Duration Debt Mutual Funds is expected to increase.

That said, keep in mind that Medium-to-Long Duration Debt Funds are moderate-to-high-risk contenders. This is due to the interest rate sensitivity of these funds, as well as the fact that there is a slight credit risk. The higher the modified duration of the scheme, the higher will be its sensitivity to interest rates.

To take a calculated risk, make sure the maturity profile of the scheme you zero in on is up to 5 years or so with G-secs making up around 30%. For this, evaluate the portfolio characteristics of the scheme and check the investment processes and systems followed at the fund house.

You may allocate around 25% of your debt mutual fund portfolio to some of the best Medium-to-Long Duration Debt Funds, keeping an investment horizon of 3 to 5 years.

To play the interest rate cycle dynamically to short and medium-to-long maturity debt papers, some of the best Dynamic Bond Funds can be a meaningful choice, provided you have an investment horizon of 3 to 5 years.

Regardless of the direction in which interest rates move, Dynamic Bond Funds are capable of taking advantage of dynamic market conditions and can invest accordingly to create an all-season portfolio that generates optimal returns. Nevertheless, it is critical to invest in Dynamic Bond Funds that hold a robust portfolio of securities across maturities and high-quality debt & money market instruments.

Around 25% of your debt mutual fund portfolio could be allocated to some of the best Dynamic Bond Funds.

Similarly, investing in some of the best Banking & PSU Debt Funds can be a good alternative if you have an investment time horizon of around 2 to 3 years.

Banking & PSU Debt Funds have exposure to debt papers across the yield curve but typically maintain a duration of around 3 to 5 years. Banking & PSU Debt Funds are mandated to invest predominantly (80% of their assets) in top-rated corporate debt instruments issued by Banks, Public Sector Undertaking (PSUs), Public Financial Institutions (PFIs), Municipal bonds, and other such securities. These entities are recognised for their robust credibility and liquidity compared to those from private issuers, making them a relatively safer investment option.

Around 25% of your debt mutual fund portfolio could be allocated to some of the best Banking & PSU Debt Funds.

For a shorter investment horizon of up to a year or so, it would be better to stick to some of the best Liquid Funds having the least or no exposure to private issuers.

Ideally, you would be better off with Liquid Funds that invest predominantly in Government securities (G-Secs), quasi-government securities, AAA/A1+ rated Public Sector Undertakings (PSU) debt, and T-bills, where there is no private corporate credit risk, the portfolio is highly liquid, it is marked-to-market daily (whereby the declared NAV is real), the AUM trend is stable, and the portfolio is disclosed regularly.

Investing in some of the best Liquid Funds with portfolio characteristics and is true its label is a sensible way to hold some money safe, whereby it can offer you liquidity, help address unforeseen circumstances, and meet short-term financial goals.

Words of Caution When Investing Debt Funds

Debt funds, in general, are not risk-free, and hence choosing the safety of the principal over returns is imperative. It is unlike investing in a bank FD, where you earn fixed and stable returns, plus deposits as covered by the DICGC for up to Rs 5 lakh per bank.

Avoid debt funds that compromise on the portfolio characteristics and engage in yield hunting to clock higher returns.

To sum up...

Falling yields would prove favourable for bonds and the NAV of debt mutual funds, particularly Medium-to-Long Duration Debt Funds, Long Duration Debt Funds and Gilt Funds.

If you follow a sensible approach to select respective schemes within these subcategories of debt funds it can be a rewarding experience.

Don't just go by the past returns as they are not necessarily indicative of the future. Instead check the portfolio characteristics, the risk ratios, and investment processes and systems followed at the mutual fund house to make a prudent choice.

Also, make sure to choose debt mutual fund schemes that align well with your personal risk profile, investment objective, and investment horizon. Follow a sensible asset allocation model.

Be a thoughtful investor.

Happy Investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.