RBI Keeps Repo Rate Steady at 6.50%. What Are the Implications for Home Loan Borrowers

Rounaq Neroy

Dec 17, 2024 / Reading Time: Approx. 8 mins

Listen to RBI Keeps Repo Rate Steady at 6.50%. What Are the Implications for Home Loan Borrowers

00:00

00:00

The six-member Monetary Policy Committee (MPC) of the RBI decided to keep the policy repo rate unchanged at 6.50% during the last bi-monthly monetary policy meeting on December 6, 2024.

As a result, the Standing Deposit Facility (SDF) rate has been maintained at 6.25%, while the Marginal Standing Facility (MSF) rate and the Bank Rate remain steady at 6.75%.

Notably, the Cash Reserve Ratio (CRR) was lowered by 50 basis points (bps) to 4.00% to ease the potential liquidity stress, injecting Rs 1.16 lakh crore into the banking system.

The decision was made by a 4:2 majority, after a detailed assessment of the current and evolving macroeconomic situation, financial developments, and outlook. The meeting marks the 11th consecutive time that the RBI has kept the repo rate unchanged.

Additionally, the MPC took a unanimous decision to continue with the 'neutral' monetary policy stance and to maintain an unambiguous focus on the durable alignment of inflation with the target, while supporting growth.

One of the main reasons behind keeping the repo rate unchanged yet again was the persistent high inflation. India's CPI inflation (also known as retail inflation) hit a 14-month high in October 2024, rising to 6.21% from 5.49% in September 2024, breaching the RBI's tolerance threshold of 6%. The inflation spike was largely attributed to higher food prices.

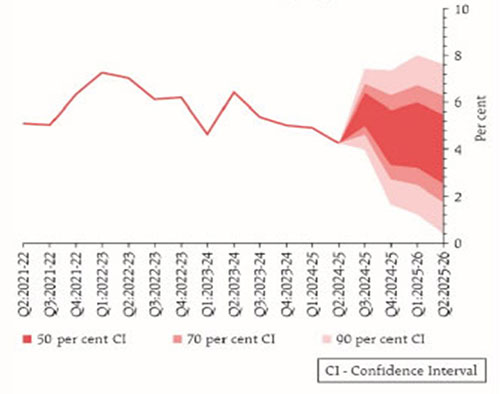

Graph: RBI's Quarterly Projection of CPI

(Source: RBI’s Bi-monthly Monetary Policy Statement, December 4 to 6, 2024)

(Source: RBI’s Bi-monthly Monetary Policy Statement, December 4 to 6, 2024)

According to the RBI, food inflation is likely to start easing from Q4 of 2024-25, owing to the seasonal corrections in vegetable prices, kharif harvest arrivals, likely good rabi output, and adequate cereal buffer stocks.

However, adverse weather conditions and the increase in the prices of international agricultural commodities pose an upside risk to food inflation. While energy prices have subsided recently, according to the RBI, their sustenance requires monitoring. Plus, businesses anticipate input cost pressures to remain elevated and expect the selling price growth to pick up momentum from Q4.

Considering all these factors, the RBI has projected the CPI inflation for 2024-25 at 4.8%, with estimates for Q3 at 5.7% and Q4 at 4.5%.

For the first two quarters of 2025-26, CPI inflation is expected to be 4.6% and 4.0% respectively (see the Graph). The risks remain evenly balanced.

In his statement, the former RBI Governor Shaktikanta Das (whose tenure concluded on December 10, 2024), said, "The MPC believes that only with durable price stability can strong foundations be secured for high growth. The MPC remains committed to restoring the inflation growth balance in the overall interest of the economy."

[Read: RBI Holds Repo Rate at 6.50% Again. Here's Why You Should Invest in Bank FDs Now]

The Path Forward

The latest CPI inflation data for November 2024 has eased to 5.48% from 6.21% in October 2024 abetted by a reduction in the 'food and beverage' inflation (which has a weight of nearly 46% in headline inflation). The price of Fruits and vegetables, in particular, have witnessed a decrease with the arrival of fresh harvests. Thus, the Consumer Food Price Inflation (CFPI) reading for November 2024 came in lower at 9.04% versus 10.87% in the previous month.

Going forward, inflationary pressures in the food basket are expected to ease in the coming months. That being said, it would be important to monitor the global developments amidst the geopolitical tensions, as they could have a significant influence on global commodity prices and thus 'imported inflation'. It would be crucial on the part of RBI to keep a watch on food prices in particular, as it directly impacts household budgets.

The MPC remains committed to its goal of restoring the balance between inflation and growth in the broader interest of the economy.

The RBI's decision to maintain a neutral stance on monetary policy provides the flexibility to adapt to evolving conditions, particularly as new data on inflation and GDP growth emerge.

The newly appointed RBI Governor, Sanjay Malhotra, who assumed office on December 11, 2024, emphasised the importance of stability and continuity in policy. He remarked, "Stability in policy and continuity is very important. Decisions will be taken with public interest to preserve trust in this institution."

What Does the RBI's Decision Mean for Home Loan Borrowers

The RBI raised the repo rate by 250 basis points between May 2022 and February 2023, in an effort to control inflation. As a result, lending institutions increased their interest rates, causing a surge in EMIs for borrowers.

At present, the RBI's decision to keep the repo rate unchanged has left home loan borrowers coping with elevated interest rates or borrowing costs for the time being.

Should inflation continue to moderate, the RBI may consider lowering rates in the future, potentially in the February 2025 or April 2025-26 bi-monthly monetary policy statement. This would bring a period of relief to home loan borrowers.

In India, a large number of borrowers opt for floating or variable interest rates, owing to their responsiveness to monetary policy shifts.

Thus, borrowers with floating interest rates could benefit from reduced Equated Monthly Instalments (EMIs) or have the advantage of their loan repayment done sooner than the tenure they originally opted for, provided CPI inflation continues to moderate, and nudges the central bank to reduce the policy repo rate. Lower borrowing rates on home loans, could significantly ease the repayment burden for existing borrowers and increase demand from new borrowers.

In the current environment, where the EMIs and interest rates are likely to remain stable for a couple of months, borrowers should take the opportunity to do the following:

1. Prepay When Possible

If your budget permits or you receive surplus funds (e.g., bonuses), consider making additional payments beyond the required EMI.

Prepayments reduce the principal amount, thereby lowering total interest costs over time. Many banks allow prepayments without penalties up to a certain limit.

2. Negotiate with Lenders

If you have a strong repayment history, good creditworthiness, and a positive relationship with your lender, consider negotiating for a lower interest rate or better repayment terms.

A successful negotiation can make monthly payments more manageable and alleviate the overall interest burden.

However, keep in mind that the decision to reduce interest rates rests solely with the lending institution. Be prepared with a strong case to increase the chances of the negotiation working out in your favour.

3. Consider a Home Loan Balance Transfer

While the repo rate sets the broad direction for interest rates in the economy, individual banks set their rates based on factors like cost of funds acquisition, risks, and strategic objectives. This results in rate variations across lenders.

Take a look at the current borrowing rates in the market...

Table 1: PSU Bank Home Loan Interest Rates

| Banks |

Interest Rate (% p.a.) |

| State Bank of India |

8.50 to 9.65 |

| Bank of Baroda |

8.40 to 10.60 |

| Indian Overseas Bank |

8.40 to 10.60 |

| Canara Bank |

8.40 to 11.75 |

| Union Bank of India |

8.35 to 10.75 |

Interest rates as of Dec 16, 2024

Note: The above list is not exhaustive and not recommendatory

(Source: Websites of respective housing finance companies)

Table 2: Private Bank Home Loan Interest Rates

| Banks |

Interest Rate (% p.a.) |

| HDFC Bank |

8.75 to 9.95 |

| ICICI Bank |

8.75 to 11.45 |

| Axis Bank |

8.75 to 14.00 |

| Kotak Mahindra Bank |

8.75 onwards |

| Yes Bank |

9.00 to 12.00 |

Interest rates as of Dec 16, 2024

Note: The above list is not exhaustive and not recommendatory

(Source: Websites of respective housing finance companies)

Table 3: Housing Finance Companies Home Loan Interest Rates

| Banks |

Interest Rate (% p.a.) |

| LIC Housing Finance |

8.50 onwards |

| Bajaj Housing Finance |

8.50 to 17.00 |

| Tata Capital |

8.75 onwards |

| PNB Housing Finance |

8.50 to 14.75 |

| Aditya Birla Capital |

8.60 to 20.00 |

Interest rates as of Dec 16, 2024

Note: The above list is not exhaustive and not recommendatory

(Source: Websites of respective housing finance companies)

If your current interest rate is significantly higher than the market average, you may want to consider a home loan balance transfer. This involves transferring the outstanding balance of your home loan to another lender offering lower interest rates or better loan terms.

However, keep in mind that a balance transfer may come with additional costs, such as processing fees and administrative charges, which can add to the overall cost of borrowing.

For the transfer to be beneficial in the long run, the potential savings must outweigh the cost of the transfer.

Additionally, it should be noted that a transfer tends to be more advantageous during the early stages of your loan tenure when the interest component of your EMIs is higher.

To Conclude...

For home loan borrowers, the RBI's decision to keep the repo rate unchanged at 6.50% for now translates to stable but elevated EMIs resulting from earlier rate hikes.

Borrowers can use this period to reassess their loan repayment strategies, such as prepaying to reduce the interest burden or considering a balance transfer to a lender with lower rates. However, each option should be carefully weighed against the costs associated.

Prudent financial planning and informed decision-making will remain key for home loan borrowers to manage their repayment burden effectively.

Happy planning!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.