Why Now Is An Opportune Time to Invest in Bank FDs For the Stability of Your Portfolio

Rounaq Neroy

Apr 01, 2025 / Reading Time: Approx. 8 mins

Listen to Why Now Is An Opportune Time to Invest in Bank FDs For the Stability of Your Portfolio

00:00

00:00

The Indian equity market has been rather volatile in the last couple of months, with the benchmark indices experiencing steep declines. While the market has finally staged a remarkable rebound in March 2025 (gaining nearly 6%), it would be imprudent to be complacent and think that markets have bottomed out.

The U.S. President Donald Trump's announcement of reciprocal tariffs, set to come into effect from April 2, 2025, and applying to "all countries" without exception, is likely to continue contributing to market volatility.

In addition, the other global and domestic headwinds, such as persistent geopolitical tensions, Israel's expansion of the Gaza war, the ongoing Russia-Ukraine war, rising crude oil prices, chances of geoeconomic fragmentation and the possibility of an economic slowdown, are keeping the Indian equity markets on edge.

During such uncertain times, strategic asset allocation and diversification are going to be crucial. A tactical exposure to bank Fixed Deposits (FDs) within debt as an asset class would prove to be a prudent move to navigate market volatility, benefit from an assured rate of return, and add a layer of stability to your, the investor's, portfolio.

Why Is Now an Opportune Time to Invest in Bank FDs?

In February 2025, the Reserve Bank of India (RBI) cut the repo rate for the first time in nearly 5 years.

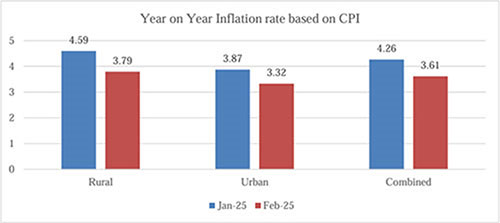

One of the key factors behind this decision was the easing of the Consumer Price Index (CPI) inflation, also known as retail inflation, to 4.31% by January 2025 from its peak of 6.21% in October 2024. Now, in February 2025, the CPI has further declined to 3.61%, reflecting the lowest year-on-year inflation after July 2024.

Graph: CPI Inflation Has Cooled Off

Data as of February 12, 2025

Data as of February 12, 2025

(Source: MOSPI)

With the inflationary pressure easing, it is anticipated that the RBI will cut the repo rate by another 25 basis points (bps) in the upcoming April 2025 bi-monthly monetary policy.

If this indeed happens, banks would be nudged to lower their deposit rates in response, impacting the returns for depositors. Thus, investing in bank FDs now can help you, the investor, to lock in at the current interest rates and potentially secure better returns before the policy repo rate cut is announced by the RBI in its April 2025 bi-monthly monetary policy statement.

Here's Why You Shouldn't Overlook Bank FDs in the Current Scenario

1. Guaranteed Fixed Interest

Unlike market-linked investments like equity mutual funds, which are susceptible to market swings, FDs offer fixed-interest earnings over a pre-determined period. This predictability allows investors to plan their financial goals with greater certainty with the assurance of steady returns regardless of external market conditions.

2. Capital Protection

Market-linked investments are integral to long-term wealth creation, however, capital protection is a crucial concern during times of economic uncertainties. Holding a certain amount in a bank FD is akin to keeping some money in cash.

Currently, amid uncertainty and mixed economic signals, even legendary investor, Warren Buffett is sitting on a record-breaking USD 334 billion in cash and short-term investments. Buffett has timely taken tactical held cash and cash equivalent avenues - whether it was the Dotcom Bubble of the early 2000s, the Global Financial Crisis (GFC) of 2008, or the COVID-19 pandemic crash. This is guided by his philosophy: "Be Fearful When Others Are Greedy and Greedy When Others Are Fearful"

While the Indian equity market gained noticeably in March 2025, downturns cannot be ignored - and they could erode your wealth.

On the other hand, hard-earned money parked in FDs may help preserve capital, making them a reliable choice, particularly for risk-averse investors whose priority is the safety of principal over returns.

3. DICGC Protection

Deposits held in commercial banks and small finance banks are also backed by the Deposit Insurance Credit Guarantee Corporation (DICGC). In the event of a bank's failure, it provides insurance coverage of up to Rs 5 lakh per depositor per bank, adding another layer of safety.

Recent media reports have suggested that the government is actively considering nearly doubling the existing insurance limit. This shall provide greater financial security, especially for retirees who usually park a higher part of their savings into bank fixed deposits.

Strategically the DICGC protection can further be maximised by spreading your deposits across multiple banks, with combinations of different rights and capacities (such as joint accounts with your spouse, children, or siblings), instead of locking all your funds in a single bank FD.

4. Cumulative and Interest Payout Options

Bank FDs come with different plans: cumulative and non-cumulative. The non-cumulative plan offers interest pay-out options such as monthly, quarterly, half-yearly or annually for you to choose from depending on your liquidity needs. You can choose the tenure options (typically ranging from 7 days to 10 years) as per your requirements.

For example, to address a short-term financial goal could consider the cumulative (also known as the reinvestment option). Conversely, if you are seeking regular income by way of interest payouts, you may consider monthly or quarterly interest payout options.

Why Are Bank FDs Suitable for Addressing Short-Term Financial Goals and Contingency Needs?

Parking funds in a bank FD provides sufficient liquidity to quickly access cash when you need it with little or no penalty for early withdrawals.

If you're saving for shorter-term goals, such as a vacation or saving for home renovation, FDs are a relatively safer and more convenient option to ensure that funds are available to you without exposing your hard-earned savings to equity market volatility.

Likewise, having around 6 to 18 months of regular monthly expenses, including EMIs, in a couple of bank FDs (in suitable tenure options) can ensure you have the money accessible instead of having to borrow from someone.

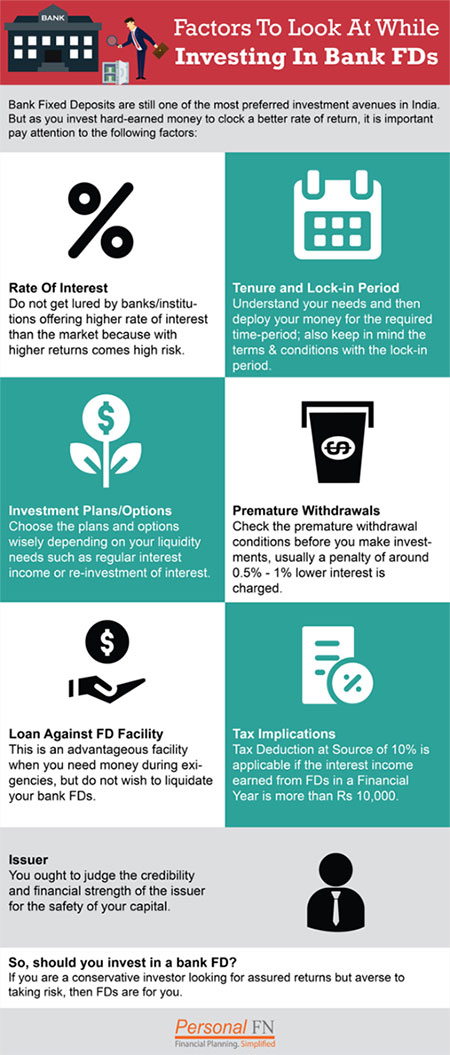

What Are the Factors to Consider When Investing in Bank FDs?

Well, here are some facets you should look at:

1. Bank's Reputation and Credibility

Choose banks with a strong market presence and reputation. Well-established banks, especially those classified as systemically important, are expected to have credible management and follow robust processes.

Be wary of banks offering exceptionally high interest rates on term deposits, as it also means that the investment risk involved is high.

2. Premature Withdrawals

Pay heed to lock-in periods, as premature withdrawals may incur penalties. It's a good practice to check penalty charges before investing to make informed investment decisions.

Follow the Laddering Strategy When Investing in Bank FDs

Fixed Deposit laddering is a smart strategy wherein you spread your FD investments across multiple maturity tenures or maturity buckets (e.g. 6 months, 1 year, 2 years) rather than locking all your funds in a single FD.

It offers you the financial flexibility to access money at regular intervals without breaking long-term deposits prematurely.

When each FD in the ladder matures at the specified interval, you'll have the maturity proceeds available to use (for whatever purpose). The maturing FDs can be reinvested at higher yields if interest rates improve in the future, paving the way for better returns over time.

What Are the Tax Implications?

Interest earned on bank FDs is taxable under the head "Income from Other Sources" and is taxed according to your applicable income tax slab.

Banks deduct TDS at 10% in cases where the total interest earned in a financial year exceeds Rs 50,000 (Rs 1 lakh in the case of senior citizens). If a PAN has not been provided, TDS will be deducted at 20%.

If your income falls below the taxable limit, submit Form 15G (for non-senior citizens) or Form 15H (for senior citizens) to your bank at the beginning of the financial year to prevent TDS deductions.

To Conclude...

Given the current equity market volatility, you cannot afford to overlook bank FDs as a part of a well-diversified portfolio. As a repo rate cut from the RBI also seems likely in the upcoming April 2025 bi-monthly monetary policy, it makes sense to lock in the current FD interest rates now.

A smart approach, such as the FD laddering strategy, would help optimise returns and reduce concentration risk by investing across different banks and different maturity buckets.

Be a thoughtful investor.

Happy investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.