Can Small Cap Funds Deliver Big Returns Going Forward?

Rounaq Neroy

Feb 20, 2024 / Reading Time: Approx. 10 mins

Listen to Can Small Cap Funds Deliver Big Returns Going Forward?

00:00

00:00

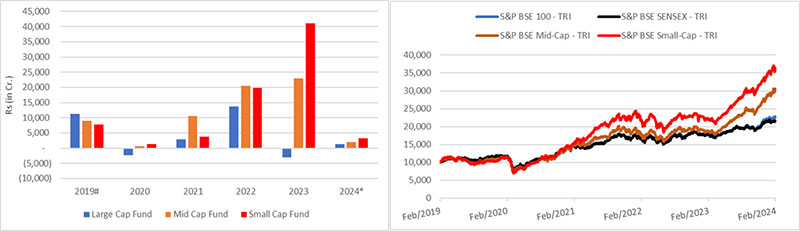

The fascination of investors in India for small caps seems to be unending. The optimism about India's economic prospects, smaller companies participating in India's growth story, the remarkable outperformance of the small-cap indices, the kind of returns generated, and increased investor awareness are some of the key factors behind the inflows into Small Cap Mutual Funds.

As seen in the graph below, the Small and Mid Cap Funds have witnessed higher cumulative net inflows than the Large Cap Funds in the last few years.

Graph 1A and 1B: Small Cap Funds Sparked Interest as Smallcap Index Clocked High Returns

Data as of February 16, 2024

Data as of February 16, 2024

In the case of inflows in sub-categories of equity funds, the segment-wise data reported by AMFI is from April 2019 onwards.

For the Indices graph, the base is taken as Rs 10,000

(Source: ACE MF, data collated by PersonalFN Research)

These inflows have come in even against the backdrop of the COVID-19 pandemic, looming geopolitical tensions, various macroeconomic factors in play, elevated valuations, and volatile equity markets. Perhaps investors are excited by the returns clocked by the small cap index but are disregarding the risks.

Table 1: Small Cap Funds Before Lehman Bros. Collapse and Now

| Particulars |

Mar-08 |

Jan-24 |

No. of Times |

| Total No. of Small Cap Funds |

7 |

18 |

2.6 |

| Total No. of Equity Funds |

172 |

674 |

3.9 |

| Small Cap Funds AUM (Rs in Cr.) |

2,524 |

222,512 |

88.2 |

| Total Equity Funds AUM (Rs in Cr.) |

122,116 |

2,815,465 |

23.1 |

(Source: ACE MF, data collated by PersonalFN Research)

In March 2008, a few months before the Lehman Brothers -- the U.S.'s fourth-largest investment bank founded in 1850 -- collapsed, the Indian equity market landscape had a total of 7 equity funds with AUM of around Rs 2,500 crore.

But nearly a decade later, when the capital market regulator, SEBI, came up with strict mutual fund categorisation and rationalisation norms (so that it become easier for investors to identify mutual funds), several schemes existing schemes having exposure to micro caps as well as combining mid and small caps were merged and/or rechristened as small caps, and the count of Small Cap Funds went up.

Besides, mutual fund houses, which didn't have an independent small cap fund in their product basket, launched New Fund Offers (NFOs) capitalising on the market sentiments. As a result, the number of Small Cap Funds more than doubled from March 2008, and the combined Small Cap Fund AUM today is Rs 28.15 trillion.

Speaking of the performance of Small Cap Funds, the category average returns over a longer period showed an outperformance vis-a-vis the small cap indices. However, the table below shows that not all Small Cap Funds have been able to deliver appealing returns.

Table 2: Performance of Small Cap Funds

| Category |

Absolute (%) |

CAGR (%) |

Risk ratios |

| 1 Year |

3 Years |

5 Years |

7 Years |

SD Annualised |

Sharpe |

Sortino |

| Top performer |

35.73 |

53.82 |

33.17 |

23.58 |

21.55 |

0.50 |

0.99 |

| Bottom performer |

12.11 |

27.49 |

12.18 |

13.23 |

17.84 |

0.32 |

0.60 |

| Category average |

25.93 |

37.72 |

22.92 |

19.00 |

16.55 |

0.44 |

0.90 |

| No. of schemes outperformed |

10 |

13 |

18 |

12 |

-- |

-- |

-- |

| No. of schemes underperformed |

14 |

9 |

1 |

1 |

-- |

-- |

-- |

| Nifty Smallcap 250 - TRI |

27.56 |

35.88 |

15.97 |

14.99 |

19.12 |

0.38 |

0.72 |

| S&P BSE 250 Small Cap - TRI |

28.21 |

35.75 |

15.86 |

15.47 |

19.32 |

0.39 |

0.73 |

Data as of February 16, 2024

The list of funds cited here is not exhaustive.

Returns expressed are rolling returns in %. calculated using the Direct Plan-Growth option.

Standard Deviation indicates Total Risk and Sharpe Ratio measures the Risk-Adjusted Return. They are calculated over 3 years assuming a risk-free rate of 6% p.a.

Past performance is not an indicator of future returns.*Please note, that this table represents past performance.

The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

(Source: ACE MF, data collated by PersonalFN Research)

The gap or the difference between the top performing Small Cap Fund and the bottom Performing Small Cap Fund is quite noticeable.

Also, not all Small Cap Funds have managed their risk well when managing the returns. For this reason, it becomes important to select Small Cap Funds prudently before adding them to your investment portfolio.

[Read: 5 Best Small Cap Funds for 2024]

Table 3: Performance of Small Cap Funds During the Bear Phase of Global Financial Crisis and the Ensuing Bull Phase

| Particulars |

Bear phase |

Bull phase |

| 08-Jan-08 To 09-Mar-09 |

09-Mar-09 To 05-Nov-10 |

| Small Cap |

Top performer |

-8.69 |

143.55 |

| Bottom performer |

-68.67 |

37.15 |

| Category average |

-54.42 |

96.09 |

| Nifty Smallcap 250 - TRI |

|

-69.31 |

115.17 |

| S&P BSE 250 Small Cap - TRI |

|

-- |

134.00 |

Returns expressed are point-to-point in %. calculated using the Direct Plan-Growth option.

Returns over 1-year are compounded annualised.

Past performance is not an indicator of future returns.*Please note, that this table represents past performance.

The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

(Source: ACE MF, data collated by PersonalFN Research)

The table above shows that during the bear phase of the Indian equity markets in 2008-09 due to the Global Financial Crisis, the average returns of Small Cap Funds plunged. Moreover, there was a noticeable difference between the returns of the top performer and the bottom performer.

Table 4: Performance of Small Cap Funds During the Bear Phase of the COVID-19 Pandemic and the Ensuing Bull Phase

| Particulars |

Bear phase |

Bull phase |

| 14-Jan-20 To 23-Mar-20 |

23-Mar-20 To Till Date |

| Small Cap |

Top performer |

-23.98 |

74.52 |

| Bottom performer |

-40.53 |

42.49 |

| Category average |

-34.37 |

50.08 |

| Nifty Smallcap 250 - TRI |

|

-41.47 |

52.56 |

| S&P BSE 250 Small Cap - TRI |

|

-41.24 |

51.54 |

Returns expressed are point-to-point in %. calculated using the Direct Plan-Growth option.

Returns over 1-year are compounded annualised.

Past performance is not an indicator of future returns.*Please note, that this table represents past performance.

The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

(Source: ACE MF, data collated by PersonalFN Research)

Similarly in the brief setback of the COVID-19 pandemic from January 14, 2020, to March 23, 2020, as shown in Table 4, Small Cap Funds, on an average, generated negative returns. Moreover, there was a stark contrast between the returns of the top and bottom performing Small Cap Fund.

In the current bull market rallies since the March 2020 lows of the COVID-19 pandemic, the Small Cap Funds have undoubtedly delivered stellar returns. However, the performance of Small Cap Funds during the bear phases of the Indian equity markets underlines the need to select Small Cap Funds carefully.

Keep in mind that among the various sub-categories of equity mutual funds, the risk of investing in Small Cap Funds is very high. They find their place at the very high end of the risk-return spectrum.

This is because Small Cap Funds, by definition, are mandated to invest at least 65% of their assets in equity and equity-related instruments of small-cap companies, i.e. the ones beyond 250 on a full market capitalisation basis. Usually, these companies have a market cap of less than Rs 5,000 crore and could be less liquid. In other words, investing in small caps is a very high-risk-high-return investment proposition.

The question then arises: Does It Still Makes Sense to Invest in Small Cap Funds in 2024?

In the past, small caps have outperformed and exceeded the returns expectations. Whether it would clock attractive returns in 2024 cannot be said with the most certainty.

At present, India is the most expensive emerging equity market. The Morgan Stanley Capital International (MSCI) India Index Price-to-Equity (P/E/) ratio is over 25x, while the MSCI Emerging Markets Index and MSCI World Index trail P/Es are around 14x and 21x (as per the latest factsheets). Even on a 12-month forward P/E, India is commanding a visible premium vis-a-vis emerging markets and the world. Looking back in time, such expensive valuations were seen even in 2007-08, just before the Lehman Brothers collapse and the Global Financial Crisis.

In the case of midcaps and small-caps, the valuations are relatively even more expensive.

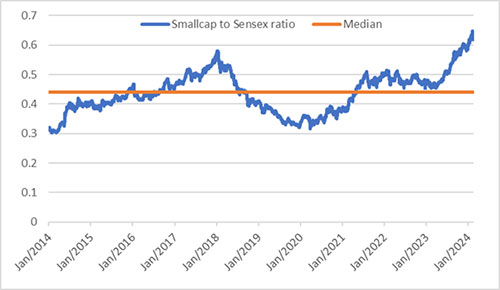

Graph 2: Smallcap Index-to-Sensex Ratio is at a Peak

Data as of February 16, 2024

Data as of February 16, 2024

(Source: ACE MF, data collated by PersonalFN Research)

The S&P BSE Smallcap to Sensex ratio, a determinant of valuations in the small-cap segment, currently stands over 0.60 versus a long-term median of 0.44. These levels were last seen in 2018, just before the mid and small-cap crash of 2018-19.

This clearly indicates that valuations aren't cheap, and the margin of safety seems to have narrowed. It would be unwise to get carried away by irrational exuberance and expect extraordinary returns from small caps.

Note that, equity markets move in cycles - a bull phase is followed by corrections or bear phases and vice versa. If things on the economic and political front do not pan out to what markets expect, equities may correct from their current lifetime high levels. In such times, small caps and Small Cap Funds would be more vulnerable or risky. Simply put, they may fall more than the Mid Cap Funds and Large Cap Funds. In other words, they could disappoint you, the investor.

When approaching Small Cap Funds, here are things you should clearly avoid:

-

Going gung-ho at a market high

-

Zeroing on funds by giving too much weightage to recent past performance

-

Expecting super-normal returns to continue

-

Keeping the mindset of a trader

-

Acting on unsolicited advice from inexperienced individuals

When investing in small caps, you ought to be mindful of the fact that they are less liquid, may have weak cash flows and high leverage, and could have corporate governance issues. Watch this video:

How to Approach Small Cap Funds

Investing in Small Cap Funds is not for the fainthearted, and even if wish to take high risk, you need to follow a sensible asset allocation and have a longer time horizon of 7 to 10 years.

From an asset allocation perspective, Small Cap Funds should not be more than 10-15% of the entire equity portfolio and should be part of satellite holdings (not core holdings) that potentially could push up the portfolio returns.

Whereas the 'Core' portfolio may comprise more stable and long-term holdings (such as a Large Cap Fund, Flexi Cap Fund, and a Value Fund).

[Read: Do Large Cap Funds Make More Sense in An Overheated Equity Market?]

By wisely structuring your mutual fund portfolio (based on your age, risk profile, broader investing objective, the financial goal/s you are addressing, and investment time horizon), you would set the path to wealth creation.

To invest in small-caps, prefer small-cap funds that follow robust investment processes and systems, pay close attention to liquidity, market capitalisation, and hold an optimally diversified portfolio (of around 40 to 60 stocks) with conviction.

Choose a Small Cap Fund scheme that is true to its label. Invest sensibly and be a thoughtful investor.

When in doubt, don't hesitate to reach out to a SEBI Registered Investment Advisor.

Happy Investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.