Gold ETFs vs Gold Savings Funds: 5 Key Differences You Should Know

Rounaq Neroy

Mar 24, 2025 / Reading Time: Approx. 9 mins

Listen to Gold ETFs vs Gold Savings Funds: 5 Key Differences You Should Know

00:00

00:00

India's enduring love for gold is not only because of its immense cultural significance but also due to its repeatedly proven mettle as a safe-haven asset during economic uncertainties.

Very recently, gold prices hit a record high of Rs 91,250 per 10 grams in the national capital. As of March 21, 2025, the MCX spot price per 10 grams of gold stood at Rs 87,821.

Gold prices have surged by 17% so far in the current calendar year 2025 and have remarkably outperformed equity and debt. It wouldn't be far-fetched to expect the prices to breach Rs 1 lakh in the near future.

Here are some of the factors working in favour of gold:

-

Global central banks continue to accumulate gold reserves, with the demand crossing 1,000 tonnes for the third consecutive year in 2024.

-

Uncertainty over U.S. President Donald Trump's protectionist policies and tariff tantrums instigating a global trade war.

-

Persistent geopolitical tensions, such as Israel's military operations in Gaza.

-

The Federal Reserve indicating that it would reduce interest rates in CY2025 with two possible cuts

-

A weakening Indian rupee against the greenback, which often leads to a rise in gold prices denominated in rupees.

-

Risk to the inflation outlook due to Trump's protectionist measures, sticky food inflation, and adverse weather events.

Periods of economic uncertainties like these heighten investors' risk aversion and push them towards gold as a safe-haven asset, a hedge against inflation, and an effective portfolio diversifier.

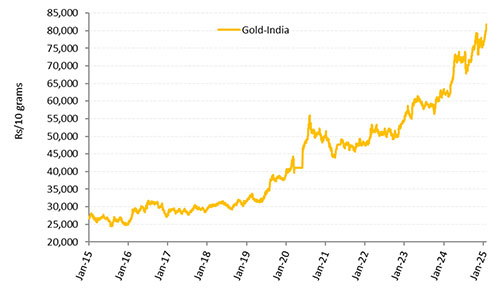

As seen in the Graph below, gold prices have significantly surged in the past decade, and the asset has displayed its sheen.

Graph: Gold Has Displayed Its Sheen in the Long Run

Data as of March 21, 2025

Data as of March 21, 2025

(Source: MCX, data collated by PersonalFN)

Now, while gold has been regarded as one of the safest and most promising investment avenues since time immemorial, the approach to gold investment has evolved significantly over time.

While the demand for physical gold surges during the wedding season and festivals, the associated storage expenses and the risk of theft remain a concern.

Sovereign Gold Bonds, a popular choice among gold investors, were recently discontinued by the government citing high borrowing costs.

At present, Gold Mutual Funds are smart and a convenient way to invest in gold. These are classified into two categories: i) Gold Exchange Traded Fund, and ii) Gold Savings Fund.

In this article, let's understand the differences between these two types of gold mutual funds so that you can make informed decisions aligned with your investment needs.

What Are Gold Exchange-Traded Funds (Gold ETFs)?

Gold ETFs are passively managed and aim to track the domestic price of physical gold by making direct investments in gold. The units purchased are backed by 0.995 finesse of physical gold by the respective fund house, and 1 unit of Gold ETF is equivalent to 1 gram of gold.

The physical gold is held in vaults by an appointed custodian for the ETF on your, the investors' behalf. Additionally, this gold with the custodian is insured and valued periodically, as per the guidelines of the Securities and Exchange Board of India (SEBI).

The investment objective of a gold ETF is to generate returns broadly in line with the domestic price of gold. When gold appreciates and the NAV goes up, you, the investor benefits.

Note that if you wish to convert your Gold ETF units into physical gold at a future date, it is possible only for a certain quantity (usually 1 kg), and the entire process takes around 2 to 3 working days.

What Are Gold Savings Funds?

A Gold Savings Fund (or Gold Fund) is a Fund of Fund scheme investing in underlying Gold ETFs, which benchmarks the performance against the prices of physical gold.

The investment objective is to generate returns that closely correspond to returns generated by the underlying Gold ETF.

Keep in mind that these funds do not really invest in the stocks of firms that mine, refine, process, or package gold. They only make investments in gold through the underlying exposure to Gold ETFs. Gold Saving Funds strive to produce parallel returns closely with the underlying Gold ETF. Ultimately, the gold saving fund's performance is influenced by the actual price of gold.

Differences Between Gold ETFs and Gold Savings Funds

1. Demat Account

You need a demat account and trading account to invest in Gold ETFs. The purchase order can be placed through your broker, similar to the way you would buy shares on the recognised stock exchange.

In contrast, you do not need a Demat account to invest in a Gold Savings Fund. You can simply approach the fund house or your mutual fund distributor to buy units in a Gold Savings Fund.

The units will be purchased at the NAV declared by the fund house, and the allotted units will be reflected in your mutual fund account statement.

2. Minimum Investment Amount

Investing in Gold ETFs requires you to purchase ETF units, with a minimum purchase requirement of one unit. Purchasing 1 unit of Gold ETF equates to purchasing 1 gram of gold.

On the other hand, investors in Gold Savings Funds may purchase units for as little as Rs 500 with a single SIP, and in certain cases, Rs 100. The units are awarded based on the current NAV of the gold fund on that particular day.

Thus, the minimum investment amount required for ETFs is more compared to Gold Savings Funds.

3. Investment Costs

The primary costs associated with investing in Gold ETFs include demat charges, brokerage, expense ratio, etc. There is no exit load incurred when you sell the gold ETF. However, the sell transaction may be subject to a brokerage.

On the other hand, to invest in Gold Savings Funds, you do not have to bear demat account charges, brokerage, etc. All that you pay bear is the expense ratio, and on redemption an exit load, depending on within how many months from the date of investment the redemption is made.

4. How to Sell

To sell Gold ETF units, you must place an order with your broker, who will then execute it on the stock exchange. If the trade is executed successfully, the proceeds will be credited to your bank account on a T+2 basis, while the Gold ETF units will move out from your demat account.

To sell your units in a Gold Savings Fund, you must duly fill and sign the redemption request slip and submit it to the fund's Registrar and Transfer Agent (RTA) or to the distributor/agent, who shall then do the needful for you. The redemption proceeds will typically be credited to your bank account within 3 to 4 working days and the transaction shall also be reflected in your mutual fund account statement.

5. Liquidity

Gold ETFs, since they are traded on stock exchanges, liquidity is high.

Likewise, Gold Savings Funds are also regarded as liquid since they can be easily purchased or redeemed at any moment, just like any other equity mutual fund scheme. However, the time for redemption is slightly longer (3-4 working days) than when selling gold ETFs on the exchange.

Which is Better - Gold ETFs or Gold Saving Funds?

Well, considering the ease of investing and liquidity, Gold ETFs have an edge over Gold Saving Funds. The returns would correspond closely with the price of gold, subject to a tracking error.

The 5 Best Gold Mutual Funds in India to invest in are:

1. Axis Gold Fund

2. HDFC Gold Fund

3. Kotak Gold Fund

4. SBI Gold Fund

5. ICICI Prudential Regular Gold Savings Fund

[Read: Top Performing Gold Mutual Funds in India]

What Are the Tax Implications of Investing in Gold Mutual Funds?

Whether you invest in gold ETFs or gold mutual funds, they are considered non-equity schemes from a taxation point of view. Both, Short Term Capital Gains (STCG) and Long Term Capital Gains on gold mutual funds will be taxed as per your, the investor's/assessee's income-tax slab, i.e. at the marginal rate of taxation.

To Conclude...

In the current uncertain market environment, you can consider tactically allocating around 10% to 15% of your investment portfolio to gold and have an investment horizon of 7-10 years or longer. Keep in mind, that in the past years when equities have disappointed investors, gold has played its role as an effective portfolio diversifier and a store of value.

Both Gold ETFs and Gold Savings Funds are smart ways of investing in gold. That said, take the decision considering your personal risk profile, investment objective, financial goal/s, and the time in hand to achieve those goals. When in doubt, consult a SEBI-registered investment advisor to make an informed decision.

Be a thoughtful investor.

Happy investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.