How Rate Hikes May Impact Equity Markets and Your Mutual Funds

Rounaq Neroy

Sep 27, 2022

Listen to How Rate Hikes May Impact Equity Markets and Your Mutual Funds

00:00

00:00

Nothing seems to be deterring Indian investors for now-neither the evident risk of rising inflation nor rate hikes nor the widespread risk of a recession. The equity markets have been reeling under pressure since October 2021, almost for a year now. From its peak, so far, the bellwether Nifty 50 Index is down by -7.9%, while the Nifty Midcap 150 and the Nifty Smallcap 250 have taken a knock of -6.4% and -14.0%, respectively (as of September 26, 2022). Nonetheless, the correction is relatively shallow, thanks to intermittent pullback rallies.

Many market commentators have turned cautious with the world's largest central bank, the U.S Federal Reserve (Fed), increasing the interest rates unprecedentedly. Between March 2022 and September 2022, the Fed raised interest rates by 300 basis points (bps), an extremely steep hike considering its relatively moderate policy response during the last tightening cycle, i.e. between December 2015 and December 2018, when the Fed hiked the interest rates by 225bps.

The tone of the Fed's latest policy statement has been unequivocal. Bringing down inflation (which currently is at a multi-decade high of 8.3%) to 2% remains its top policy objective.

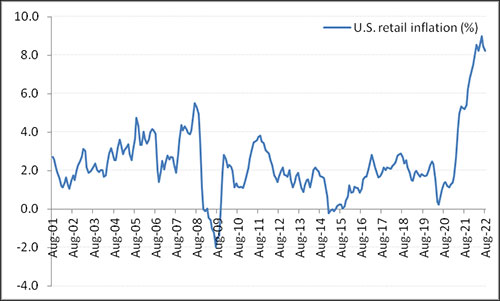

Graph 1: Inflationary pressure has dampened the economic growth prospects in the US

Data as of August 2022

Data as of August 2022

(Source: Federal Reserve, PersonalFN research)

The aggressive rate hikes of the past few months have now begun to reflect in the economic activity. The housing market has cooled off significantly, and consumer spending has slowed as well. Weaker economic prospects have dampened the business sentiment reflected in weaker capex and shrinking exports.

And it's not the Fed alone fighting inflation. Several central banks in both developed and emerging market economies have raised their policy interest rates to fight spiralling inflation.

[Read: Is Inflation Eroding Value of Your Investments? Learn How to Rebalance Your Portfolio]

The successive rate hikes have come after the accommodative or dovish stance taken to tackle economic challenges during the COVID-19 pandemic. But as monetary policy stimulus offered no help in dealing with the problem of supply chains, loose monetary policies proved a double whammy for inflation. The demand jumped significantly after lockdown restrictions were lifted, and supply failed to match as the Russia-Ukraine war exacerbated the situation.

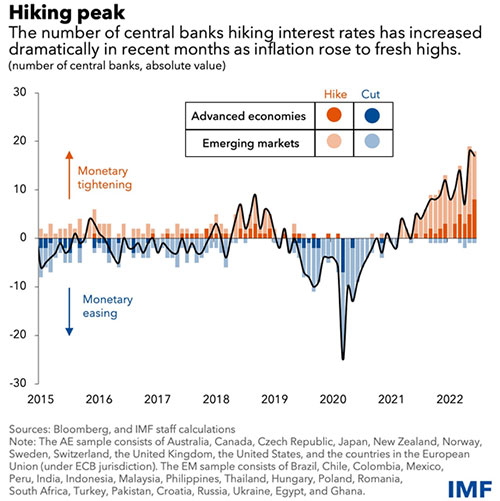

Graph 2: Unprecedented and synchronized rate hikes may cause a global recession

(Source: imf.org)

(Source: imf.org)

That said, some emerging market economies, particularly India, has evaluated the situation and adopted a more calibrated approach in the monetary policy stance. It was wisely assessed that the inflation wasn't transitory.

According to the World Bank, with central banks raising interest rates this year with a degree of synchronicity not seen over the past five decades-a trend that is likely to continue well into next year--the world may be edging toward a global recession in 2023 and a string of financial crises in emerging market and developing economies that would do them lasting harm.

"Global growth is slowing sharply, with further slowing likely as more countries fall into recession. My deep concern is that these trends will persist, with long-lasting consequences that are devastating for people in emerging market and developing economies." - David Malpass, World Bank Group President

Unless supply disruptions and labour-market pressures subside, those interest-rate increases could leave the global core inflation rate at about 5% in 2023, as per the World Bank's estimates. And to cut global inflation to a rate consistent with the targets, the central may need to raise rates further by an additional 2 percentage points, according to the report's model.

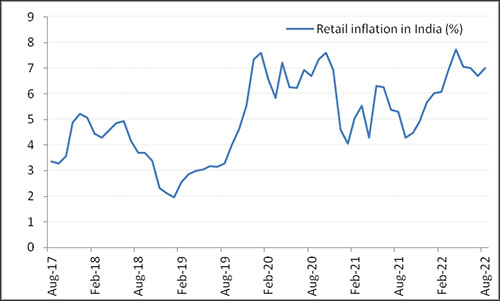

Graph 3: Spiralling CPI in India

Data as of August 2022

Data as of August 2022

(Source: Mospi, PersonalFN Research)

The Reserve Bank of India (RBI), too, if inflation pressures do not settle within the comfort range, is likely to increase the policy repo rate further, even if it costs GDP growth rate in the short term.

Fortunately, to India's benefit, Brent crude oil prices have fallen more than 30% from their 2022 peak. At present, the spot Brent crude oil is hovering at USD 90/per barrel, and for the purpose of inflation forecasting, the RBI has assumed a rate of USD 105/per barrel.

In one of the latest media interviews, RBI Governor Shaktikanta Das opined that inflation in India has perhaps peaked out already. He believes the number may drop to 5% by Q1FY24. But in my view, we need to see if these estimates really come true based on the ever-evolving situation.

Another factor that is playing out is the Indian rupee, which has depreciated nearly 7% against the U.S. Dollar (USD) since the start of FY23 and has already crossed the 81/USD level. Foreign exchange (Forex) reserves have also depleted to USD 545.7 billion as per the RBI data for the week ending September 16, 2022. This, again, is a factor that the RBI may take cognizance of for its policy intervention.

Other currencies also have weakened against the greenback. For instance, at 2.25%, the policy rates in the UK are at the highest levels since 2008, and the Great Britain Pound (GBP) has recently touched a fresh 20-year low (1 GBP = 1.08 USD).

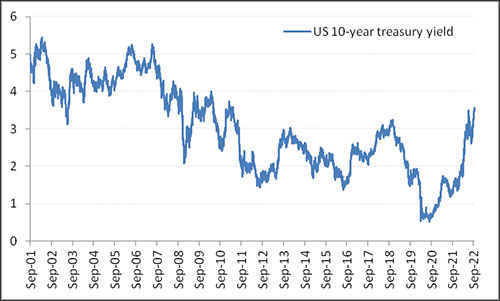

Graph 4: A sharp rise in treasury yields: a sign of potential meltdown in equities

Data as of September 26, 2022

Data as of September 26, 2022

(Source: macrotrends.net)

Owing to inflation, rate hikes by central banks in many parts of the world and depreciation in currencies, the U.S. long-term treasury yield has also inched up remarkably since last year.

The yield on India's 10-year benchmark bond has witnessed a rise of nearly 120 bps in the last one year (from the levels of 6.2% to 7.4% now), but this is more in line with the 140 bps increase in the policy rates by the RBI.

(Image source: freepik.com; photo courtesy @snowing)

(Image source: freepik.com; photo courtesy @snowing)

What will be the potential impact of rate hikes on the Indian Equity Markets?

Past experiences suggest that sharp interest rate hikes are often associated with the weaker subsequent performance of stock markets and vice-versa. The equity markets are already feeling the jitters or panicking because hawkish monetary policy measures and the chances of a global recession may leave a material impact on the business environment and corporate earnings. Thus, the chorus of doom and gloom is getting louder nowadays, and the bears are running amok. Nouriel Roubini, an economist famously known as Dr Doom, who forecasted the financial crisis of 2007-08, has warned investors of an ugly recession that can drag markets as much as 40%.

As you must be aware, a weaker global economy, a strong U.S. Dollar, and the prevalence of risk-off trade often flush out liquidity from emerging markets. The hardening of bond yields in the US suggests that the U.S. Dollar is likely to remain strong in the foreseeable future and the risk-off trade is likely to prevail. Higher bond yields usually result in a shift in focus from equities to debt.

Against the above backdrop, India may not really decouple. In other words, it may weigh down on macroeconomic indicators and market sentiments. A lot would depend on how the global funds flow and domestic participation in the Indian market.

Table: How have markets reacted to the U.S. Subprime mortgage crisis and the COVID-19 pandemic?

| Index |

Return (Absolute %) |

| October 2008-April 2009 (Impact of the U.S. Sub-prime mortgage crisis) |

January 2020-April 2020 (Impact of the COVID-19 pandemic) |

| S&P 500 |

-24.8% |

-10.6% |

| Nifty 50 |

-12.1% |

-19.7% |

(Source: ACE MF, PersonalFN Research)

Having said that, India is currently the fastest growing economy amongst the major economies -- and was so even during times of uncertainties. Backed by reforms, India has managed to do well despite the global crisis and remained a promising investment destination.

Even amidst the COVID-19 pandemic, the impact on corporate balance sheets has been better than anticipated earlier, and many companies managed to raise capital. Major Indian banks, too, raised capital over the last two-three years and now appear adequately capitalised.

India has a strong and vibrant domestic economy, and it's emerging as a strong manufacturing alternative, making it a perfect fit for the China+1 supply chain strategy. India's capex cycle has been showing signs of a strong revival, with major capital investments expected to happen in infrastructure, sustainability and manufacturing. As a result, prospects of corporate earnings in India remain bright.

The RBI has retained its FY23 real GDP forecast at 7.2% despite a slew of challenges witnessed over the last few months. RBI's data for the fortnight ended on September 9, 2022, suggests that the credit demand has expanded at 16.2% on a year-on-year (y-o-y) basis despite rate hikes since May this year. Such a high double-digit credit growth was witnessed back in November 2013. Amid the ongoing festive season and increase in capex demand, credit growth is likely to increase.

What will be the impact on your mutual funds?

As volatility in the Indian equity market intensifies, Small-cap Funds and Mid-cap Funds (due to dominant exposure to smaller companies) would be quite vulnerable compared to Large-cap Funds. As regards the performance of Multi-cap Funds and Flexi-cap Funds, it shall depend on the underlying portfolio characteristic (the market-cap orientation and quality of securities held) and the astuteness of the fund manager/s.

Likewise, with Focused Funds (that hold a concentrated portfolio), whether the conviction-driven bets really pay off. Similarly, Sector & Thematic Funds may draw very high risk if the macroeconomic conditions for the respective sector or theme are not so favourable. If the markets correct -- which is a high possibility -- there would be value-buying opportunities for Value Funds, and that may reward you, the investors, over the long term.

At present, valuation-wise, the Indian equity market seems better placed with the trail P/E of the Nifty 50 Index at around 20x, the Nifty Midcap 150 Index P/E at 25x, and the Nifty Smallcap 250 Index at 19x (as of September 26, 2022), compared to their peak. This provides a decent margin of safety, particularly amidst encouraging corporate earnings in the last couple of years.

That said, as a retail investor, it is important to devise a sensible strategy to make the best of the beaten-down markets while you invest in equities. Don't avoid investing in equities just because interest rates are moving up.

If you have a high-risk appetite and an investment time horizon of 3 to 5 years or more, equity as an asset class might be appropriate for you to generate decent real returns for you. Invest in the best equity funds following the 'Core & Satellite Approach'.

The term 'Core' applies to the more stable, long-term holdings of the portfolio, whereas the term 'Satellite' applies to the strategic portion that would help push up the overall returns of the portfolio across market conditions. This time-tested investment strategy is followed by some of the most successful equity investors, proving to be a wealth multiplier for them in the long run.

The 'Core' holdings should be 65%-70% of the portfolio and consist of equity funds such as Large-cap Fund, Flexi-cap Fund, and Value Fund/Contra Fund.

The 'Satellite' holdings, on the other hand, can be around 30%-35% and comprise of equity funds such as worthy Mid-cap Funds and an Aggressive Hybrid Fund.

When you construct an equity mutual fund portfolio based on the 'Core & Satellite Approach', you should ensure it does not contain more than 7 to 8 best equity mutual funds. There is no point in over-diversifying your equity mutual fund holdings.

It would be best to ensure that no more than two equity mutual fund schemes belonging to the same fund house are included in the portfolio.

Further, no more than two schemes in the portfolio should be managed by the same fund manager, all the schemes should have a strong track record of at least five years, they have outperformed over at least three market cycles, are among the top performers in their respective categories, and are abiding by the stated objectives, indicated asset allocation, and investment style.

Your objective as an investor should always be to try generating superior risk-adjusted returns higher than the risk-free rate.

If you are looking at investing in high-potential funds that are well capable of multiplying your wealth in the long run, I suggest subscribing to PersonalFN's Active Wealth Multiplier service, where my colleague Vivek Chaurasia will recommend you diversified equity mutual funds based on PersonalFN's proprietary smart alpha score and market conditions. This service includes active monitoring and guidance on the recommended funds so that you take timely actions that could generate market-beating returns. If you are serious about strategically investing in equity mutual funds, subscribe now!

Given that the equity markets would be very volatile, you may consider taking the SIP (Systematic Investment Plan) route over the lump sum while following the Core & Satellite investment strategy. The inherent rupee-cost average feature of SIPs will help mitigate the volatility, instil the good habit of investing regularly in a disciplined manner, and over the long-term help compound money. Watch this video on the 5 benefits of starting a SIP.

In a rising interest rate scenario if you are investing in debt mutual funds, stay away from longer-duration debt funds (with a maturity profile of 5 to 10 years), as they would be sensitive to interest rate risk and may witness high volatility in the near term. You will be better off deploying your hard-earned money in shorter-duration debt mutual funds, particularly Liquid Funds.

[Read: 3 Best Liquid Mutual Funds to Invest in 2022]

Whichever category of mutual funds you are investing in, assess your personal risk profile, your broader investment objective, the financial goal/s you wish to address, and the time in hand to achieve those envisioned goals. Based on set your asset allocation right and select the best schemes for your mutual fund portfolio.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter