The Key Factors Behind the Recent Volatility in the Indian Equity Market

Rounaq Neroy

Jan 14, 2025 / Reading Time: Approx. 12 mins

Listen to The Key Factors Behind the Recent Volatility in the Indian Equity Market

00:00

00:00

Financial markets are often likened to a roller coaster due to their inevitable ups and downs, and the recent events have made this comparison feel more real than ever.

On Monday, January 13, 2025, investors in India were left reeling as stock markets took a nosedive, with the BSE Sensex plummeting 1,048.90 points or 1.36% to hit a low of 76,330.01. Meanwhile, the NSE Nifty50 shed 345.55 points or 1.47% to close at 23,085.95 (the lowest since June 6, 2024).

The BSE Mid Cap and Small Cap indices also bore the brunt, with a sharp decline of 4% each.

The overall market capitalisation of BSE-listed firms declined sharply to approximately Rs 417 trillion down from Rs 430 trillion in the previous session, wiping out around Rs 13 trillion worth of investors' wealth in a single day.

Although the benchmark indices -- the BSE Sensex and the Nifty 50 -- have dropped by 1% during the initial seven sessions of January 2025, they are down up to 11% from their high recorded in September 2024. Volatility in the Indian equity market has surely intensified.

A variety of factors are behind this -- from a weakening Indian Rupee (INR) to a rise in global crude oil prices, slowing consumption, corporate earnings, profit booking, geopolitical landscape and much more.

Let's understand the key reasons...

1. Uncertainty Surrounding Trump's Trade Policies

As preparations are in full swing for U.S. President-elect, Donald Trump's inauguration on January 20, 2025, the financial markets are grappling with heightened uncertainty over the potential impact of his protectionist policies.

[Read: How Donald Trump's Victory Would Playout On the Indian Equity Market]

While Trump plans to cut tax rates in the U.S., speculation is rife that his administration might impose higher tariffs on imports from various countries, including India fuelling worries about geoeconomic fragmentation and inflation.

Additionally, potential changes to the U.S. tax policies or immigration laws are a source of unease for India's technology and export-driven sectors. These industries, reliant on the U.S. for business and talent mobility, may face significant disruptions if restrictive measures are introduced.

Now while Trump shares a good bonhomie with India's Prime Minister, Narendra Modi, recognising that Trump is a mercurial and transactional leader who likes to keep everyone guessing, the Indian equity market seems worried.

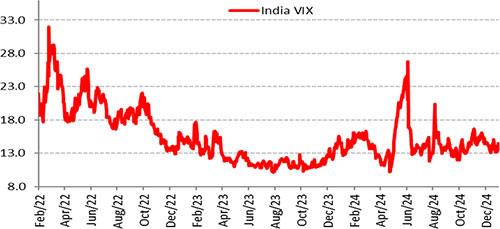

Graph 1: India's VIX

Data as of December 31, 2024

Data as of December 31, 2024

(Source: NSE, data collated by PersonalFN Research)

India's Volatility Index or VIX spiked soon after Trump's victory. The surge aligns with the global volatility trends and reflects growing concern in the Indian equity market.

2. Rising Crude Oil Prices

On January 13, 2025, crude oil prices reached their highest level in over three months, with Brent crude surpassing USD 81 per barrel.

This surge in prices has largely been attributed to expectations that U.S. sanctions could disrupt Russian crude supplies, impacting major importers such as China and India.

The rise in oil prices has sparked apprehensions about its potential impact on 'imported inflation' amidst a weak Indian rupee, given that India is one of the largest importers of oil.

If oil continues to rise further, it could get in the way of potential policy rate cuts by the Reserve Bank of India (RBI) in the near to medium term, further weighing on market sentiment.

3. Geopolitical Tensions

The ongoing military conflict between Russia and Ukraine, coupled with the recurring Israel-Hamas, and Israel-Hezbollah clashes in the Middle East, continues to keep global markets on edge.

Moreover, the relations between the U.S. and China, are strained. Trump's national security team sees China as the central economic and security threat to the U.S. They are committed to technological decoupling, geopolitical competition and strong support of Taiwan.

The U.S. military has also been supporting Taiwan primarily through the sale of arms & ammunition for decades to keep China away. Trump has consistently been in favour of strengthening the U.S. military to daunt China's aggression, particularly towards Taiwan.

The crisis over Taiwan may trigger a war between the U.S. and China, even though the U.S. does not have a treaty obligation to defend Taiwan. The U.S.'s strong support for Taiwan could intimidate China. Similarly, as you may know, there are tensions between China and the Philippines, as well as North Korea and South Korea.

Under Trump 2.0 the geopolitical landscape is likely to change. Among global risks, geopolitical conflicts and geo-economic fragmentation are perceived as high risks to the domestic financial system, according to the RBI's latest Financial Stability Report.

The medium-term outlook remains challenging, with downside risks from possible intensification of geopolitical conflicts, sporadic financial market turmoil, extreme climate events and rising indebtedness, as per the RBI.

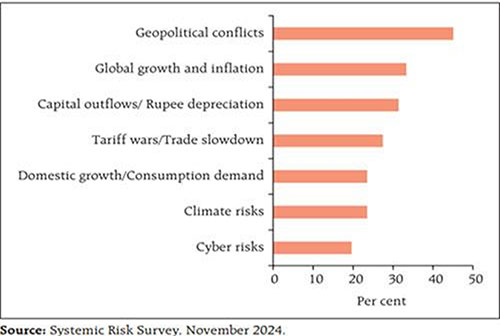

Graph 2: Potential risks to financial stability as per the RBI

(Source: RBI Financial Stability Report, December 2024)

(Source: RBI Financial Stability Report, December 2024)

According to the BlackRock Investment Institute's Geopolitical Risk Dashboard as of December 2024, as well the geopolitical risk has increased. While economies and markets have so far proven to be adaptable and resilient, the year 2025 is likely to test that resilience. These geopolitical tensions pose significant risks, as they have the potential to disrupt supply chains create uncertainty in the availability and pricing of vital commodities and may result in 'imported inflation'.

4. Vulnerable the Indian Rupee (INR) Against the Greenback

The INR continued its downward trajectory, reaching an all-time low of Rs 86.27 against the U.S. dollar (USD) in early trade on January 13, 2025. In CY2024 the INR has depreciated nearly 3.0%.

With protective trade policies under Trump 2.0, the INR is likely to be vulnerable against the U.S. Dollar, particularly in the first half of 2025.

Also, the hawkish comments from the U.S. Federal Reserve on rate cuts, i.e., an expected reduction of 50 bps versus 100 bps projected earlier, is likely to weigh on the INR.

This depreciation of INR is likely to intensify capital outflows as investors seek higher returns in dollar-denominated assets.

Moreover, it may widen India's Current Account Deficit, and may not yield much benefit to exports, as the trade deficit has already reached a record high (USD 37.8 billion in November 2024).

5. Decreased Hopes of U.S. Fed Rate Cuts

In December, the U.S. economy added 2.56 lakh jobs, significantly surpassing the anticipated 1.65 lakh. This surge in job creation brought the unemployment rate down to 4.1%, signalling robust economic momentum.

However, this positive economic data has dampened hopes of aggressive rate cuts by the Federal Reserve. Markets now expect the Fed to reduce rates by only 50 basis points, compared to the earlier expectation of a 100-basis-point cut.

While the present economic vigour of the U.S. economy is positive news for Trump as he takes charge on January 20, 2025, it has cast a shadow over global markets, including India. One needs to see the monetary policy actions of the RBI while the stance of the policy is changed to neutral.

6. Slowing GDP Growth

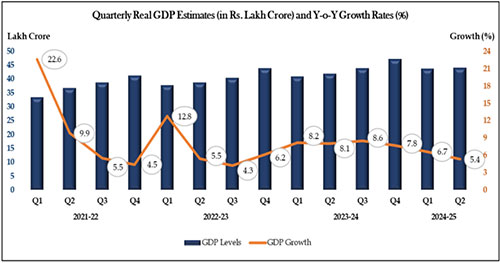

India's GDP in Q2FY25 slowed to 5.4% (a 7-quarter low) -- the lowest since Q3FY23 -- according to the data released by the National Statistics Office, Ministry of Statistics & Programme Implementation (MOSPI). Last year, in Q2FY24, GDP growth was 8.1%.

For the half year of the fiscal year 2024-25 (H1FY25), India's GDP growth was 6.0% versus 8.2% in H1FY24. The real GDP or GDP at Constant Prices in April-September of 2024-25 is estimated at Rs 87.74 trillion, against Rs 82.77 trillion in H1 of 2023-24.

Graph 3: India's GDP Growth Slowed in Q2FY25

Data as of September 2024 quarter for GDP at constant prices 2011-12.

Data as of September 2024 quarter for GDP at constant prices 2011-12.

(Source: Press Release Press Information Bureau, MOSPI.)

India's economic growth is projected to decelerate to a four-year low of 6.4% in FY25, according to the National Statistics Office's (NSO) First Advance Estimates. This figure falls short of the Reserve Bank of India's (RBI) projection of 6.6%.

The slowdown in economic growth has also led to a steep decline in credit consumption, particularly in critical sectors like housing and vehicles. Banks and NBFCs have also taken a more cautious approach to lending with the RBI tightening lending norms in recent times, further bogging down economic activity.

7. Corporate earnings Have Entered the Slow lane

India has seen encouraging corporate earnings growth in the post-pandemic period (in the last four years). India Inc.'s profit share in GDP was at 5.2% in FY24. However, of late, Q2FY25 corporate earnings have entered the slow lane due to decelerating demand or consumption and higher expenses or input costs. There is a cyclical downturn, which also is a factor that is not auguring well for the Indian equity market. The topline and bottom-line of most companies are expected to be slower than expected.

Disappointing corporate earnings of India Inc. are currently a big risk for the Indian equity market, as ultimately the earnings justify the valuations. Companies may face some headwinds in margin protection as rising costs will only be gradually passed on to consumers ultimately hurting demand.

In contrast in the U.S., the Q3 2024 corporate earnings of several S&P 500 companies are quite encouraging.

8. Massive FPI Selling

Foreign portfolio investors (FPIs) have intensified their sell-off in Indian equities, with January 2025 witnessing outflows exceeding Rs 213 billion. This comes on the heels of a significant outflow worth Rs 169 billion in December 2024.

The persistent selling is largely attributed to concerns over stretched valuations in Indian markets, weaker-than-expected corporate earnings, and the rising yields on U.S. bonds.

These elements have collectively dampened investor confidence, prompting FPIs to be net sellers in the Indian equity market.

How to Approach Investing in the Indian Equity Market Now

Current valuations in the midcap and smallcap segments of the market do not offer much comfort.

If the broader market falls more owing to the geopolitical tensions, protectionist policies of U.S. President-elect Donald Trump, and we see geoeconomic fragmentation, the midcaps and smallcaps may take further beating. I suggest, avoiding going overweight or skewing your investment portfolio, particularly to midcaps and smallcaps.

The largecaps, in comparison, would hold up better amid such times owing to the fact that they have been relatively inexpensive.

At the current juncture, a thoughtful and well-structured approach to equity investing is essential. A 'Core & Satellite' approach can be a prudent way to build a resilient portfolio.

The 'Core' portion of the portfolio should focus on quality Large Cap Funds that offer relative stability and have the potential to steadily grow your wealth over an investment horizon of around 5 years.

Additionally, exploring opportunities in Value/Contra Funds could be worthwhile, as these funds focus on undervalued/underperforming stocks with strong recovery potential.

You could typically allocate around 65%-70% of the equity portion in the best Largecap Funds, Flexi-cap Funds/Multi-cap Funds, and Value/Contra Funds as part of the 'core portfolio'.

The 'Satellite' portion of the portfolio, on the other hand, comprising up to 30%-35% of the equity portion, can include some of the best Mid-cap Funds(no more than two) and an Aggressive Hybrid Fund. But make sure to have an investment time horizon of at least 7-8 years when investing in these sub-categories of funds. If you are already having exposure to these sub-categories, refrain from adding more.

At this stage, also avoid adding Small Cap Funds or Sector/Thematic funds to your satellite portfolio unless you are a very aggressive investor with a very high-risk appetite and have an investment horizon exceeding 8 years. A deep understanding of these funds is essential to navigate their volatility.

This combination of a stable 'Core' and a selective 'Satellite' portfolio would pave the path for wealth creation, ensuring both stability and growth when investing in equities.

Remember, while equity investments offer growth opportunities, are inherently volatile. To mitigate risks, it is wise to diversify your portfolio across other asset classes. So, allocating to debt and fixed-income instruments, as well as gold, is also essential to add stability and may serve as a hedge during periods of equity market turbulence.

[Read: Equity, Debt, and Gold - Performance Review and Investment Outlook for 2025]

A Multi-Asset Allocation Fund could be a prudent choice for those seeking a tactical approach to asset allocation. These funds offer a diversified investment strategy within a single product, allowing you to benefit from different market conditions while maintaining a tactical allocation to equity, debt, and gold.

To Conclude...

Market corrections, economic headwinds, and volatility are an inherent part of equity investing. While such periods may test your, the investor's patience, they also present an opportunity to reassess and refine financial strategies for long-term success.

It's important not to let short-term fluctuations or volatility deter you from your long-term goals, especially those with an investment horizon of five years or more.

By staying focused on your long-term objectives, maintaining a well-diversified portfolio, and sticking to a disciplined investment approach, you can navigate market volatility with greater clarity and confidence.

A thoughtful and measured approach during challenging times not only helps protect your portfolio but also positions it to capitalise on future opportunities.

Happy investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.