What Does Slowdown in India's GDP Growth in Q2FY25 Mean for Your Mutual Fund Investments

Rounaq Neroy

Dec 02, 2024 / Reading Time: Approx 12 mins

Listen to What Does Slowdown in India's GDP Growth in Q2FY25 Mean for Your Mutual Fund Investments

00:00

00:00

India's GDP for the second quarter of the fiscal year 2024-25, July to September (Q2FY25) has slowed to 5.4% -- a 7-quarter low (the lowest since Q3FY23) -- according to the data released by the National Statistics Office, Ministry of Statistics & Programme Implementation (MOSPI). Last year, in Q2FY24, GDP growth was 8.1%.

The real GDP or GDP at constant prices in Q2 of 2024-25 is estimated at Rs 44.10 lakh crore, against Rs 41.86 lakh crore in Q2 of 2023-24.

The Gross Value Added (GVA), which excludes taxes and subsidies and is an important indicator of economic activity, has also slowed to 5.6% in Q2FY25 compared to 7.7% in Q2FY24.

The real GVA in Q2 of 2024-25 is estimated at Rs 40.58 lakh crore, against Rs 38.42 lakh crore in Q2 of 2023-24.

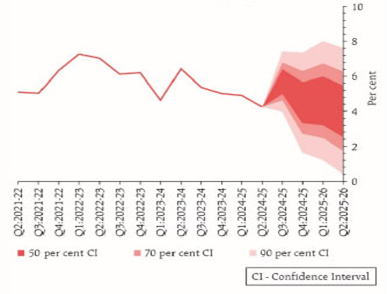

Graph 1A and 1B: Quarterly GDP and GVA Estimates along with Y-o-Y Growth Rates from Q1FY22 to Q2FY25 at Constant Prices

(Source: MOSPI Press Release)

(Source: MOSPI Press Release)

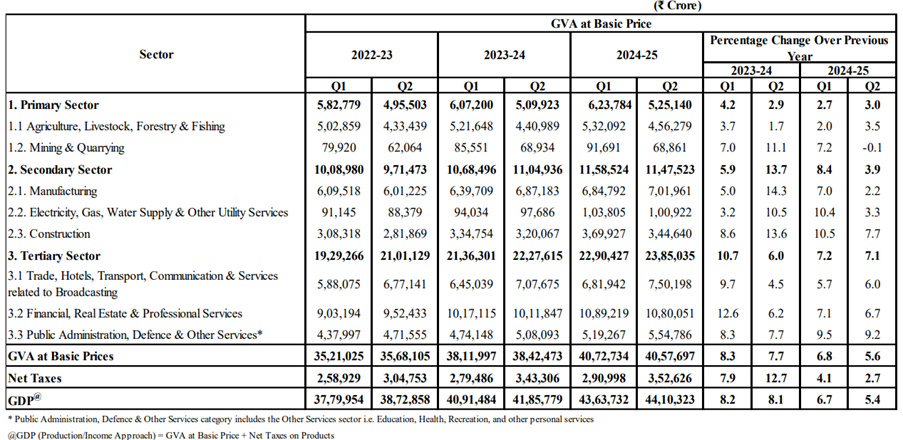

A sluggish growth in terms of GVA was observed in Manufacturing (at 2.2%) and a contraction in Mining & Quarrying (-0.1%) in Q2FY 25 compared to the same quarter last year.

Even construction activity (at 7.7%) slowed compared to the previous quarter and Q2FY24. Likewise, Electricity, Gas, Water Supply and Other Utility Services, report a lower growth rate compared to Q2FY24.

Whereas the GVA growth in Trade, Hotels, Transport, Communication & Services related to Broadcasting (at 6.0%), Financial, Real Estate & Professional Services (at 6.7%) and Public Administration, Defence & Other Services, i.e. Education, Health, Recreation, and other personal services (at 9.2%) was better than Q2FY24.

Similarly, Agriculture, Livestock, Forestry & Fishing, which are among the primary sectors did a tad better (at 3.0%) compared to Q2FY24.

Table 1: Quarterly Estimates of GVA at Basic Prices for Q2FY25 (at 2011-12 Prices)

(Source: MOSPI Press Release)

(Source: MOSPI Press Release)

So, it can be said that some of the primary and tertiary sectors proved supportive for Q2FY25 GDP data, while the growth in secondary sectors slowed down remarkably.

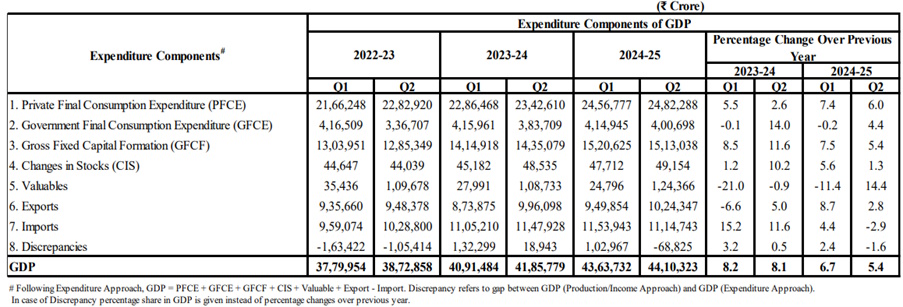

When we look at the expenditure component of GDP, an evident slowdown was seen in Private Final Consumption (which accounts for nearly 60% of GDP). This was perhaps owing to higher borrowing costs and stagnation of real wages (adjusted for inflation, which reflects the purchasing power of hard-earned money).

Table 2: Quarterly Estimates of Expenditure Components of GDP for Q2FY25 (at 2011-12 Prices)

(Source: MOSPI Press Release)

(Source: MOSPI Press Release)

The Government Final Consumption Expenditure (GFCE), which represents the government's spending on goods and services and accounts for nearly 10% of GDP, was also subdued compared to Q2FY24 (See Table 2).

India's Gross Fixed Capital Formation (GFCF) which reflects on how much new investments were made, also slowed to 5.4% in Q2FY25 versus the previous quarter and Q2FY24. It accounted for 34% of the current GDP.

Similarly, exports showed a diffident growth of 2.8% in Q2FY25 compared to the previous quarter and Q2FY24.

For the half year of the fiscal year 2024-25 (H1FY25), India's GDP growth is 6.0% versus 8.2% in H1FY24. The real GDP or GDP at Constant Prices in April-September of 2024-25 is estimated at Rs 87.74 lakh crore, against Rs 82.77 lakh crore in H1 of 2023-24.

Similarly, on a GVA basis, the growth reported in H1FY25 is 6.0% compared to 8.2% in H1FY24. The real GVA in H1 of 2024-25 is estimated at Rs 81.30 lakh crore, against Rs 76.54 lakh crore in H1 of 2023-24.

The Chief Economic Advisor to the government, Mr V Anantha Nageswaran has described the GDP data as "disappointing but not alarming".

He is confident that going forward, doubling down on deregulation, expanding state capacity for public investment, and improving hiring and compensation policies in the private sector, will improve growth prospects and turn the second quarter numbers into a fading memory.

Impact on the Indian Equity Market

The current Slowdown in GDP is now weighing down on the sentiments in the Indian equity market.

Further, weakness in GDP growth is also seen in India Inc.'s corporate earnings. For Q2FY25, the earnings data has been uninspiring with 4% year-on-year growth reported by the frontline Nifty companies.

A Business Standard report cites that earnings growth has been uneven with several sectors such as metals, oil & gas, power, auto, and FMCG facing a slowdown.

Only the Banking & Financial Services (BFSI) sector and certain companies in the construction and infrastructure space are driving earnings. In the case of BFSI, several well-known banks and NBFCs have already reported high delinquencies in personal loans and credit cards of late (since July 2024). So, there is stress building up in these portfolios of banks as Indian consumers aspire to meet their desires.

It should be noted that if the credit funnel narrows (as a consequence of regulatory tightening and a higher level of due diligence), India's consumption slowing down further cannot be ruled out.

Also, a fact is that lately elevated CPI inflation (across several goods and services), is impacting discretionary spending among the lower middle class and the middle class and is weighing on India's consumption story. It is sort of pushing back consumers and they are focusing only on non-discretionary spends currently. The Ministry of Finance's latest monthly review has acknowledged consumer demand is softening.

If CPI remains above the RBI's target range of 2-6%, it may deter the RBI from cutting rates -- although the finance minister, Ms Nirmala Sitharaman, of late, has been batting for lower policy interest rates to boost private investments and support economic growth.

In the December 2024 bi-monthly monetary policy statement 2024-25, it looks unlikely that the RBI would cut the policy repo rate in a hurry, given that CPI inflation data for October 2024 (released on November 12, 2024)

If CPI inflation comes down, perhaps in the February 2025 bi-monthly monetary policy the RBI may cut the policy rates or may even give it a miss and consider cutting rates in the fiscal year 2025-26.

Such domestic macroeconomic factors will continue to have a bearing on the Indian equity market and the returns you could expect from your equity mutual funds.

Current Valuations of the Indian Equity Market

At present, the Indian equity market continues to command a premium compared to its global peers.

The Morgan Stanley Capital International (MSCI) India Index trail Price-to-Equity (P/E) ratio is over 27x while the MSCI Emerging Markets Index and MSCI World Index trail P/Es are around 16x and 22x, respectively, as per the latest factsheets.

While India's valuation premium dropped a bit since the peak, it is still way above the MSCI Emerging Markets Index and the World Index.

Even on a 12-month forward P/E, India with a P/E of nearly 23x is commanding a premium vis-a-vis the MSCI Emerging Market Index and World Index whose forward P/E is around 12x and 19x, respectively.

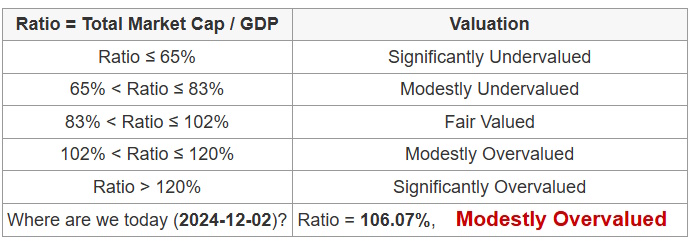

Table 3: India's current Market cap-to-GDP ratio

Data as of December 1, 2024

Data as of December 1, 2024

Based on historical values, divided into five zones.

(Source:https://www.gurufocus.com/global-market-valuation.php?country=IND)

Currently, even India's market capitalisation-to-GDP ratio, famously called the Buffett indicator (named after legendary investor Warren Buffett), is in the 'modestly overvalued' zone notwithstanding some correction since the peak.

Investment Strategy to Follow Now

Considering the valuations and that against the backdrop of geopolitical tensions, there are chances of geoeconomic fragmentation and global economic uncertainty, when investing in equities it would be imprudent to get carried away and expect equities to clock stellar returns, as you witnessed in the past.

Note that past returns are in no way indicative of future returns. It is important to keep your return expectations rational, given that volatility would increase. Also, it is not always true that that high risk translates into high returns.

When investing in equities, it would be wise to follow a Core & Satellite' approach -- a strategy followed by some of the most successful equity investors around the world.

The term 'Core' refers to the portfolio's more stable, long-term equity holdings. Given that, your core portfolio of the equity mutual fund portfolio should mainly comprise some of the best Large Cap Funds, Flexi-cap Funds/Multi-cap Funds, and Value/Contra Funds that can add stability to the investment portfolio and potentially steadily multiply your wealth by keeping an investment horizon of around 5 years.

The 'Satellite' portion of the portfolio, on the other hand, may include a couple of best Mid-cap Funds (max 2) and an Aggressive Hybrid Fund. When considering these funds, keep an investment time horizon of around 7 to 8 years. These funds would support boosting the portfolio's overall returns given their risk-return characteristics.

At this juncture, avoid adding Small Cap Funds and Sector/Thematic Funds to the satellite portfolio, unless you are a very, very aggressive investor with a stomach for very high risk, a time horizon of over 8 years, and have a good understanding of these funds.

Such a 'Core & Satellite' investment strategy shall prove sensible when deploying money into equity funds to address your long-term financial goals.

Given that there are chances of high volatility, it would be prudent to make staggered lump sum investments, or even better is to take the Systematic Investment Plan (SIP) route, particularly when planning for your long-term financial goals.

[Read: Micro SIPs in Mutual Funds: Is It a Good and Feasible Idea?]

When investing in debt, given that interest rates in the Indian economy have almost peaked, ideally it would be an opportune time to invest (around 25% of your debt portfolio) in some of the best Medium to Long Duration Debt Funds keeping an investment horizon of 3 to 5 years and assuming some interest rate risk.

To play the interest rate cycle with the expertise of a debt fund manager, some of the best Dynamic Bond Funds are meaningful, provided you have an investment time horizon of 3 to 5 years.

For a shorter investment horizon of 2 to 3 years, some of the best Banking & PSU Debt Funds may be a meaningful choice.

For a more short-term horizon, say, a couple of months to a year, some of the best Liquid Funds would be an ideal choice.

[Read: Best Debt Mutual Fund Categories for 2025]

Whichever sub-category of debt mutual funds you choose, be mindful of the fact that investing in debt funds is not 100% risk-free or safe (as in the case of an FD with a robust bank). Hence, choose debt mutual fund schemes that have worthy portfolio characteristics, i.e. the ones that hold a quality portfolio and do not engage in yield hunting.

To invest in debt funds, you could make lump sum investments (as they are less volatile than equity funds) considering your liquidity needs and risk profile.

It also makes sense to allocate around 10% to 15% of your entire investment portfolio to gold and hold with a long-term view (of over 8 to 10 years) by assuming a moderately high risk. Given that there are headwinds in play, geopolitical tensions, chances of global economic uncertainty, and that global debt is burgeoning, the spotlights will stay on gold. Considering this, even central banks of the world are also adding sizeable amounts of gold to their reserves. Having a tactical allocation to gold would prove to be an effective portfolio diversifier.

Invest sensibly following the best-suited asset allocation for you.

Be a thoughtful investor.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.