Sovereign Gold Bond Scheme Discontinued: Why This is Done and What It Means for Investors

Rounaq Neroy

Feb 05, 2025 / Reading Time: Approx. 8 mins

In one of my previous articles on Sovereign Gold Bonds, I drew attention to the point that the central government may discontinue the Sovereign Gold Bond (SGB) scheme, considering the higher borrowing cost involved.

Very recently, in the post-Union Budget 2025-26 briefing, Finance Minister, Ms Nirmala Sitharaman when questioned about the future of the SGB scheme -- as no issuance of SGB happened after February 2024 -- she responded, "Yes, in a way", acknowledging the discontinuation.

Elaborating on the government's decision at the briefing, Economic Affairs Secretary, Mr Ajay Seth said, "These are the decisions which are taken with the purpose of raising borrowings from the market, for the purpose of financing the Budget, and at some point of time, whether this asset class is to be supported or not. The recent past experiences have been that this has been a rather fairly high-cost borrowing for the government. As a result, the government has chosen not to follow that path".

This was expected because in August 2024, the Reserve Bank of India (RBI), the issuing authority of SGBs, announced a premature redemption window for SGBs issued between May 2017 and March 2020.

Despite the allocation of Rs 18,500 crore for SGBs in the FY2024-25 Budget (down from Rs 26,852 crore in the Interim Budget), no new tranches have been issued in the current fiscal year.

The last tranche was offered in February 2024 at an issue price of Rs 6,263 per gram.

SGBs were first issued back in 2015 by the RBI (the issuing authority). Since its inception, the scheme has seen total issuances worth Rs 45,243 crore as of FY23, with an outstanding amount of Rs 4.50 lakh crore by March 2023.

But after the finance minister announced the reduction in basic customs duty on gold from 15% to 6% in the Union Budget 2024-25 presented on July 23, 2024, in the following month August 2024, after the reduction in customs duty, gold imports surged by approximately 104% year-on-year in August 2024, reaching USD 10.06 billion.

This surge was expected, given India's cultural affinity for gold. As you may know, the demand for physical gold rises during festivals and weddings.

However, this spike contradicted one of the key objectives of the SGB scheme -- reducing physical gold imports and improving India's trade deficit.

Now while SGBs earned decent returns (around 9-11% return per annum, and on top of that an interest of 2.50%, as cited by a senior government official), the scheme has proved financially burdensome for the government.

As you may know, the redemption price of SGBs is based on the average closing price of 999 purity gold (as published by the India Bullion and Jewellers Association Ltd for the preceding three business days).

The current rise in gold prices means that the government has to pay higher amounts to investors at the time of redemption.

Since the launch of the scheme in 2015 (maturity period of 8 years and earning an annual interest of 2.75%, which was later revised to 2.50%), the price of gold has been on a consistent upward trend amidst economic uncertainty and geopolitical tensions, reinforcing its reputation as a safe haven or a store of value.

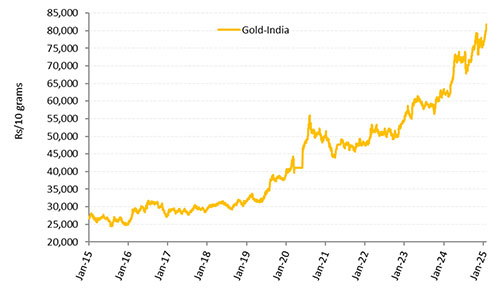

Graph: Gold Has Displayed Its Sheen in the Long Run

Data as of January 31, 2025

Data as of January 31, 2025

(Source: MCX, data collated by PersonalFN Research)

Around the time the RBI announced the premature redemption window (August 2024), the price per 10 grams of gold had already scaled over Rs 71,000. Today the spot price of gold in the National Capital Region is over Rs 85,000 per 10 grams for 99.9 per cent purity (as of February 4, 2025). In CY2024, the precious yellow metal clocked a remarkable 20.6% absolute returns -- marking its strongest performance since CY2020.

What Are the Implications for the Current SGB Investors?

The government has not announced any official changes affecting current investors of SGBs.

If you are an SGB investor, you're likely to continue receiving the 2.50% annual interest until maturity, with redemptions proceeding as per the original terms.

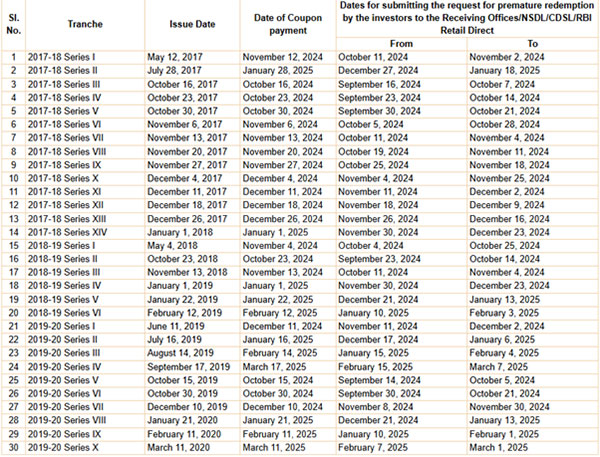

If you wish to exit early, you can use the RBI's premature withdrawal window for SGBs issued between May 2017 and March 2020, carried out in phases between October 11, 2024, and March 1, 2025.

Table: Schedule for Premature Redemption of SGBs

(Source: https://www.rbi.org.in/)

(Source: https://www.rbi.org.in/)

If you're planning to submit a premature redemption request between February 7, 2025, and March 1, 2025 (for 2019-20 Series X), note that the Reserve Bank has also stated that the specified dates may change in the event of unscheduled holiday/s.

To prematurely redeem SGBs, contact the bank or agent through whom you purchased the SGBs.

Remember, the RBI accepts premature redemption requests one month before the interest payout date, so ensure you initiate the process well in advance.

It is also important to understand the tax implications of early exits before making your decision.

The semi-annual interest earned on SGBs is taxed under the head 'Income from Other Sources' (under the Income Tax Act) as per your applicable income tax slab, i.e., at the marginal rate of taxation.

The proceeds from the premature redemption of the SGB through the RBI window (available after five years of holding) are exempt from Long Term Capital Gains Tax, as per the current tax rule.

However, if SGBs are sold or transferred on the stock exchange, any Long Term Capital Gains (for a holding period exceeding 12 months) will be subject to a flat 12.5% tax under Section 112 of the Income Tax Act, 1961 (plus the surcharge and health and education cess as applicable).

If you hold the SGBs until their full maturity period of eight years, the resulting capital gains will be exempt from tax, as they are not considered a transfer for capital gains.

Hence, if you are considering redeeming from SGB either utilise the premature redemption window made by the RBI or hold until maturity period 8 years to save from the axe of tax.

How to Invest in Gold Now?

Instead of buying physical gold, I suggest the smart option of a Gold ETF and/or Gold Savings Fund.

They are worthwhile to gain exposure to gold without the concerns of physical storage, risk of theft/loss, and quality.

Benefits of investing in a Gold ETF and/or Gold Savings Fund include...

-

Invest at prevailing market prices without paying additional premiums associated with physical gold.

-

Serves as a valuable portfolio diversifier.

-

Highly liquid, allowing a quick sale at prevailing market prices without the need for time-consuming quality checks.

To Conclude...

Even after the discontinuation of SGBs (and premature withdrawal if you choose to do so), gold remains a valuable investment asset with its traits as a safe haven, an effective portfolio diversifier, and a store of value during economic uncertainty.

You may consider allocating 10-15% of your entire portfolio to gold by way of a Gold ETF and/or Gold Savings Fund and hold them with a long-term view (of over 5 to 10 years) by assuming moderately high risk.

[Read: Top 5 Gold Mutual Funds in India]

A fact is unlike financial assets, gold is a real asset -- meaning gold does not carry credit or counterparty risk. Even a stronger U.S. Dollar -- typically seen during the stagflation period -- hasn't dampened the sentiments toward gold, according to the WGC.

Approach your investments sensibly, considering the tax implications, your risk profile, overall investment objectives, and the time horizon to achieve the envisioned financial goals.

Happy investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.