How’s the Union Budget 2023 for the Common Man

Rounaq Neroy

Feb 02, 2023 / Reading Time: Approx. 14 min

Listen to How’s the Union Budget 2023 for the Common Man

00:00

00:00

The most awaited full final Union Budget 2023-24 of the Modi 2.0 government before the Lok Sabha election 2024 was announced. As expected, it has done three key things: 1) laid emphasis on growth (by increasing the capital investment outlay by 33% to Rs 10 lakh crore, which is 3.3% of GDP for FY24); 2) walked the path of fiscal consolidation (by estimating the fiscal deficit at Rs 17.87 lakh crore or 5.9% of GDP for FY24 and further down to 4.5% of GDP by FY25) --much needed in times of economic uncertainty and global slowdown, and 3) tried to make the common man happy by tweaking certain tax proposals.

As a result, the Indian equity markets also gave a thumbs up, creating wealth for investors after being rather volatile in the previous few sessions.

Here are 12 key proposals that have a positive impact on the common man:

1. Food and Nutritional Security -- The government has decided to implement from 1st January 2023 a scheme under the Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) that shall supply free food grain to all Antyodaya and priority households for the next one year. The entire expenditure of about Rs 2 lakh crore estimated for this will be borne by the central government, which would ensure food and nutritional security to the poor.

2. Increased expenditure on health and education -- To facilitate better healthcare facilities, a sum of 86,175 crore has been allocated to the department of health and family welfare while Rs 2,980 crore has been allocated to the department of health research. In the current fiscal year, the government spent Rs 76,370 on health and family welfare, while Rs 2,775 crore had been marked for the department of health research.

For education Rs 1,12,899 crore is proposed in FY24, which is nearly 8.26% (or Rs 8,621 crore) more than the previous budget estimate of Rs 1,04,278 crore. Moreover, for higher education Rs 44,094 crore has been allocated, which is 7.9% higher than the budget estimate for FY23.

Other than that, the union budget speech stated Pradhan Mantri Kaushal Vikas Yojana 4.0 will be launched to skill lakhs of youth in the next three years. This shall bring with it on-job training, industry partnership, and alignment of courses with the needs of the industry.

The Pradhan Mantri Kaushal Vikas Yojana 4.0 will also cover new-age courses for Industry like coding, AI, robotics, mechatronics, IOT, 3D printing, drones, and soft skills. To skill the youth for international opportunities, 30 Skill India International centres would be set up across different states.

Besides, the launch of a unified Skill India Digital platform is announced, which shall provide a digital ecosystem for skilling. This shall facilitate demand-based formal skilling, linking with employers including the MSMEs, and access to entrepreneurship schemes.

This in my view was the need of the hour to make the youth future-ready and employable. Likewise, the increased allocation to education and healthcare is encouraging (given that currently these sectors comprise roughly only around 3.5% of GDP, much less than some of the global peers), but for the for benefits to percolate, implementation is the key.

3. Integrated IT portal for Unclaimed Shares and Dividends -- Owing to whatever reasons if you have some unclaimed money lying in the form of unclaimed shares or unpaid dividends, to reclaim from the Investor Education and Protection Fund Authority, an integrated IT portal will be established making it easy to access such unclaimed money.

4. Introduced a small savings scheme for women -- Commemorating Azadi Ka Amrit Mahotsav and encouraging women and girls to invest, a one-time new small savings scheme, the Mahila Samman Savings Certificate (MSSC) is introduced.

MSSC will be made available for a 2-year period up to March 2025 allowing women or girls a deposit facility up to Rs 2 lakh (for a tenor of 2 years) earning a fixed interest rate of 7.5% p.a. and partial withdrawal facility. After the Sukanya Samriddhi Yojana (which is specifically designed for the girl child), this is the second small savings scheme targeted at women and girls by the government, encouraging them to make investments in their own name and take control of their finances.

5. Enhanced the maximum deposit limit for Senior Citizen Savings Scheme -- In a move that would prove meaningful for senior citizens to earn a regular income, the government increased the maximum deposit limit under the Senior Citizen Savings Scheme (SCSS) from Rs 15 lakh to Rs 30 lakh.

With the interest rates having gone up of late, SCSS is a worthwhile avenue for retirees offering 8.0% p.a. interest, compounded annually, over the 5-year maturity period of SCSS.

The investment made in SCSS entitles you to a deduction of up to Rs 1.50 lakh (from Gross Total Income) under Section 80C of the Income Tax Act, 1961 in the year the investment is done if you opt for the Old Tax Regime.

While the interest earned is taxable as per your income tax slab (but first subject to tax deduction at source if interest income earned in a financial year is greater than Rs 50,000 per financial year) to avoid tax at source, you can furnish Form H to the bank/post office if the accrued interest earned is less than the aforesaid prescribed limit.

If you are a risk-averse retiree seeking to draw a regular source of interest income, surely investment in SCSS can help complement investment planning and tax planning.

6. Enhanced the maximum deposit limit for Monthly Income Account Scheme -- The Union Budget 2023-24 also increased the maximum deposit under this scheme from Rs 4.5 lakh to Rs 9 lakh for a single account, and from Rs 9 lakh to Rs 15 lakh for a joint account.

For someone who is risk-averse and looking for monthly income, the Post Office Monthly Income Scheme (POMIS) similarly is a good option. Given the current interest rate of 7.1% p.a. payable on completion of a month from the date of opening and so on till maturity of 5 years, investment in POMIS can offer a decent real rate of return as inflation moderates further. That said, the interest earned on the POMIS account will be taxable as per your income tax slab.

7. Conversion of Gold to Electronic Gold Receipt not to attract capital gains tax -- Considering the fact that India currently is the second largest consumer of gold -- mostly held in physical form -- and to encourage financialisation of gold holdings, the Union Budget 2023-24 proposed not to treat the conversion of physical gold to Electronic Gold Receipt and vice versa as 'transfer' and therefore not levy capital gains tax on it. However, the finance minister has proposed to increase the customs duty on gold (thus making physical gold expensive). Hopefully, this shall promote the culture of holding gold the smart way in the form of Sovereign Gold Bonds (SBGs), Gold ETFs, and Gold Savings Funds.

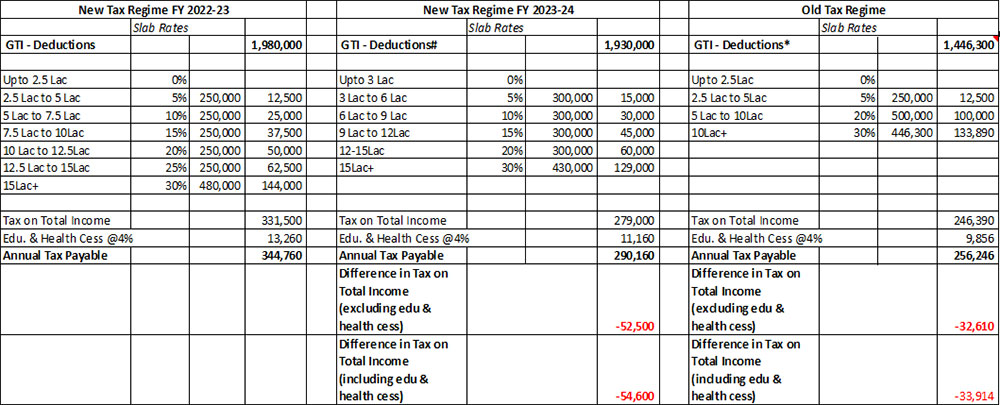

8. Increased the tax rebate limit to Rs 7 lakh under the New Tax Regime -- Currently, those with income up to Rs 5 lakh in a financial year do not pay any income tax in both Old and New Tax Regimes. Thus, the tax rebate limit is enhanced to Rs 7 lakh in the financial year under the New Tax Regime, whereby persons with income up to Rs 7 lakh per financial year will not have to pay tax.

9. Changed in tax structure under New Tax Regime making it attractive for the middle class -- Finance Minister, Ms. Nirmala Sitharaman has reduced the number of tax slabs to five and increased the tax exemption limit to Rs 3 lakh.

The new tax rates under the New Tax Regime

| Total Income (in Rs) |

Rate |

| Upto 3,00,000 |

Nil |

| From 3,00,001 to 6,00,000 |

5% |

| From 6,00,001 to 9,00,000 |

10% |

| From 9,00,001 to 12,00,000 |

15% |

| From 12,00,001 to 15,00,000 |

20% |

| Above 15,00,000 |

30% |

(Source: Budget 2023-24 Speech)

This, according to the finance minister, is expected to provide major relief to all taxpayers in the new regime.

"We are also making the new income tax regime as the default tax regime. However, citizens will continue to have the option to avail the benefit of the Old Tax Regime," said Ms. Sitharaman in her budget speech.

10. Standard Deduction for the salaried class under the New Tax Regime -- Currently the New Tax Regime is devoid of exemptions and deductions available under section 10 and chapter VIA of the Income Tax Act, respectively. Even a standard deduction of Rs 50,000 is not allowed under the New Tax Regime.

To provide relief to the salaried class standard deduction the Union Budget 2023-24 has proposed to allow the standard deduction of Rs 50,000 under the New Tax Regime. Thus each salaried person with an income of Rs 15.5 lakh or more will thus stand to benefit by Rs 52,500 in terms of tax on total income payable (excluding the payment of education & health cess). If the education and health cess of 4% is considered, it helps an individual assessee with an income of nearly Rs 20 lakh to save Rs 54,600 per annum under the New Tax Regime.

#Under the New Tax Regime FY 2023-24, a standard deduction of Rs 50,000 is subtracted from Gross Total Income.

#Under the New Tax Regime FY 2023-24, a standard deduction of Rs 50,000 is subtracted from Gross Total Income.

* Under the New Tax Regime FY 2023-24, a standard deduction of Rs 50,000 as well as maximum permissible deduction limits for children's education allowance, profession tax, health insurance premium, interest on a home loan of an SOP, for 80C items, meal allowance, NPS, and Leave Travel Allowance are considered for deduction from Gross Total Income.

While the Union Budget 2023-23 proposal apparently encourages people to opt for the New Tax Regime, in my view, those with a higher Gross Total Income of Rs 20 lakh or more will stand to benefit under the Old Tax Regime (where a variety of exemptions and deductions can be claimed), while those below that income may on case-to-case basis could opt for the New Tax Regime. Currently, there are more assessees filing ITRs under the Old Tax Regime, than under the New Tax Regime. The former encourages making tax-saving investments, while the latter does not.

11. Increase in leave encashment limit -- Currently, the encashment of earned leave up to 10 months of average salary, at the time of retirement in case of an employee (other than an employee of the Central Government or State Government), is exempt under sub-clause (ii) of clause (10AA) of section 10 of the Income-tax Act. The maximum amount which can be exempted is Rs 3 lakh at present. The Union Budget 2023-24 has now proposed to issue a notification to extend this limit to Rs 25 lakh.

12. Reduction in surcharge -- The government also has reduced the surcharge applicable to higher income assessees levied on their income tax to 25% from 37% under the New Tax Regime. This will effectively reduce the tax rate on income above Rs 2 crore to 39% from the current 42.7%.

Other than these, deductions from family pension up to Rs 15,000 will be now allowed from FY 24 under the new regime also.

The government has also proposed to reduce the TDS rate on the tax portion of the Employee Provident Fund (EPF) withdrawals in non-PAN cases from 30% to 20%.

However, from FY24 when huge claims are made by high-net-worth assesses it is proposed that the deduction from capital gains on investment in residential houses under Sections 54 and 54F will now be capped at Rs 10 crore.

Much to the dismay, the budget expectations that standard deduction will be increased, and so would the maximum permissible deduction under Section 80C, 80D, 24(b), children's education and hostel allowance, and raising long-term capital gains on equities among others, have not been addressed. Had this been done, it would have been more populist and encouraged investments by individuals. It appears that the government going forward may phase out the Old Tax Regime (currently offering exemptions and deductions), which may dissuade investments for the lack of tax incentives.

[Read: Old or New Tax Regime - Which is Beneficial for You Post the Union Budget 2023-24 Announcements]

Having said that the Union Budget 2023-24 has aimed to a balancing act amid challenging times ahead.

Happy Investment & Tax Planning!

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.