ITR Filing Made Easy: Document Checklist for FY 2023-24 Tax Season

Mitali Dhoke

Jun 24, 2024 / Reading Time: Approx. 10 mins

Listen to ITR Filing Made Easy: Document Checklist for FY 2023-24 Tax Season

00:00

00:00

There is a list of certain documents required to be submitted and held as evidence under the Income Tax Act, 1961, to file Income Tax Return in India. Every individual liable to file taxes is required to possess these documents, and thus, you need to keep such documents handy to ensure that your ITR filing process is hassle-free.

Considering this, the Government of India gives taxpayers a sufficient time period of four months after the end of the Financial Year (on 31st March) to compile their documents.

[Read: Easy ITR Filing Process: 10 Steps to File Your ITR Online]

The Income Tax filing procedure and the documents required for tax filing vary depending on the income earned per year and the income source, such as business profit, salary, interest income, investment profit, etc. Here's an example of what types of documents are required for different sources of income:

|

Type of Income/Tax-saving Investment

|

Documents Required

|

| Salary Income |

Form 16 and Form 26AS |

| Income from other sources |

- Interest or TDS certificate for bank FD interest

- Bank account/bank passbook statement for interest earned from Savings account

- Dividend warrant in case of dividend income

- Rent agreement and TDS certificate (if applicable)

- Any other documentary proof (as applicable)

|

| Capital gains income |

- Purchase and Sale deeds of immovable property

- Contract note/Demat account statement for securities sale/purchase

- Purchase and sale proof/receipts of all applicable capital assets and virtual digital assets

|

| Income from business/profession |

- Balance Sheet

- Audit records (if applicable/mandatory)

- TDS certificates

- Income Tax payment (self-assessment tax/advance tax) challan copy

|

| Tax-saving Investments |

- Receipt of the life insurance premium paid

- Receipt of medical insurance

- Public Provident Fund passbook

- Fixed Deposit receipt

- Home Loan repayment certificate/receipt

- Donation paid receipt

- Tuition fee paid receipt

- Mutual Fund Consolidated Account Statement (CAS)

- Education Loan repayment certificate

|

As the Income Tax Return filing or ITR filing season approaches, the scramble for gathering all the relevant documents to ensure the returns are filed on time has begun. The last date to file Income Tax Return (ITR) by individual taxpayers who are not subject to tax audit for the Financial Year 2023-24 (AY 2024-25) is July 31st, 2024, unless the Government decides to extend the deadline.

Keep your documents ready before you start filing your Income Tax Return for FY 2023-24 (AY 2024-25) by checking out our comprehensive list of the most important ITR documents.

1. Linked PAN and Aadhaar card

A PAN card and an Aadhaar card are the first and foremost prerequisites if you are filing an income tax return. According to Section 139AA of the Income Tax Act, individuals need to provide his/her Aadhaar card details while filing the returns. PAN is also required to deduct TDS and should be linked with your bank account for direct credit of income tax refund (if any). The Income Tax Department issues it, and a salaried employee can find the PAN number either on a PAN card, Form 26AS, Form 16, Form 12BB etc.

The deadline for the Aadhaar-PAN link has ended on 30th June 2023. But, those whose PAN and Aadhaar are still not seeded will still be able to file their respective ITR. However, the Income Tax Department will not process their return until they link their PAN with Aadhaar.

The taxpayers who failed to link their PAN-Aadhaar within the deadline of 30th June 2023, their PAN card has become inoperative, now to reactivate your PAN and link your PAN with Aadhaar one needs to pay Rs 1,000 as a penalty.

2. Form-16

The employer issues Form-16 to all salaried individuals. This Form consists of the details of the employee's salary and the amount of TDS deducted from the salary. Form 16 consists of two different parts, Part A and Part B, both of which have the TRACES logo and unique ID.

-

Part-A contains the details of the amount of tax deducted by the employer during the financial year, along with the PAN and TAN details of the employer.

-

Part B of the Form consists of TDS calculations like gross salary breakup, exempt allowances, perquisites, etc.

The Form - 16 of an individual acts as proof of tax paid on time and is a vital document for filing Income tax return by salaried individuals. It proves that the income of an individual employee (earned from their salary) is valid and on record with the Indian Government and Income Tax department. In addition, you are required to collate the information on all taxable allowances you have received, i.e. the exemptions claimed on these allowances, such as house rent allowance, leave travel allowance, etc. Kindly disclose this information in your applicable ITR form. Your month-wise salary slips are also essential for ITR filing if you are a salaried individual.

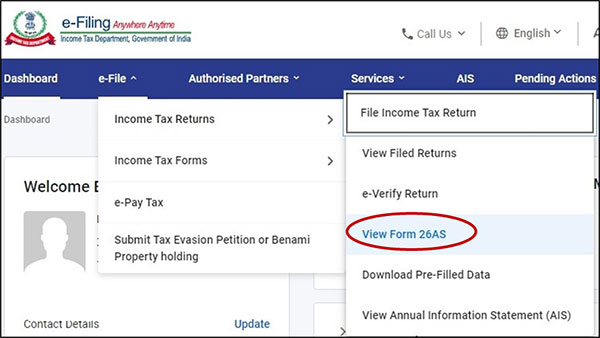

3. Form 26AS

Form 26AS, also known as the annual consolidated statement, is an important document that contains all tax-related information of the taxpayer, like TDS, advance tax, details of pending and completed tax proceedings, tax refunds received, etc. It is an annual credit statement provided by the Income tax department, one of the most important documents required for Income tax return filing. Form 26AS can be easily downloaded by individuals from the new income tax portal. Log in to 'https://eportal.incometax.gov.in/iec/foservices/#/login'

You can also download Form 26AS through the TRACES website or even via net banking. You must ensure that the taxes deducted during the financial year are reflected against your PAN in Form 26AS. If there is a mismatch, you must get it rectified at the earliest by getting in touch with the deductor, otherwise, you will not be able to claim tax credit for the TDS deduction.

4. Documents Related to Interest Income

When it comes to evaluating your interest income, keep the documents handy such as bank statements/passbook for interest on a Savings account, interest income statements for Fixed Deposits, and TDS certificates issued by banks and others. In some cases, you are eligible for a deduction of taxes on interest earned from your bank savings account and deposits. In case you are not liable under the taxable bracket, you can simply prevent this tax deduction by submitting Form 15G for individuals/Form 15H for senior citizens.

5. Tax-saving Investment Proofs

Individuals must gather tax-saving investment and expenditure proofs while filing tax returns to claim deductions. Tax-saving investment and expenditure proofs such as receipt of the life insurance premium paid, receipt of medical insurance, Public Provident Fund passbook, Fixed Deposit receipt, home loan repayment certificate/receipt, donation paid receipt, tuition fee paid receipt, mutual fund consolidated account statement for ELSS, education loan repayment certificate, etc. are essential to claim a deduction when filing ITR. However, You can claim these deductions if you opt for the Old Tax Regime when filing Income tax return.

Generally, employees declare and submit these proofs to their employers to avoid higher TDS on their salary. The proofs submitted are mentioned in Part B of Form 16, and the Income Tax Department uses this information and pre-fills it in the ITR form. However, in case you miss declaring any tax-saving proof, then you can claim it at the time of Income tax return filing.

6. Capital Gains

Capital gains tax is applicable after selling any capital assets like shares, mutual funds, residential property, gold, etc. These gains are taxable, and the tax rate depends upon the type of investment and the returns on it.

It is mandatory to obtain the details of long-term investments in the ITR. You need to ensure that you possess the documents related to any such transactions made in FY 2023-24 for Capital gains tax liability.

In addition, there are a few changes that you should consider when filing your ITR for FY 2023-24. The income generated from the transfer of Virtual Digital Assets (VDAs) needs to be reported in the ITR; it will be subject to taxation at a rate of 30% and applicable surcharge and cess. Such income can be taxed either under the head of business income or capital gains.

7. Other Required Documents

Apart from the above-mentioned documents, there are several other documents required while filing the ITR that varies for every taxpayer.

-

Interest Certificate for Home Loans - The individuals are provided with the details like principal and interest that they repay in their loan statement. This breakup information is needed as proof and to provide information while filing your ITR. If the individual has taken a home loan from financial institutions like banks, they should collect the statement for the last Financial Year, 2023-24.

Interest paid on housing loan is eligible for tax saving up to Rs 2,00,000 per financial year under Section 24(b) of the Income Tax Act, for self-occupied property. In case of let out or deemed to be let out property, the entire interest paid on the housing loan can be claimed as a deduction, there is no upper limit on the amount of interest that can be claimed as deduction.

-

Donation Receipts - Many of you have considered donating to charity and contributing to society. Under Section 80G of the Income Tax Act of 1961, the Government encourages support for charitable services by allowing you a tax deduction for donations made to charitable organisations. Ensure to maintain your donation receipts as documents required while filing your Income tax return.

Additionally, in the current year's ITR Form, a new column has been added to 'Table D'. This column requires disclosure of the ARN (Donation Reference Number) for donations made to entities where a 50% deduction is allowed, subject to the qualifying limit. The ARN should be obtained from the donation certificate issued in Form 10BE by the donee institutions and should be mentioned in the Income tax return.

To conclude...

The ITR filing deadline is just a few days away unless extended. If this date is missed, a belated ITR can still be filed until December 31, 2024, with a late filing penalty of Rs 1,000/-. However, if the total income is more than Rs 5,00,000, then the penalty farthest will be expanded to Rs 5,000/-. One must file the ITR with the required documents on time to avoid such penalty charges.

The experts are urging taxpayers to prevent any delay towards this critical financial task. Many taxpayers tend to delay their Income tax return filing till the last day, which creates a hotchpotch, as you need to collate several documents and information required to file the ITR for the specific financial year. Therefore, to avoid such consequences, you must keep the above-mentioned documents ready and file your Income Tax Return as early as possible.

Frequently Asked Questions (FAQs)

1. What Is ITR Filing?

Income Tax Return (ITR) filing is a process consisting of a form in which taxpayers file information about their income earned and tax applicable to the income tax department. It contains information about your income and the taxes to be paid during the financial year. The ITR form declares the net tax liability, claiming tax deductions, and reporting the gross taxable income.

2. Who Should File an ITR?

Filing an Income Tax Return is mandatory if the aggregate of all your income exceeds the basic exemption limit. There are various criteria for a basic exemption limit based on your age and income slab. Kindly refer to (www.incometaxindia.gov.in - tax slabs for AY2024-25)

3. What Is the Time Period to File an ITR?

You should file your ITR on or before the mentioned due date to avoid any errors. Ideally, an ITR should be filed on or before July 31st of the assessment year. For example, to file the ITR of FY 2023-24, the due date will be July 31st, 2024.

4. What Happens If I Fail to File My ITR Before Due Date?

In case you fail to file your ITR before the due date, it will lead to certain ramifications, and you will be charged late fee as a penalty. The non-filing of ITR might be considered as tax evasion, which is punishable under Income Tax Act 1961.

5. What Are the Benefits of ITR Filing?

If you file your income tax return with accurate information on or before the due date, you could save on your tax with applicable deductions and get a tax refund. If you file your ITR well on time without delaying it until the last minute, you will avoid errors, undue stress, and a penalty.

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

MITALI DHOKE is a Research Analyst at PersonalFN. She is an MBA (Finance) and a post-graduate in commerce (M. Com). She focuses primarily on covering articles around mutual funds including NFOs, financial planning and fixed-income products. Mitali holds an overall experience of 4 years in the financial services industry.

She also actively contributes towards content creation for PersonalFN’s social media platforms in the endeavour to educate investors and enhance their financial knowledge.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.