Old or New Tax Regime - Which is Beneficial for You Post the Union Budget 2023-24 Announcements

Mitali Dhoke

Feb 01, 2023 / Reading Time: Approx. 8 mins

Listen to Old or New Tax Regime - Which is Beneficial for You Post the Union Budget 2023-24 Announcements

00:00

00:00

In my previous article, I explained in detail the functioning of the Old Tax Regime vs the New Tax Regime and the key difference between them.

Today, February 01, 2023, our Finance Minister, Ms Nirmala Sitharaman, presented the last full budget of the Modi government before next year's parliamentary elections, slated for April-May 2024. The cost of living has increased in the past few years, which has added to inflationary pressures. The Union Budget 2023 is likely to put emphasis on taxpayers by offering them tax relief and the addition of tax deductions to increase their purchasing power (money in hand) and revive the Indian economy.

Union Budget announcements this year focused on pro-growth measures with a special boost to the infrastructure, unleashing the potential, green growth, youth power and inclusive development. The budget aims to maintain India's growth momentum in FY 2023-2024 despite a further slowdown in the global economy.

*This video is for information purposes only and is not meant to influence your investment decisions.

Finance Minister Ms Nirmala Sitharaman's Budget Speech 2023 was her 5th consecutive budget speech which includes several proposals for the benefit of taxpayers in the lowest and highest tax brackets. No announcement on income tax was made in the 2022 budget; however, in the latest budget, 5 personal income tax-related announcements were made. Here's the list of tax-related major announcements:

-

Under the New Tax Regime (introduced in budget 2020), the basic exemption limit has been raised to Rs 3 lacs, up from Rs 2.5 lacs earlier

In a bid to make the New Tax Regime more effective for taxpayers, the basic exemption limit, which was Rs 2.5 lacs has been increased to Rs 3 lacs. This is applicable to taxpayers across all age groups. An individual earning an annual income < Rs 3 lacs is exempt from paying tax only under the New Tax Regime.

In addition, the government has also announced changes in income tax rates for individuals opting for the new tax regime, and the number of tax slabs has been reduced to 5 from 6. The new regime will be the default tax regime; the old one, however, has not been discontinued, and taxpayers can continue to use it either.

Table 1: Revised tax slabs and rates for New Tax Regime for FY 2023-24 and AY 2024-25

(Source: indiabudget.gov.in)

(Source: indiabudget.gov.in)

-

The highest surcharge rate is reduced from 37% to 25% in the New Tax Regime

A surcharge is a tax on tax, and it is levied on the tax payable and not on the income generated. For example, if you have an income of Rs 1,000, on which Rs 300 is the taxable amount, the surcharge would be 10% of Rs 300. In India, the surcharge is applicable to high-income groups. Currently, the surcharge on income tax under both the old regime and the new regime is as follows:

- 10% if income is above Rs 50 lacs and up to Rs 1 crore

- 15% if income is above Rs 1 crore and up to Rs 2 crore

- 25% if income is above Rs 2 crore and up to Rs 5 crore

- 37% if income is above Rs 5 crore.

Finance Minister Ms Nirmala Sitharaman has proposed to reduce the highest surcharge rate from 37% to 25% in the new tax regime. This proposal would result in a reduction of the maximum tax rate to 39% for those in the highest tax bracket. Previously, the effective tax rate for those in the highest tax bracket was 42.74%.

-

Section 87A rebate increased from the current Rs 5 lacs to Rs 7 lacs in the new tax regime

Section 87A provides a tax rebate to individual taxpayers if their total income is less than Rs 5 lakh after claiming deductions. Currently, those with income of up to 5 lacs do not pay any income tax and a maximum rebate of up to Rs 12,500 under Section 87A of the Income-Tax Act is allowed.

As per the budget proposal, there is an increase in the rebate and individuals earning up to Rs 7 lakh will have to pay no tax under the New Regime.

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

The Finance Minister also announced several proposals for the benefit of salaried individuals, senior citizens and pensioners.

-

Proposal to extend the benefit of the standard deduction in the New Tax Regime for the salaried class and the pensioners, including family pensioners

The standard deduction is the amount that is not subject to tax, in addition to the basic exemption limit. Currently, the standard deduction is Rs 50,000 in the Old Regime, and the max deduction for professional tax is Rs 2,500. As per the Budget 2023, the Finance Minister said that each salaried person with an income of Rs 15.5 lacs or more would thus stand to benefit by an additional Rs 52,500 in terms of tax savings.

-

Hike in tax exemption limit on leave encashment on the retirement of non-government salaried employees

The limit of Rs 3 lacs was last fixed in 2002 during the Atal Bihari Vajpayee government when the highest basic pay in the government was Rs 30,000 per month. In line with the increase in government salaries, Finance Minister proposed to increase this limit to Rs 25 lacs from Rs 3 lacs earlier.

Now that you are aware of the applicable changes to the New Tax Regime after the Union Budget FY 2023-24 announcements, should you opt for it?

You see, the old tax regime offers various exemptions and deductions under numerous sections for tax-saving purposes. On the other hand, the new regime provides revised tax rates and more flexibility and tries to simplify the process.

Which tax regime should you opt for after the Budget 2023 announcements?

Let us compare with an example to identify which tax regime will be beneficial for you, and it provides a better perspective on which one should you opt for:

An individual's taxable income is obtained after deducting various deductions under chapter VI A of the Income Tax Act 1961. i.e. the deduction ranging from Section 80C to 80U from the Gross Total Income (GTI).

In the given example, we have calculated the taxable income after considering commonly used deductions such as: Standard deduction u/s 16, Children education allowance u/s 10(14), Professional tax u/s 16(iii), Mediclaim u/s 80D, Housing loan interest u/s 24(b), Leave travel allowance u/s 10(5), Meal allowance exemption, deductions for NPS and other benefits under section 80C.

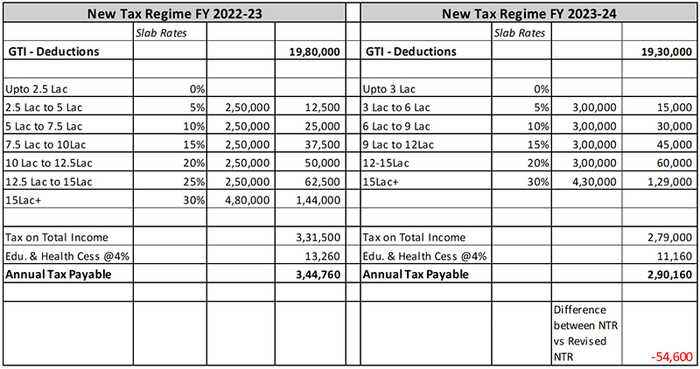

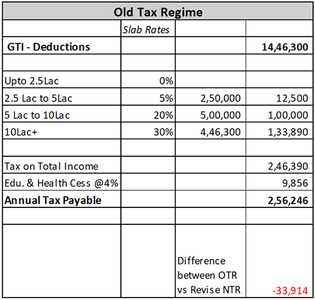

Table 2: Comparison of income tax rates under the old tax regime vs new tax regime till FY 2022-23 and the rates applicable from FY 2023-24.

(Source: PersonalFN Research)

(Source: PersonalFN Research)

As you can see, there is a substantial difference when you opt for the new tax regime due to the flexible rates as compared to the old tax regime. However, do note that the New Tax Regime aims to provide relief to you taxpayers, but it does not allow major exemptions and deductions that are available in the old tax regime. As a result, choosing between the Old and New Income Tax Regimes would entirely depend on a case-to-case basis.

As an assessee, you have the option to choose between the Old Tax Regime and the New Tax Regime while filing your ITR in a financial year. Your decision to choose the best suitable tax regime should be based on a variety of factors such as current income level, income structure, exemptions and deductions you are eligible for, etc.

Therefore, the tax benefits have been tweaked in the Union Budget 2023 to encourage individuals to move towards new tax regime, which has not seen much traction since its launch in FY 2020-21 and to provide relief to middle-class taxpayers.

MITALI DHOKE is a Research Analyst at PersonalFN. She is an MBA (Finance) and a post-graduate in commerce (M. Com). She focuses primarily on covering articles around mutual funds including NFOs, financial planning and fixed-income products. Mitali holds an overall experience of 4 years in the financial services industry.

She also actively contributes towards content creation for PersonalFN’s social media platforms in the endeavour to educate investors and enhance their financial knowledge.