Should Home Loan Borrowers Still Opt for the Old Tax Regime?

Ketki Jadhav

Feb 04, 2023 / Reading Time: Approx. 5 mins

Listen to Should Home Loan Borrowers Still Opt for the Old Tax Regime?

00:00

00:00

The Indian taxation system underwent a significant change in the Union Budget 2023-24, encouraging individual taxpayers to opt for the new tax regime by offering higher tax rebate limit compared to the old tax regime. However, it is ultimately up to the taxpayer to choose which regime to opt for.

For home loan borrowers, the decision to choose between the two regimes can have a significant impact on their tax liabilities and eventually their finances. On one hand, the old tax regime provides higher deductions on interest & principal payments on home loans, while on the other hand, the new regime provides lower tax rates and no exemptions on other investments. In this article, we will explore the key differences between the two tax regimes and if it makes sense for home loan borrowers to opt for the old tax regime.

In India, property prices have been on the rise for many years, especially in urban areas where the demand for housing is high. This trend is expected to continue in the coming years as well, with the growth in the country's population and as the economy develops. The rising property prices can have several implications for primary home buyers, particularly those who are considering a home loan to finance their purchase.

One of the main implications of rising property prices is the increase in the home loan amount required to purchase the property. This can result in a higher EMI burden for home loan borrowers, as they need to repay the loan over a longer period and pay high interest as well.

Given the high EMI burden, the choice between the old and new tax regimes for home loan borrowers is one such opportunity to optimize their tax benefits and reduce their financial burden.

Home loan deduction under Section 80C of the Income Tax Act, 1961, is one of the important tax benefits available to home loan borrowers in India. The section allows individuals to claim a tax deduction of the principal component of their home loan repayment. The maximum amount that can be claimed as a deduction under this section is Rs 1.5 lakhs.

In addition to the deduction under Section 80C, home loan borrowers can also claim a tax deduction on the interest component of their home loan repayment under Section 24(b) of the Income Tax Act. The maximum amount that can be claimed as a deduction under this section is Rs 2 lakhs for self-occupied properties.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

These tax benefits can help home loan borrowers reduce their overall tax liability and minimize the cost of their home loan. However, you cannot claim the deduction under Section 80C if you have opted for the new tax regime. The new tax regime, introduced in the Union Budget 2020, offers lower tax slab rates but eliminates certain tax deductions and exemptions, including the deduction under Section 80C. By opting for the new tax regime, individuals forego the opportunity to claim the deduction under Section 80C and other tax benefits, but in return, they get a lower tax rate and a simplified tax structure.

The old tax system features three tax brackets, each with a corresponding rate of 5%, 20%, and 30%. The 20% rate is applied to the income range between Rs 5 to 10 lakhs, while the highest bracket begins for income exceeding Rs 10 lakhs. However, these tax rates only take effect after deductions are considered, so it is crucial to determine the available deductions.

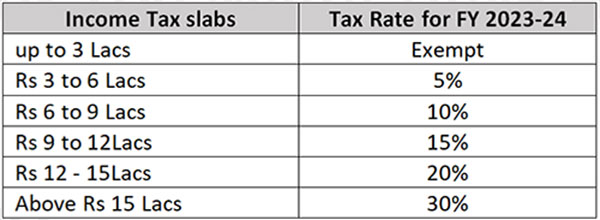

The blocks in the new tax regime are updated to Rs 3 lakhs each, so the 5% tax rate applies to the income range between Rs 3 lakhs to Rs 6 lakhs, and the 10% rate applies to the next range from Rs 6 lakhs to 9 lakhs, and so on.

Table 1: Revised tax slabs and rates for New Tax Regime for FY 2023-24 and AY 2024-25

(Source: indiabudget.gov.in)

(Source: indiabudget.gov.in)

Here's an illustration to show how a home loan borrower in a higher tax bracket can effectively save tax by opting for the old tax regime:

Table 2: Calculation of Income Tax for an individual below 60 years with an annual income of Rs 10 lakhs

|

Old Regime |

New Regime |

| Gross Income |

10,00,000 |

10,00,000 |

| (-) Standard deduction |

50,000 |

50,000 |

| (-) Principal repayment under Section 80C |

1,50,000 |

- |

| (-) Interest repayment under Section 24(b) |

2,00,000 |

- |

| Taxable Income |

6,00,000 |

9,50,000 |

| Tax Due (including health & education cess) |

33,800 |

54,600 |

Source: PersonalFN Research

(The table is for illustration purposes only and the actual tax liability will depend on the individual's specific financial circumstances, tax bracket, and loan repayment amount.)

Apart from the home loan deductions, utilizing benefits under other tax-saving options like health insurance, NPS, LTA, etc. can lead to a substantial reduction in tax payments. Let's see how this can be achieved:

Table 3: Calculation of Income Tax for an individual below 60 years with an annual income of Rs 10 lakhs

|

Old Regime |

New Regime |

| Gross Income |

10,00,000 |

10,00,000 |

| (-) Standard deduction |

50,000 |

50,000 |

| (-) Principal repayment under Section 80C |

1,50,000 |

- |

| (-) Interest repayment under Section 24(b) |

2,00,000 |

- |

| (-) Health insurance for family and senior citizen parents under Section 80D |

75,000 |

|

| (-) NPS under Section 80CCD(1B) |

50,000 |

|

| Taxable Income |

4,75,000 |

9,50,000 |

| Tax Due (including health & education cess) |

11,700 |

54,600 |

Source: PersonalFN Research

(The table is for illustration purposes only and the actual tax liability will depend on the individual's specific financial circumstances, tax bracket, and loan repayment amount.)

As we can see from the above tables, home loan borrowers in the higher tax bracket can effectively save tax by opting for the old tax regime, as they can claim the tax deductions under Section 80C and 24(b) of the Income Tax Act. The tax savings under the old tax regime can be substantial and can help the borrowers manage the high EMI burden and achieve their financial goals more effectively.

While the new tax regime has streamlined the tax system and simplified the tax filing process for individuals and businesses, the removal of these tax incentives can lead to an increase in the overall tax burden, making it deterring for individuals to invest their money. This is because investment decisions are often based on the potential tax savings that can be achieved through deductions and exemptions. The lack of these incentives in the new tax regime can be seen as a disincentive for investing, as it reduces the potential financial benefits of investing.

While the old tax regime offers tax deductions, to ensure this regime is advantageous for you if your income is higher than Rs 15 lakhs, the total deduction needs to be higher as well. Hence, it makes sense to claim other essential tax-saving options too like health insurance for self/family and senior citizen parents, NPS, LTA, etc., which could help you save a maximum amount with the old tax regime.

Let's see how using multiple tax-saving instruments can result in ample tax savings:

Table 4: Calculation of Income Tax for an individual below 60 years with an annual income of Rs 25 lakhs

|

Old Regime |

New Regime |

| Gross Income |

25,00,000 |

25,00,000 |

| (-) Standard deduction |

50,000 |

50,000 |

| (-) Principal repayment under Section 80C |

1,50,000 |

- |

| (-) Interest repayment under Section 24(b) |

2,00,000 |

- |

| (-) Health insurance for family and senior citizen parents under Section 80D |

75,000 |

|

| (-) NPS under Section 80CCD(1B) |

50,000 |

|

| Taxable Income |

19,75,000 |

24,50,000 |

| Tax Due (including health & education cess) |

4,21,200 |

4,52,400 |

Source: PersonalFN Research

(The table is for illustration purposes only and the actual tax liability will depend on the individual's specific financial circumstances, tax bracket, and loan repayment amount.)

Table 5: Calculation of Income Tax for an individual below 60 years with an annual income of Rs 25 lakhs

|

Old Regime |

New Regime |

| Gross Income |

25,00,000 |

25,00,000 |

| (-) Standard deduction |

50,000 |

50,000 |

| (-) Principal repayment under Section 80C |

1,50,000 |

- |

| (-) Interest repayment under Section 24(b) |

2,00,000 |

- |

| Taxable Income |

21,00,000 |

24,50,000 |

| Tax Due (including health & education cess) |

4,60,200 |

4,52,400 |

Source: PersonalFN Research

(The table is for illustration purposes only and the actual tax liability will depend on the individual's specific financial circumstances, tax bracket, and loan repayment amount.)

So, as you can see in Table 4 & 5 when your income is on the higher side and you do not claim a higher tax deduction, the old tax regime will not prove to be much advantageous to you. Hence it is crucial to analyze your tax bracket, home loan due amount, investments, and expenses eligible for a tax deduction benefit, and other financial circumstances to determine the best tax regime for the specific situation and accordingly achieve optimum tax savings.

In conclusion, the choice between the old and new tax regime after the Union Budget 2023-24 announcement is an important one for home loan borrowers. The old tax regime, with its exemptions and deductions, can provide significant tax savings for those who have a high income, home loan, and other tax-saving investments. On the other hand, the new tax regime offers lower tax rates and fewer exemptions, making it an attractive option for taxpayers who do not have multiple sources of income and are not able to claim higher deductions. However, we cannot ignore the fact that the new tax regime promotes the culture of 'spending' and not 'saving'. Ultimately, the decision between the two regimes will depend on the individual taxpayer's tax liability and financial situation. To make the best choice, home loan borrowers need to understand the benefits and drawbacks of both regimes and consider their own financial goals and needs. While the old tax regime is for savers and investors, the new tax regime is for spenders.

KETKI JADHAV is a Content Writer at PersonalFN since August 2021. She is an MBA (Finance) and has over seven years of experience in Retail Banking. Ketki specialises in covering articles around banking, insurance, personal finance, and mutual funds and has been doing it for over three years now.