Will Tax Saving Instruments Lose Their Appeal After the Union Budget 2023-24

Divya Grover

Feb 06, 2023 / Reading Time: Approx. 6 mins

Listen to Will Tax Saving Instruments Lose Their Appeal After the Union Budget 2023-24

00:00

00:00

The government introduced the new optional tax regime in the Union Budget in FY 2020-21 to offer benefits of lower tax rates to taxpayers who do not claim much deductions or exemptions. However, taxpayers who opt for the new tax regime have to forego all deductions and exemptions.

Taxpayers can only avail of deductions under Section 80C of the Income Tax Act through investments in tax-saving instruments such as Public Provident Fund (PPF), National Pension System (NPS), Equity Linked Saving Scheme (ELSS), Tax Saving Bank FDs, and insurance-cum-investment products such as term insurance, ULIPs, and guaranteed return plans if they opt for the old tax regime.

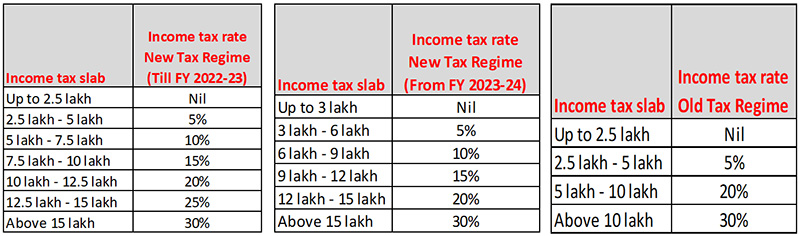

The old tax regime has been a preferred choice for most taxpayers till now. With a view to make the new tax regime attractive for taxpayers, the government during its Union Budget 2023-24 proposed a major revamp to the income tax slab and rates under the new tax regime. It has lowered the number of slabs to five and raised the tax exemption threshold to Rs 3 lakh from Rs 2.5 lakh. The income tax rates and slabs under the old tax regime remain unchanged.

In addition, the government has raised the rebate ceiling to Rs 7 lakh from Rs 5 lakh for those opting for the new tax regime. It has also extended the benefit of a standard deduction of Rs 50,000 to individuals under the new tax regime. Moreover, the new tax regime will now be the default tax regime, though taxpayers will have the option to stay with the old tax regime.

Income tax rates and slabs under the new and old tax regime

Most taxpayers invest heavily in tax-saving instruments such as PPF, NPS, ELSS, Tax Saving Bank FDs, and insurance-cum-investment products, that are eligible for income tax deduction up to Rs 1.5 lakh in a financial year under Section 80C of the Income Tax Act.

But with a higher basic exemption limit and lower tax outgo, many taxpayers are expected to shift to the new tax regime. Notably, the new tax regime will make the tax filing process easier as it will not require much planning related to investment in tax-saving instruments. This, in turn, will mean that investments in tax-saving instruments could take a major hit.

Should you continue to invest in tax-saving instruments?

It is observed that taxpayers often delay their tax planning exercise till the end of the financial year, which results in financial mistakes. Do note that investment should never be made solely for the purpose of avoiding taxes but for creating wealth for the long term. More importantly, the investments should align with your financial goals, risk profile, and investment horizon. The Union Budget 2023-24 has ensured that taxpayers do not engage in impulsive investments in tax-saving instruments.

If you are able to fully utilise deductions under various Sections such as 80C (eligible investments), 80D (insurance premium), and 80E (interest on education loan), Sec 24 (interest on home loan), as well HRA, LTA, and lunch coupons, it might be beneficial to stay in the old tax regime. Such investors can invest and avail benefits of various tax saving instruments viz. PPF, EPF, ELSS, SSY, NSC, SCSS, Tax Saver Bank FD, NPS, etc.

(Image source: www.freepik.com - photo created by rawpixel.com)

(Image source: www.freepik.com - photo created by rawpixel.com)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

That said, even if you continue with the new tax regime, tax-saving instruments can form a part of your portfolio if they align with your financial needs.

Here are the benefits these avenues have to offer apart from tax savings:

PPF, SSY, SCSS, and MIS offer long-term wealth solutions offering higher interest rates compared to Bank FDs. These avenues invest predominantly in government securities and corporate bonds to help you build a significant corpus for your various goals, such as retirement, children's education/marriage, buying your dream home, etc., without much volatility.

These schemes are backed by the Indian government and therefore carry minimal risk. They act as a good diversification tool and enable disciplined savings as the money is locked in for a certain period. The government has increased the investment limit under SCSS and MIS so that investors can allocate more for their goals and benefit from higher interest rate.

On the other hand, ELSS and some plans of NPS invest predominantly in equities which can help you earn better gains and accumulate a bigger corpus. The lock-in period ensures that your corpus stays invested through market highs and lows to generate significant capital appreciation through equities over the long run.

While you invest for your future, do not ignore insurance and get adequate life and health cover for you and your family. But ensure that you do not co-mingle investment with insurance as the objective of insurance is to provide cover during emergencies and not capital growth.

To conclude...

The new tax regime will likely put more disposable income in the hands of taxpayers due to lower tax outgo. This may increase consumption and lead to reduced savings and investment, thereby impacting future goals. Therefore, it is necessary to continue investments in suitable financial instruments.

Individuals should compare their taxability under both tax regimes after taking into account all the financial goals, investments, and expenses and take an informed decision. Opt for the tax regime that offers optimal tax savings.

PPF, NPS, ELSS, SCSS, etc., offer various benefits apart from being efficient tax planning instruments. Thus, individuals under the new tax regime can also allocate some portion in these avenues if it helps them meet their future goals.

DIVYA GROVER is the co-editor for FundSelect, the flagship research service of PersonalFN. She is also the co-editor of DebtSelect. Divya is an avid reader which helps her in analysing industry trends and producing insightful articles for PersonalFN’s popular newsletter – Daily Wealth letter, read by over 1.5 lakh subscribers.

Divya joined PersonalFN in 2019 and has since then used stringent quantitative and qualitative parameters to analyse funds to provide honest and unbiased research to investors. She endeavours to enable investors to make an informed investment decision and thereby safeguard their wealth.