Are You Holding an Adequate Emergency Fund Amidst the Third Wave of COVID-19 Pandemic?

Rounaq Neroy

Jan 19, 2022

Listen to Are You Holding an Adequate Emergency Fund Amidst the Third Wave of COVID-19 Pandemic?

00:00

00:00

World over, coronavirus infections have increased, of both the earlier Delta variant and the very recent Omicron variant (B.1.1.529), which is far more virulent and classified as 'variant of concern' by the World Health Organisation (WHO). The United States of America currently tops the charts with over 24.3 million active cases, followed by India at 1.83 million cases (as of Jan 19, 2022).

The hospitalisation rate in India during this third wave of COVID-19 has been low (around 10% compared to 20%-23% during the second wave)---thanks to the seroprevalence and improved inoculation rate. However, experts in the government warn that the situation is dynamic and may change given our density of population and the fact that a large number of people (across states) are skipping their second dose. In the U.S., the hospitalisation rate has risen to an alarming level (across age groups). The World Health Organisation (WHO) has warned that the COVID-19 pandemic is "far from over." Many other nations such as France, Germany, the United Kingdom, and many others in Europe are seeing record-high cases.

In such times, we surely cannot afford to be complacent and drop our guard against COVID-19. At the same time, we need to be financially prepared to, God forbid, handle any medical emergency in the family. So, you need to ask yourself: Am I holding an adequate Emergency Fund amidst the pandemic.

A medical emergency could strike without a forewarning. Life, as you may know, at times, throws a curveball, an unpleasant surprise at us, and brings with it financial complications. "Nothing is imminent than the impossible...what we must always foresee is the unforeseen," said Victor Hugo (a French poet, essayist, novelist, playwright, and dramatist).

If you hold an adequate Emergency Fund, you could handle the exigencies more courageously.

So, how much should be your Emergency Fund?

Well, there is no magic number as such. You need to sensibly figure out a sum of money that will provide you with a financial safety net.

But very broadly, your emergency fund should ideally be:

Emergency Fund = 12 to 24 months of regular monthly unavoidable expenses, including EMIs

So, if your monthly, regular, unavoidable expenses are, say, Rs 35,000, going by the above formula, your Emergency Fund should be: Rs 35,000 x 24 months = Rs 8.40 lakh.

You may further add 5%-10% extra to this amount considering your and your family members' medical condition, history, and health insurance cover. The idea behind this is to hold an Emergency Fund that would provide you with the required cushion, peace of mind, and avoid endangering your financial wellbeing.

(Image source: freepik.com; photo created by jcomp)

(Image source: freepik.com; photo created by jcomp)

Never commit the mistake of holding an inadequate amount as your Emergency Fund; it may leave you with no other option but liquidate investments assigned for other financial goals if a medical emergency (or any other financial emergency) arises and drain you financially.

Also, make it a point to park your Emergency Fund in appropriate investment avenues. Never risk this safe money to invest in stocks, equity mutual funds, debt mutual funds, etc., and/or those with a longer lock-in period viz. Public Provident Fund, National Savings Certificate, Kisan Vikas Patra, and so on. When holding an Emergency Fund, the approach and objective should not be to clock high returns but liquidity and safety of the principal while yielding nominal returns.

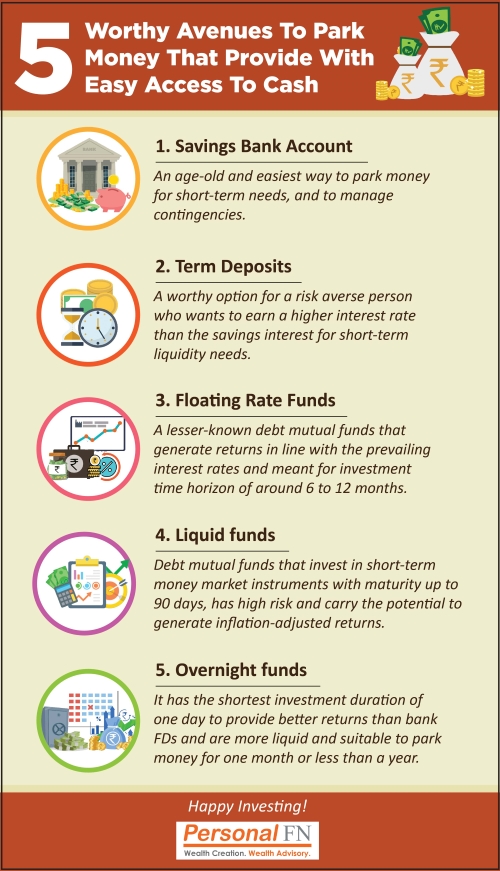

Therefore, ideally, deploy your Emergency Fund in a separate savings account, a pure liquid fund (having no exposure to private issuers and investing only in Government Securities, Treasury Bills and AAA/A1+ rated Public Sector Undertakings)/overnight fund, and/or short-term bank fixed deposit wherein there is safety and liquidity of your hard-earned money in case of an emergency. It is important to select the right mix of these avenues that suit you.

Furthermore, never commit the mistake of utilising money set aside for emergency purposes for non-emergencies, viz., buying a fancy gadget, a car, a vacation, etc. Doing this could dry out your Emergency Fund, making it difficult for you if a medical emergency or any other exigency crops up.

Even when you have used a portion of your Emergency Fund for any other exigency (say you lose your job, for the unexpected rise in your school fees, unavoidable home repairs, etc.), replenishing the Emergency Fund to an adequate level is your responsibility. In this regard, consider engaging in a prudent budgeting exercise (involving your family) to save more, monetise existing assets, and/or utilise the windfall income. This would ensure that you have adequate contingency reserve if another emergency crops up soon after.

If a prudent approach is followed for your Emergency Fund, it would adduce the following benefits:

-

✔ Instil the confidence to handle testing times.

-

✔ Prevent borrowing from friends and relatives and, thus keep debts under control.

-

✔ Provide easy access to your money when you need it the most.

-

✔ Reduce financial and mental stress.

-

✔ Safeguard the financial well-being of your loved ones.

Remember, holding an Emergency Fund is based on the premise: Hope for the best and be prepared for the worst.

And even after having planned well, if you are falling short of money to deal with the emergency, you may consider taking some help from friends/relatives or avail of a Personal Loan. When availing of a Personal Loan for your medical emergency (or any other purpose), consciously do the following:

-

✔ Check your eligibility - it may vary across lenders.

-

✔ Evaluate your need, i.e., how much money you have to borrow.

-

✔ Compare personal loan interest rates, processing charges, the penalty for pre-payment/foreclosure, etc., because all of these charges add to your cost.

-

✔ Check the interest rate, tenure, processing fee, etc.

-

✔ Understand how much the EMI will be on your personal loan (using the Personal Loan EMI calculator).

-

✔ Choose the loan tenure (which can range anywhere between 12 to 60 months) such that the EMIs do not turn out to be a burden.

Amidst the third wave of the COVID-19 pandemic, if you have been falling short of maintaining an adequate Emergency Fund, make a course correction by reviewing your Emergency Fund prudently so that you don't have to borrow money in difficult times. Remember, a stitch in time saves the nine.

Happy Planning & Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

PS: If you are looking for quality mutual fund schemes to add to your investment portfolio, I suggest you subscribe to PersonalFN's premium research service, FundSelect.

PersonalFN's FundSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell. Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

If you are serious about investing in a rewarding mutual fund scheme, subscribe now!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds