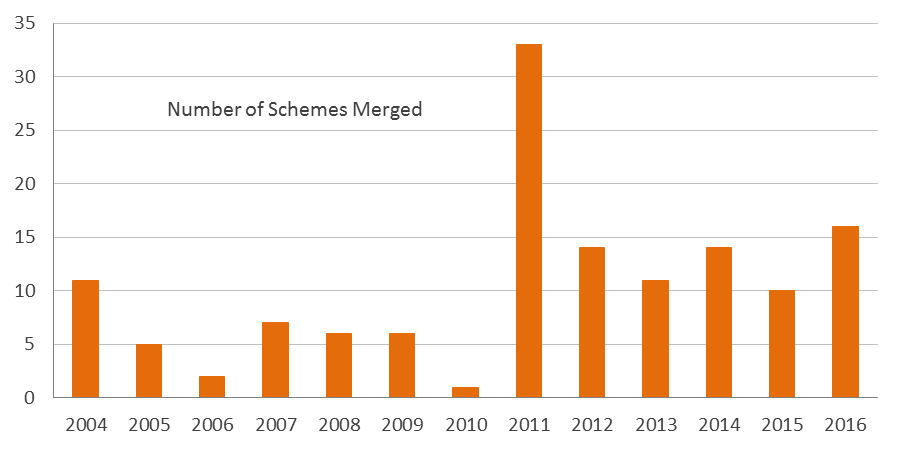

Over the past five years, the mutual fund industry has witnessed as many as 74 equity scheme mergers. This number is excludes mergers of different plans (such as dividend or growth plans) under the same equity scheme and where schemes were merged due to acquisition by another fund house. In 2016, as many as 15 equity schemes were merged – the highest in the past five years. This is result of the capital market regulator, the Security and Exchange Board of India (SEBI) cracking the whip in 2010. The regulator asked fund houses to merge schemes with a similar investment objective, as too many schemes would confuse investors. This push by SEBI led to a flood of equity scheme mergers, as seen in the chart below. From 2011 till date, there have been as many as 98 equity scheme mergers.

Mutual Fund Schemes Mergers

(Source: ACE MF, PersonalFN Research )

You see, in the race to garner more Assets Under Management (AUM), Fund houses established New Fund Offer (NFO) factories rolling more funds in exuberant times, when retail sentiment was high. During the secular bull market between 2004 and 2008, as many as 150 new fund offers were launched. This asset gathering exercise, led to a glut of equity schemes no different from each other. Within fund houses too, there were schemes with overlapping objectives.

What should you do if your mutual fund scheme is merged…

Evaluate the surviving scheme diligently, irrespective whether the scheme(s) is being merged with the one share similar investment objective. This is because, it’s alike to switching another mutual scheme -- a vital investment decision altogether.

While fund mergers are expected to be done in investors’ interest, the surviving scheme may not always be suitable for you.

Besides merging similar schemes, a fund house may merge schemes to create economies of scale or to smother schemes with an embarrassing track record. If a scheme has a small corpus size, it may cost more to manage than what it can generate in fees. Therefore, it is often seen that a fund houses merge schemes which failed to attract investors in to other—often more prominent—schemes.

So, here’s how you should evaluate whether you should continue to remain invested or shift to another scheme…

Investment Objective

In the past, narrow focussed sector schemes have been merged with their more diversified peers. In July 2016, Sundaram-Select Thematic Funds-PSU Opportunity and Sundaram-Select Thematic Funds-Enter Opportunity was merged with Sundaram Equity Multiplier, a flexi-cap scheme which invests across all sectors. In February 2016, Birla Sun Life Latin America Equity was merged with Birla Sun Life Financial Planning Fund FoF - Aggressive Plan. The latter is a hybrid scheme, while the merged scheme invested in global equities. Therefore, if you invested in a scheme with a specific investment objective in mind, such as investing in global equities, the surviving scheme may not meet your investment goal. You will need to review whether or not the new scheme is suitable for your portfolio.

Performance

Fund houses often launch schemes when a specific theme is in flavour, be it strategic schemes such as contra funds or thematic funds. There was a flurry of infrastructure funds between 2006 and 2007, when the infrastructure sector looked promising. However, post the financial crisis, this was among the worst performing sectors. Sector schemes investing in infrastructure stocks suffered. In order to cover up the pitiable performance, such schemes were merged in to other schemes. However, this may not necessarily mean that the surviving scheme is the best amongst its peers. If the investment objective is in line with your goals, review the performance to evaluate if the scheme has consistently beaten its benchmark and thereafter take an appropriate investment decision.

Costs

The fees or expense ratio of a scheme with a smaller corpus is often higher than a scheme with a higher asset base. But, this may not always be true. In 2014, Canara Robeco Nifty Index was merged with Canara Robeco Large Cap+. As the names suggest, the former was an index fund with an expense ratio not exceeding 1.50%, while the latter, a large-cap equity scheme with an expense ratio of 2.75%. Hence, in this case, not only was there a difference in investment objective, but in terms of cost too, you would end up paying higher. Thus evaluate the cost associated with your investments.

Risks

Risk too is an important factor you should evaluate when deciding to continue or exit in case of a scheme merger. Therefore, when an index fund is being merged with equity diversified fund there can be an increased risk. In September 2016, Sundaram Growth was merged with Sundaram Select Focus. While the earlier scheme maintained a diversified portfolio, investing over a number of stocks, the latter maintains a concentrated portfolio of just a few select stocks. Therefore, the risk of the concentrated portfolio will more likely be greater.

To sum up…

If your scheme is being merged it may not always be a good thing. You need to review the new scheme, and perhaps even review your entire mutual fund portfolio to take a deserving action – be it Buy, Hold or Sell. Conducting a portfolio review will help you be rightly placed on the path to long-term wealth creation whereby you can achieve many of your financial goals.

Add Comments